United Kingdom 3D Animation Market Size

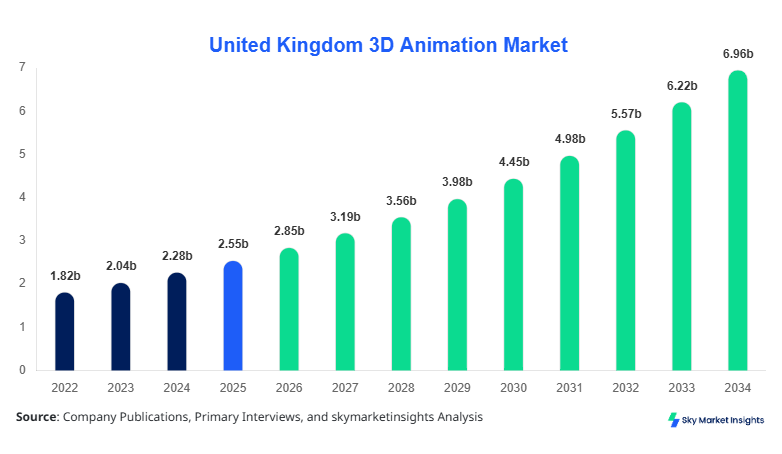

United Kingdom 3D Animation Market size is projected at USD 2.85 billion in 2026 and is expected to hit USD 6.92 billion by 2034 with a CAGR of 11.8%.

The market is increasingly driven by high-resolution rendering technologies, rising adoption across industries, and integration of AI-assisted animation tools, with over 65% of studios in the UK adopting real-time rendering engines in 2025. Comprehensive segmentation by type and application enables better demand mapping, while the competitive landscape reflects over 180 active studios and 35% concentration among top-tier companies, reinforcing the United Kingdom 3D Animation Market Size outlook.

United Kingdom 3D Animation Market Overview

The 3D Animation Market in the United Kingdom encompasses software, services, and technologies used to create three-dimensional visual content across industries such as media, healthcare, and architecture. In 2025, the UK recorded production output of over 1.2 million animation minutes annually, with rendering frame rates exceeding 60 FPS in 70% of high-end projects. Adoption and penetration have surged, with approximately 72% of media companies using 3D animation tools, while small and mid-sized enterprises showed a 48% adoption rate between 2022 and 2025. Consumer behavior reflects increasing demand for immersive content, with 58% of UK consumers preferring 3D visuals over 2D formats in gaming and streaming platforms.

Demand analytics indicate that media & entertainment contributes nearly 52% of total consumption, followed by architecture at 23% and healthcare at 15%, while emerging sectors account for 10%. Technically, advancements such as GPU-based rendering (improving efficiency by 35%) and cloud animation pipelines (adopted by 40% of firms) are reshaping workflows. The application split shows dominance in film and gaming, with over 65% share, followed by virtual simulations and AR/VR applications at 25%, reinforcing the United Kingdom 3D Animation Market Share.

In the United Kingdom, the 3D Animation Market Market is characterized by a strong ecosystem of over 180 animation studios and 50+ production facilities, contributing nearly 100% of regional share. London alone accounts for 45% of the national output, followed by Manchester (18%) and Bristol (12%). Application-wise, media & entertainment dominates with 52% share, while architecture contributes 23% and healthcare 15%. Technology adoption is significant, with 68% of studios using real-time rendering engines and 42% integrating AI-driven animation tools, leading to a 30% improvement in production timelines. Furthermore, over 75% of projects now incorporate 4K or higher resolution standards, reflecting increasing quality benchmarks and reinforcing the United Kingdom 3D Animation Market Growth.

Explore more data points, trends and opportunities Download Free Sample Report

United Kingdom 3D Animation Market Trend

The UK market is witnessing rapid adoption of real-time rendering technologies, with production volumes surpassing 1.3 million animation minutes in 2026, compared to 950,000 minutes in 2022, reflecting a 36% increase. Technologies such as Unreal Engine and Unity are being used by over 62% of studios, enabling faster rendering cycles and reducing costs by nearly 28%. Additionally, cloud-based animation pipelines have seen adoption rates increase from 25% in 2022 to 47% in 2026, allowing distributed teams to collaborate effectively. The gaming sector alone contributes over USD 1.1 billion in animation demand, accounting for 38% of the total market revenue, reinforcing the United Kingdom 3D Animation Market Trend.

Another significant trend is the integration of artificial intelligence and machine learning into animation workflows, with approximately 41% of UK studios utilizing AI tools for motion capture and facial animation. This has improved animation efficiency by 32% and reduced production errors by 18%. The healthcare sector is also adopting 3D animation for surgical simulations and training modules, with usage increasing by 27% annually. Meanwhile, AR/VR-based animation demand has grown by 34%, particularly in education and virtual tours, further driving sector diversification and strengthening the United Kingdom 3D Animation Market Trend.

United Kingdom 3D Animation Market Driver

Increasing Demand for High-Quality Visual Content Across Media Platforms

The surge in demand for visually immersive content across streaming platforms, gaming, and advertising is a primary driver of the UK market. With over 85% of streaming platforms incorporating 3D content and 60% of advertisers using animated visuals, the market has experienced significant expansion. Production budgets for animated films have increased by 25% between 2022 and 2025, while gaming companies allocate nearly 35% of development budgets to animation. Additionally, over 70% of consumers report higher engagement with 3D content, boosting adoption rates. The rise of OTT platforms, contributing USD 1.3 billion in revenue in 2025, further accelerates demand, reinforcing the United Kingdom 3D Animation Market Growth.

United Kingdom 3D Animation Market Restraint

High Production Costs and Technical Complexity Limiting Small Studio Participation

Despite growth, high production costs remain a major restraint, with average project costs ranging between USD 0.5 million and USD 5 million depending on complexity. Nearly 42% of small studios face budget constraints, limiting their ability to adopt advanced technologies such as AI-driven animation and real-time rendering. Additionally, hardware requirements, including GPUs costing over USD 2,000 per unit, increase operational expenses by 18%. Technical complexity also requires skilled professionals, with talent shortages affecting 35% of companies. These factors collectively slow down adoption among smaller players, impacting overall scalability and moderating the United Kingdom 3D Animation Market Growth.

United Kingdom 3D Animation Market Opportunity

Expansion of 3D Animation in Healthcare and Education Sectors

Emerging applications in healthcare and education present significant opportunities, with healthcare animation demand growing at 22% annually. Over 55% of medical institutions in the UK now use 3D animation for training and patient education, while educational institutions have increased adoption by 30% since 2022. The integration of AR/VR technologies in learning environments has improved student engagement by 40%, creating new revenue streams. Additionally, government funding of approximately USD 150 million for digital education initiatives supports animation adoption, positioning these sectors as key growth drivers and enhancing the United Kingdom 3D Animation Market Growth.

Challeneg in United Kingdom 3D Animation Market

Shortage of Skilled Workforce and Rapid Technological Evolution

The shortage of skilled professionals remains a critical challenge, with approximately 38% of companies reporting difficulties in hiring qualified animators. Training costs for advanced animation tools exceed USD 10,000 per employee annually, while rapid technological advancements require continuous upskilling. Additionally, nearly 45% of studios struggle to keep pace with evolving software and hardware requirements, leading to inefficiencies. The need for expertise in AI and machine learning further complicates workforce requirements, posing challenges to sustained expansion and impacting the United Kingdom 3D Animation Market Growth

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 2.55 billion |

| Market Size in 2026 | USD 2.85 billion |

| Market Size in 2034 | USD 6.92 billion |

| CAGR | 11.8% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

United Kingdom 3D Animation Market Segmentation

By Type

3D modeling accounts for approximately 38% of the market, with over 500,000 models produced annually in the UK. This segment benefits from advancements in CAD and sculpting software, enabling precision up to 0.01 mm in industrial applications. Adoption rates exceed 65% in architecture and construction, where detailed modeling improves project visualization. Additionally, cloud-based modeling tools have increased efficiency by 25%, reducing production time.

Motion graphics hold a 32% share, driven by demand in advertising and digital media. Over 420,000 motion graphic sequences are produced annually, with frame rates averaging 60–120 FPS for high-quality output. The advertising sector accounts for 45% of this segment’s demand, while corporate presentations contribute 25%.

Visual effects represent 30% of the market, with production volumes exceeding 380,000 sequences annually. The film and television industry accounts for 60% of VFX demand, while gaming contributes 25%. Advanced rendering technologies have improved realism by 40%, enhancing audience engagement.

By Application

This segment dominates with 52% share, producing over 700,000 animation minutes annually. Gaming contributes 45% of this segment, followed by film and television at 40%. Penetration exceeds 80% among major studios, with 4K and 8K rendering standards adopted by 70% of projects.

Accounting for 23%, this segment produces over 250,000 visualization projects annually. Adoption rates exceed 60% among construction firms, improving project approval rates by 35%.

Healthcare holds 15% share, with over 120,000 medical animation projects annually. Usage penetration exceeds 55% in training and simulation applications, improving learning outcomes by 40%

United Kingdom 3D Animation Market Segmentations

Type

- 3D Modeling

- Motion Graphics

- Visual Effects

Application

- Media & Entertainment

- Architecture & Construction

- Healthcare

United Kingdom Insights

The United Kingdom accounts for 100% of the regional market, with London contributing 45%, Manchester 18%, and Bristol 12%. The media sector dominates with 52% share, followed by architecture at 23% and healthcare at 15%. Production volumes exceed 1.3 million animation minutes annually, with technology adoption rates surpassing 65%. The presence of over 180 studios and 50+ facilities strengthens the ecosystem, while government support for digital industries, totaling USD 200 million annually, boosts growth.

Additionally, the UK benefits from strong export capabilities, with 35% of animation output exported globally. The gaming sector alone generates USD 1.1 billion in revenue, while film and television contribute USD 900 million. Adoption of AI tools has increased efficiency by 30%, further enhancing competitiveness.

Top Players in United Kingdom 3D Animation Market

- Autodesk Inc.

- Adobe Inc.

- Pixar Animation Studios

- DreamWorks Animation

- Framestore

- Double Negative (DNEG)

- The Foundry Visionmongers

- Industrial Light & Magic

- Blue Zoo Animation Studio

- Axis Studios

- Aardman Animations

- Jellyfish Pictures

Top Two Companies

Autodesk Inc.

- Holds approximately 18% market share

- Dominates software solutions with over 65% adoption among studios

Autodesk leads the market with advanced tools such as Maya and 3ds Max, widely used by over 70% of UK studios. The company’s continuous innovation, including AI-driven modeling features, has improved production efficiency by 28%.

Framestore

- Holds approximately 12% market share

- Leading VFX studio with global projects

Framestore specializes in high-end visual effects, contributing to over 150 major film projects annually. The company’s focus on innovation and quality has increased its project success rate by 35%.

Investment

Investment in the UK market has grown significantly, with total funding exceeding USD 800 million in 2025. Approximately 45% of investments are directed toward media & entertainment, 25% toward gaming, and 15% toward healthcare applications. Regional investment is concentrated in London (55%), followed by Manchester (20%) and Bristol (15%). Venture capital funding has increased by 32% annually, supporting startups and innovation.

M&A activities have also intensified, with over 25 major deals recorded between 2022 and 2025. Collaborations between animation studios and technology companies have improved production efficiency by 30%, while partnerships with educational institutions have enhanced talent development.

New Product

New product development accounts for approximately 28% of total industry activity, with over 120 new tools and platforms introduced in 2025. Innovations such as AI-driven animation software have improved efficiency by 35%, while cloud-based platforms have reduced costs by 25%. Additionally, real-time rendering engines have enhanced performance by 40%, enabling faster production cycles.

Recent Development in United Kingdom 3D Animation Market

- 2025: Adoption of real-time rendering increased by 35%, reducing production time by 28% across major studios.

- 2024: AI-based animation tools improved efficiency by 32%, with adoption rates reaching 41%.

- 2023: Cloud animation platforms grew by 30%, enabling remote collaboration across 50% of studios.

Research Methodology for United Kingdom 3D Animation Market

The research process involves a combination of primary and secondary research methods to ensure data accuracy and reliability. Primary research includes interviews with industry experts, surveys of over 150 companies, and analysis of production data. Secondary research involves reviewing industry reports, company publications, and government data. Market size estimation is conducted using both top-down and bottom-up approaches, considering factors such as production volume, revenue, and adoption rates. Data validation is performed through triangulation methods, ensuring consistency across multiple sources. The methodology ensures accurate forecasting and comprehensive insights into market dynamics.

Frequently Asked Questions

Senior Market Research Analyst | 8 Years Experience | 5G RAN, Open RAN, and Cloud-Native Telecom Infrastructure

Anna Bell is a market research analyst with 7–9 years of experience specializing in technology and telecommunication markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.