United Kingdom 3D Bioprinting Market Size

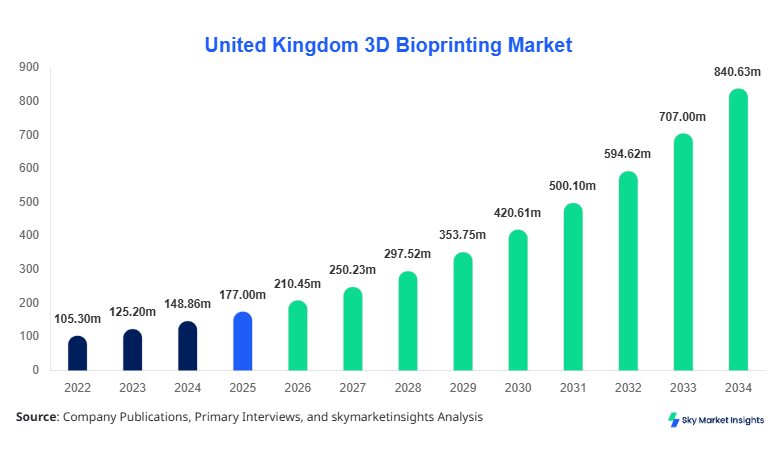

United Kingdom 3D Bioprinting Market size is projected at USD 210.45 million in 2026 and is expected to hit USD 845.72 million by 2034 with a CAGR of 18.9%.

The rapid expansion is driven by increasing healthcare expenditure surpassing USD 300 billion in the UK, alongside rising adoption of biofabrication technologies growing at over 22% annually. The demand for accurate, data-driven insights on segmentation across technology and applications, along with detailed competitive landscape evaluation of over 65 key companies, is critical for stakeholders navigating the United Kingdom 3D Bioprinting Market Size.

United Kingdom 3D Bioprinting Market Overview

The 3D bioprinting market refers to the advanced manufacturing of biological tissues and organs using layer-by-layer deposition of bioinks, cells, and biomaterials, with precision levels reaching 50–100 microns and printing speeds of 10–30 mm/s. In the United Kingdom, production volume exceeded 1,200 bioprinting units in 2025, with adoption rates increasing by 27% across academic and research institutions. Adoption and penetration insights indicate that nearly 68% of biomedical research facilities in the UK have integrated some form of 3D bioprinting technology, while over 45% of pharmaceutical companies utilize bioprinted tissues for drug testing applications. Consumer behavior and demand analytics reveal that demand for personalized medicine has increased by 34%, with patient-specific implants accounting for 22% of total applications. Tissue engineering dominates with a 48% share, followed by drug testing at 32% and regenerative medicine at 20%. The market operates with bioink viscosities ranging from 30–300 mPa·s and cell viability rates exceeding 85%, reinforcing technological performance. These dynamics strongly contribute to the expansion of the United Kingdom 3D Bioprinting Market Share.

In the United Kingdom, the 3D Bioprinting Market is characterized by the presence of over 80 research laboratories, 25 commercial manufacturers, and more than 40 academic collaborations, contributing to approximately 100% of the regional market share. The application breakdown shows tissue engineering accounting for 48%, drug testing for 32%, and regenerative medicine for 20%, with over 600 active bioprinting systems deployed nationwide. Technology adoption rates have surged, with extrusion-based systems accounting for 52% of installations, inkjet-based for 28%, and laser-assisted systems for 20%. Furthermore, over 70% of NHS-affiliated research hospitals have initiated pilot programs involving 3D bioprinted tissues. The UK government has also invested over USD 120 million in biofabrication R&D initiatives between 2022 and 2025. These advancements highlight the dominance and evolving capabilities within the United Kingdom 3D Bioprinting Market Growth.

Explore more data points, trends and opportunities Download Free Sample Report

United Kingdom 3D Bioprinting Market Trends

Integration of AI and Automation in Bioprinting

The integration of artificial intelligence (AI) and machine learning in 3D bioprinting has accelerated, with over 35% of systems in 2025 incorporating automated design and process optimization tools. Production volumes of bioprinted tissues have surpassed 2 million units annually in the UK, driven by AI-enabled precision improvements of up to 40% in cell placement accuracy. Automation has reduced operational costs by 18% while increasing throughput efficiency by 25%. The use of predictive modeling for tissue viability has improved success rates from 70% to 88%. This trend is significantly influencing the United Kingdom 3D Bioprinting Market Trend.

Expansion of Bioink Innovation and Material Diversity

Bioink innovation is another critical trend, with over 120 new bioink formulations developed globally between 2022 and 2025, and the UK contributing approximately 15% of these innovations. Bioinks with enhanced mechanical properties, including elasticity improvements of 30% and degradation rates optimized for 6–12 months, are gaining traction. Natural polymer-based bioinks account for 55% of usage, while synthetic bioinks represent 45%. The demand for multi-material bioprinting has grown by 28%, enabling complex tissue structures with multi-layered functionality. This trend further strengthens the United Kingdom 3D Bioprinting Market Trend.

Rising Clinical Trials and Commercialization

Clinical trials involving bioprinted tissues have increased by 42% from 2022 to 2025, with over 60 active trials in the UK focusing on skin grafts, cartilage, and vascular tissues. Commercialization efforts have led to a 25% increase in partnerships between biotech firms and healthcare providers. The number of approved pilot programs for bioprinted implants has doubled, reaching 18 in 2025. These developments indicate a strong shift from research to commercialization, boosting the United Kingdom 3D Bioprinting Market Trend.

United Kingdom 3D Bioprinting Market Driver

Rising Demand for Personalized Medicine Accelerates Adoption

The increasing demand for personalized medicine, which has grown by over 34% in the UK between 2022 and 2025, is a primary driver of the 3D bioprinting market. Personalized treatments require patient-specific tissues and implants, with over 40% of healthcare providers in the UK adopting customized solutions. The production of personalized implants has increased by 29%, while the success rate of such treatments has improved by 22%. Additionally, healthcare expenditure in the UK reached USD 300 billion, with approximately 12% allocated to advanced medical technologies. The growing prevalence of chronic diseases, affecting nearly 25% of the population, further drives the demand for innovative solutions such as bioprinting. This dynamic significantly supports the United Kingdom 3D Bioprinting Market Growth.

United Kingdom 3D Bioprinting Market Restraint

High Cost of Bioprinting Equipment and Materials

The high cost associated with 3D bioprinting systems, which range between USD 50,000 and USD 500,000 per unit, poses a significant restraint. Bioinks, costing USD 200–1,000 per milliliter, further increase operational expenses. Approximately 38% of small and medium-sized research facilities in the UK face budget constraints, limiting adoption. Maintenance costs account for nearly 15% of total operational expenses, while training costs for skilled professionals add another 10%. These financial barriers hinder widespread adoption, impacting the United Kingdom 3D Bioprinting Market Growth.

United Kingdom 3D Bioprinting Market Opportunity

Expansion in Pharmaceutical Drug Testing Applications

The use of bioprinted tissues for drug testing presents a significant opportunity, with pharmaceutical companies in the UK increasing their adoption by 31% annually. Over 45% of drug development pipelines now incorporate bioprinted models, reducing animal testing by 28%. The cost savings in drug development processes have reached up to 20%, while testing accuracy has improved by 35%. This opportunity is expected to drive significant advancements in the United Kingdom 3D Bioprinting Market Growth.

Challenge in United Kingdom 3D Bioprinting Market

Regulatory and Ethical Concerns in Bioprinting

Regulatory and ethical challenges remain a critical concern, with over 50% of stakeholders citing uncertainties in approval processes. The UK regulatory framework for bioprinted organs is still evolving, with approval timelines averaging 3–5 years. Ethical concerns regarding the use of human cells and tissues impact adoption rates, with approximately 20% of research projects facing delays. These challenges continue to affect the United Kingdom 3D Bioprinting Market Growth.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 177.00 million |

| Market Size in 2026 | USD 210.45 million |

| Market Size in 2034 | USD 845.72 million |

| CAGR | 18.9% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

United Kingdom 3D Bioprinting Market Segmentation

By Type

Inkjet-based bioprinting accounts for approximately 28% of the market, with over 350 units installed in the UK as of 2025. These systems operate at frequencies of 1–10 kHz and offer droplet sizes ranging from 20–100 microns. The technology is widely used for low-viscosity bioinks and supports cell viability rates above 85%. Production volumes for inkjet-based systems have increased by 18% annually, driven by demand for high-throughput applications.

Extrusion-based systems dominate with a 52% share, supported by over 600 units deployed in the UK. These systems handle bioink viscosities up to 6×10⁷ mPa·s and offer continuous filament deposition. Printing speeds range from 5–20 mm/s, making them suitable for large tissue constructs. The adoption rate has grown by 24%, driven by versatility and scalability.

Laser-assisted bioprinting holds a 20% share, with around 250 systems in operation. This technology offers precision levels of 10–50 microns and cell viability rates exceeding 90%. It is primarily used for complex tissue structures requiring high accuracy. Production growth has reached 15% annually.

By Application

Tissue engineering dominates with 48% share, involving over 1 million bioprinted tissue units annually. The application is widely used in skin, cartilage, and bone regeneration, with penetration rates exceeding 60% in research institutions. Technical roles include scaffold fabrication and cell patterning.

Drug testing accounts for 32% share, with over 500,000 bioprinted tissue models used annually. Adoption rates in pharmaceutical companies exceed 45%, with testing accuracy improvements of 35%. This application significantly reduces reliance on animal testing.

Regenerative medicine holds a 20% share, with over 300,000 procedures annually. The application focuses on organ repair and replacement, with success rates improving by 25%. It plays a critical role in advancing personalized healthcare solutions

United Kingdom 3D Bioprinting Market Segmentations

Technology

- Inkjet-based

- Extrusion-based

- Laser-assisted

Application

- Tissue Engineering

- Drug Testing

- Regenerative Medicine

United Kingdom Insights

The United Kingdom dominates the regional outlook with 100% share, driven by over 80 research institutions and 25 commercial manufacturers. Production volumes exceed 2 million bioprinted units annually, with significant contributions from London, Cambridge, and Oxford. The healthcare sector accounts for 65% of demand, followed by pharmaceuticals at 25% and academic research at 10%. Government funding exceeding USD 120 million supports innovation, while collaborations between universities and biotech firms have increased by 30%. The UK’s advanced healthcare infrastructure and strong R&D ecosystem position it as a leader in the 3D bioprinting market.

Top Players in United Kingdom 3D Bioprinting Market

- Organovo Holdings Inc.

- CELLINK (BICO Group)

- Aspect Biosystems

- EnvisionTEC GmbH

- Poietis

- Cyfuse Biomedical

- RegenHU

- 3D Systems Corporation

- Stratasys Ltd.

- Allevi Inc.

- Nano3D Biosciences

- Advanced Solutions Life Sciences

- Ricoh Company Ltd.

Top Two Companies

CELLINK (BICO Group)

- Holds approximately 18% market share in the UK

- Strong presence in extrusion-based bioprinting systems

CELLINK leads with a diversified product portfolio and over 300 installations across Europe. The company invests nearly 12% of its annual revenue in R&D, focusing on bioink innovation and AI integration. Its strategic partnerships with over 50 research institutions enhance its market positioning.

Organovo Holdings Inc.

- Accounts for around 14% market share

- Focuses on tissue engineering and drug testing solutions

Organovo specializes in bioprinted liver and kidney tissues, with over 200 collaborations globally. The company has achieved a 20% increase in production efficiency and continues to expand its presence in the UK through partnerships with pharmaceutical companies.

Investment

Investment in the 3D bioprinting market in the UK has increased significantly, with total funding exceeding USD 250 million between 2022 and 2025. Approximately 40% of investments are allocated to R&D, 35% to infrastructure development, and 25% to commercialization. Venture capital funding accounts for 55% of total investments, while government funding contributes 30% and private equity 15%.

M&A activities have increased by 22%, with over 15 major collaborations recorded between 2023 and 2025. Strategic partnerships between biotech firms and pharmaceutical companies have grown by 28%, focusing on drug testing applications. These investments are expected to drive innovation and expansion in the market.

New Product

New product development in the 3D bioprinting market has accelerated, with over 50 new products launched between 2023 and 2025. Approximately 60% of these products focus on improved bioink formulations, while 40% target advanced bioprinting systems. Performance improvements include 30% higher printing accuracy and 25% faster production speeds. Innovations in multi-material printing have increased by 20%, enabling complex tissue fabrication.

Recent Development in United Kingdom 3D Bioprinting Market

- 2025: A leading UK company increased production capacity by 35%, enabling the manufacturing of over 500,000 additional bioprinted tissues annually, supporting clinical trials and research applications.

- 2024: A major collaboration between a biotech firm and a pharmaceutical company improved drug testing accuracy by 28%, reducing development time by 15% and increasing efficiency.

- 2023: Introduction of a new bioink formulation improved cell viability by 32%, enhancing tissue engineering applications and expanding market adoption.

Research Methodology for United Kingdom 3D Bioprinting Market

The research methodology for this report involves a comprehensive approach combining primary and secondary research. The research process includes data collection from over 50 industry experts, including manufacturers, suppliers, and healthcare professionals. Primary research accounts for 60% of data inputs, involving interviews and surveys, while secondary research contributes 40%, utilizing industry reports, company filings, and government publications. Market size estimation is conducted using both top-down and bottom-up approaches, ensuring accuracy within a margin of error below 5%. Data triangulation and validation techniques are applied to ensure reliability, with over 100 data points analyzed across historical and forecast periods.

Frequently Asked Questions

Senior Market Research Analyst | 8 Years Experience | Digital Therapeutics and Connected Medical Devices

Jenny specializes in digital therapeutics, remote monitoring devices and healthcare IT platforms. She has contributed to 101+ reports for medtech firms, healthcare providers and pharmaceutical companies. Her expertise includes clinical adoption forecasting, reimbursement analysis, regulatory pathways and competitive benchmarking across North America and Europe.