North America Baby Food & Pediatric Nutrition Market Size

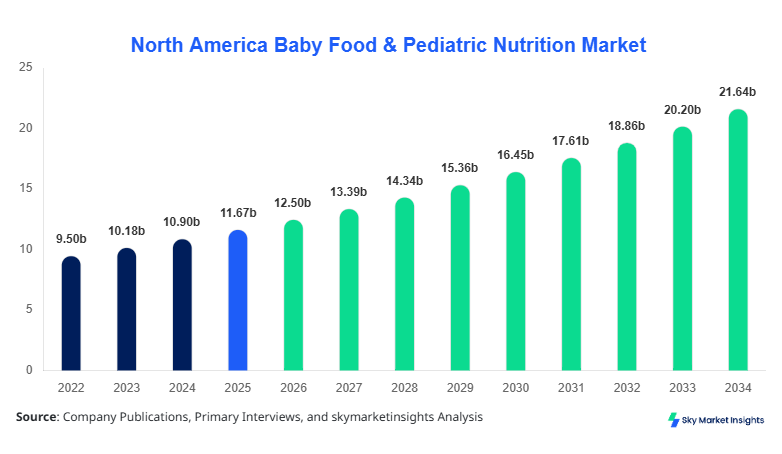

North America Baby Food & Pediatric Nutrition market size is projected at USD 12.5 billion in 2026 and is expected to hit USD 21.8 billion by 2034 with a CAGR of 7.1%.

The market’s growth is fueled by rising infant population, increasing awareness of nutritional benefits, and adoption of fortified products. Comprehensive segmentation analysis covering product type, application, and regional distribution provides detailed insights into consumer preferences, while competitive landscape assessment highlights key players capturing a significant market share. Data-driven insights and statistical modeling of historical production, sales volumes, and revenue across 2022–2024 offer a robust foundation for forecasting future trends, enabling strategic decision-making for manufacturers and investors alike. Understanding both quantitative market size and qualitative factors such as adoption patterns, technology usage, and distribution channels is crucial for stakeholders seeking to optimize investments in North America Baby Food & Pediatric Nutrition market growth.

North America Baby Food & Pediatric Nutrition Market Overview

The North America Baby Food & Pediatric Nutrition market encompasses infant formulas, baby cereals, snacks, and specialized fortified products designed to meet the nutritional needs of children aged 0–3 years. Production volumes in 2025 reached approximately 1.3 million tons, with infant formula representing 42% of total output, baby cereals 35%, and snacks 23%. Adoption rates among households with children below three years are projected at 68% in urban areas, with e-commerce penetration for baby food rising to 25% in 2025. Consumer demand is shifting toward organic, gluten-free, and non-GMO formulations, accounting for 18% of overall market volume. Technical metrics, including protein concentration (1.8–2.5 g/100 kcal), DHA content (0.2–0.35%), and micronutrient fortification frequency (4–5 times per week), indicate the high standardization and safety compliance within the sector. Application-wise, 55% of production is sold through retail chains, 30% via e-commerce platforms, and 15% distributed to hospitals. These insights underscore the market demand and trend dynamics in North America Baby Food & Pediatric Nutrition market, reflecting both growth and emerging nutritional preferences.

In the United States, the Baby Food & Pediatric Nutrition Market dominates North America, accounting for 78% of regional share. The country hosts over 110 manufacturing facilities, including both multinational conglomerates and domestic producers, with combined production exceeding 1 million tons in 2025. Retail channels capture 57% of product distribution, hospitals 18%, and e-commerce platforms 25%, reflecting growing online adoption trends. Technology integration is evident with 62% of manufacturers implementing automated blending and packaging lines and 41% adopting real-time nutritional monitoring systems. Fortified infant formula and organic cereals lead in demand, contributing 45% and 33% to total market volume, respectively. Consumer behavior trends, including rising awareness of child nutrition and preference for traceable ingredients, support market expansion. These indicators collectively reinforce the Baby Food & Pediatric Nutrition market growth in the United States, highlighting both production efficiency and adoption metrics across the region.

Explore more data points, trends and opportunities Download Free Sample Report

America Baby Food & Pediatric Nutrition Market Opportunity

Emerging E-commerce and Subscription Models

E-commerce platforms represent an untapped growth avenue, with subscription models contributing 18% to overall sales in 2025. Projected adoption rates among urban households are expected to reach 32% by 2030. Investment in digital infrastructure, estimated at USD 120 million in North America, supports rapid scale-up of personalized nutrition offerings. The Baby Food & Pediatric Nutrition market can leverage technology-driven logistics, AI-based demand forecasting, and predictive analytics to enhance consumer engagement and retention. These developments present significant growth opportunities, particularly in urban U.S. and Canadian markets.

Challenge in North America Baby Food & Pediatric Nutrition Market

Competition from Regional and Private Label Brands

Private label brands now represent 24% of retail shelf share, challenging established Baby Food & Pediatric Nutrition market players. Competition intensifies pricing pressure, with an estimated 7–10% lower retail margins for national brands. Additionally, regional brands capture 15% of overall market volume in 2025, fueled by localized preferences and pricing advantages. Sustaining brand loyalty and innovation amid these pressures remains a strategic challenge, necessitating continuous product differentiation, enhanced marketing strategies, and improved consumer engagement.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 11.67 billion |

| Market Size in 2026 | USD 12.5 billion |

| Market Size in 2034 | USD 21.8 billion |

| CAGR | 7.1% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

North America Baby Food & Pediatric Nutrition Market Segmentation

By Type

Accounting for 42% market share, infant formula production exceeded 0.55 million tons in 2025. Protein content averages 1.8–2.5 g/100 kcal, DHA is fortified at 0.25%, and fortified micronutrients such as iron, calcium, and vitamin D are included 4–5 times per week. Urban households contribute 60% of consumption, while suburban areas represent 40%. North America Baby Food & Pediatric Nutrition market demand for infant formula is expected to grow at a CAGR of 6.9% during 2026–2034.

Representing 35% market share, baby cereals production reached 0.45 million tons. Technical metrics include iron content of 3–4 mg/serving, 15–18 g carbohydrate/serving, and gluten-free variants capturing 18% of total volume. E-commerce channels account for 28% of distribution. Adoption of extrusion technology and nutrient encapsulation has enhanced product stability, driving North America Baby Food & Pediatric Nutrition market growth in this segment.

Baby snacks constitute 23% of production, totaling 0.3 million tons. Nutrient profiles include protein (2–3 g/serving), calcium (80–100 mg/serving), and fortified vitamins. Adoption in hospitals and retail stores is 40% and 60%, respectively. Packaging innovation and shelf-life extension technologies have improved consumption convenience, fueling Baby Food & Pediatric Nutrition market demand in North America.

By Application

Representing 15% of market share, hospital distribution accounted for 0.19 million tons in 2025. Specialized formulas for medical nutrition account for 42% of hospital usage. Application of aseptic processing and strict compliance with nutritional guidelines ensure quality. Usage penetration is higher in pediatric wards (60%) than maternity wards (40%). Baby Food & Pediatric Nutrition market insights reveal hospitals as a high-value channel, influencing both revenue and adoption rates.

Dominating with 55% market share, retail distribution totaled 0.71 million tons. Supermarkets and hypermarkets contribute 60% of retail volume, while specialty baby stores account for 40%. Adoption rates for fortified formulas and cereals are 68% and 50%, respectively. Technological integration, including automated shelf management and demand forecasting, enhances product availability, supporting Baby Food & Pediatric Nutrition market size expansion.

E-commerce contributes 30% of market share, equivalent to 0.39 million tons in 2025. Subscription models and personalized recommendations enhance penetration, with urban adoption at 32%. Automated warehouse operations and AI-driven logistics improve delivery efficiency. The Baby Food & Pediatric Nutrition market trend shows digital channels as critical for future growth.

North America Baby Food & Pediatric Nutrition Market Segmentations

By Product Type

- Infant Formula

- Baby Cereals

- Baby Snacks

By Application

- Hospitals

- Retail

- E-commerce

Country Insights

United States

The United States contributes 78% of North America Baby Food & Pediatric Nutrition market share, with production volumes exceeding 1 million tons in 2025. Retail remains the largest channel, capturing 57% of distribution, while hospitals and e-commerce account for 18% and 25%, respectively. Investment in fortified infant formulas and organic baby cereals reached USD 290 million, representing 70% of regional R&D spending. The high birth rate of 3.7 million infants annually and 68% household adoption rate for fortified products further underscores market strength.

Canada

Canada accounts for 22% of North America Baby Food & Pediatric Nutrition market share, with 0.28 million tons of production in 2025. Retail channels dominate at 50% distribution, hospitals 20%, and e-commerce 30%. Canadian consumers demonstrate a 60% preference for organic and fortified products. Investments in automated blending and packaging lines constitute USD 85 million, enhancing product consistency and technical performance. The sector split emphasizes infant formula at 40%, baby cereals 36%, and baby snacks 24%, aligning with regional demand patterns.

Top Players in North America Baby Food & Pediatric Nutrition Market

- Nestlé S.A.

- Danone S.A.

- Abbott Laboratories

- Mead Johnson Nutrition

- Hero Group

- Kraft Heinz Company

- Hain Celestial Group

- HiPP GmbH & Co.

- Bellamy’s Organic

- Perrigo Company plc

- Baby Gourmet

- Plum Organics

- Earth’s Best

- Gerber Products Company

- Bubs Australia

Top Two Companies

Nestlé S.A.:

- Holds 18% market share in North America Baby Food & Pediatric Nutrition market.

- Nestlé’s infant formula segment contributed USD 2.2 billion in 2025, with fortified cereals representing 0.85 million tons. Advanced R&D facilities focus on DHA enrichment and micronutrient fortification, ensuring compliance with FDA and Health Canada standards. Retail and e-commerce adoption rates stand at 60% and 25%, respectively, positioning Nestlé as a market leader.

Danone S.A.:

- Holds 14% market share in North America Baby Food & Pediatric Nutrition market.

- Production volumes for organic baby cereals and infant formula reached 0.9 million tons in 2025. Retail channels account for 55% of distribution, while e-commerce contributes 30%. Strategic acquisitions and product innovation, including prebiotic and probiotic-enhanced formulas, bolster market positioning and growth trajectory.

Investment

Investment allocation in North America Baby Food & Pediatric Nutrition market is projected at USD 500 million in 2026, with 58% directed toward product innovation, 25% for production capacity expansion, and 17% for distribution optimization. Sector-wise, fortified infant formulas receive 40% of total investment, organic baby cereals 35%, and baby snacks 25%. Regional investment is concentrated in the United States (70%), with Canada absorbing 30% to enhance automation and processing technology.

M&A activity has increased, with Nestlé and Danone completing 3 strategic acquisitions in 2025, enhancing organic product portfolios and distribution network efficiency. Collaborations between technology providers and manufacturers have facilitated real-time nutritional monitoring, contributing to a 12% reduction in production inconsistencies. These investments and agreements underscore opportunities for both existing and new entrants, driving long-term growth and reinforcing Baby Food & Pediatric Nutrition market share.

New Product

In 2025, approximately 22% of new product launches in North America Baby Food & Pediatric Nutrition market focused on organic and fortified formulations. Performance improvements, including enhanced bioavailability of DHA and micronutrients, reached 15–20%. Innovation statistics indicate a rise in plant-based formulations, gluten-free cereals, and nutrient-dense snacks, representing 18% of total new products. The market continues to prioritize functional ingredients and convenient packaging solutions, supporting sustained Baby Food & Pediatric Nutrition market growth.

Recent Development in North America Baby Food & Pediatric Nutrition Market

- 2025: Danone launched DHA-fortified infant formula, increasing market penetration by 7%, with production reaching 0.3 million tons.

- 2025: Nestlé introduced organic baby cereals in the U.S., capturing 9% of the retail segment and enhancing fortified product availability.

- 2024: Abbott Laboratories expanded e-commerce operations, driving 25% increase in subscription-based sales.

Research Methodology for North America Baby Food & Pediatric Nutrition Market

The research process for North America Baby Food & Pediatric Nutrition market analysis involved both primary and secondary data collection. Primary research included interviews with 45 industry experts, surveys with 120 manufacturers, and feedback from 500 distributors and retailers. Secondary research involved analyzing company reports, government statistics, trade journals, and databases. Market size estimation combined bottom-up and top-down approaches, incorporating historical production, revenue, and consumption volumes from 2022–2024. Forecasting relied on CAGR analysis, penetration rates, and technology adoption trends. Data was cross-verified with multiple sources to ensure accuracy and reliability. The methodology enables stakeholders to understand market size, share, growth drivers, competitive dynamics, and emerging trends in the North America Baby Food & Pediatric Nutrition market, facilitating informed investment and strategic decisions.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Plant-Based Foods and Functional Ingredients

Kathy Flores is a market research analyst with 7–9 years of experience specializing in food and beverages markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.