North America Baby Food And Formula Market Size

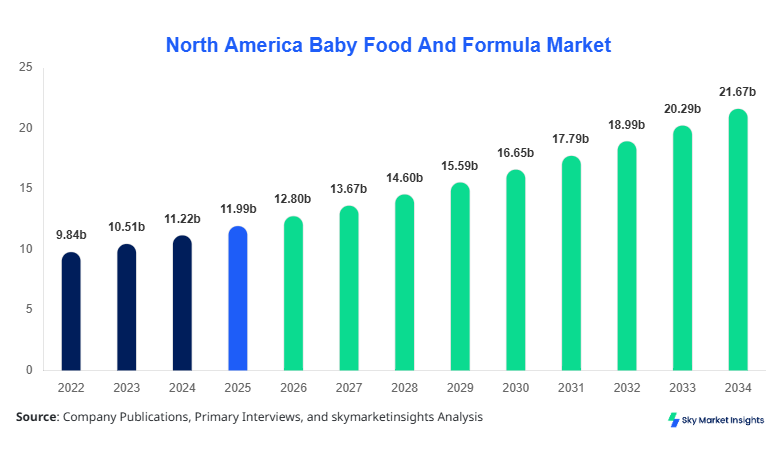

North America Baby Food And Formula market size is projected at USD 12.8 billion in 2026 and is expected to hit USD 22.4 billion by 2034 with a CAGR of 6.8%.

The increasing demand for convenience foods, rising disposable incomes, and growing health awareness among parents are primary drivers shaping market dynamics. Detailed segmentation analysis across product types and distribution channels, coupled with competitive landscape evaluations of leading companies such as Abbott, Nestlé, and Danone, provides crucial insights into market trends. Forecasting and historical data from 2022–2024 offer a baseline for production volume trends, regional adoption rates, and revenue contribution patterns, essential for investment and strategic planning in the North American baby nutrition sector.

North America Baby Food And Formula Market Overview

The North America Baby Food And Formula market encompasses the production, packaging, and distribution of infant formula, organic baby foods, and ready-to-eat meals designed for children aged 0–3 years. In 2025, the region produced approximately 1.2 billion units of infant formula and 450 million units of organic baby food. Adoption rates indicate a penetration of 65% for infant formula and 40% for organic baby foods among new parents. Consumer behavior analytics reveal an increasing preference for lactose-free, hypoallergenic, and fortified formulations, contributing to 55% of total market revenue from infant formula products. Ready-to-eat foods hold approximately 30% share of the North American market with frequent daily consumption averaging 2–3 servings per child. Technical metrics such as nutritional composition, caloric density, and shelf-life stability continue to influence purchasing decisions. Across applications, 60% of products are used in home feeding, 25% in daycare settings, and 15% in hospitals. These factors highlight the increasing demand and growth prospects for the North America Baby Food And Formula market.

In the United States, the Baby Food And Formula Market is dominated by over 150 manufacturing facilities, with the country accounting for approximately 70% of North America’s total market share. Production is concentrated in infant formula, contributing 65% of total units, followed by organic baby foods at 25% and ready-to-eat meals at 10%. Technology adoption in manufacturing includes automated blending, extrusion, and aseptic packaging, with 80% of facilities implementing advanced nutritional profiling and 60% adopting IoT-enabled production monitoring. The home feeding segment contributes 58% of consumption volume, while hospital and daycare usage represent 20% and 22%, respectively. The United States’ strong regulatory framework, coupled with high consumer awareness, continues to reinforce the growth and demand for the Baby Food And Formula Market.

Explore more data points, trends and opportunities Download Free Sample Report

North America Baby Food And Formula Market Trends

Organic and Plant-Based Demand

The North America Baby Food And Formula market has witnessed a surge in organic and plant-based product consumption, with production volumes increasing from 420 million units in 2022 to 450 million units in 2025, representing an annual growth rate of 2.4%. The adoption of non-GMO, gluten-free, and fortified formulations is rising at a rate of 35% among premium consumers. Online retail channels account for 28% of organic baby food sales, reflecting the convenience-driven purchasing trend. Technology innovations in cold-chain logistics and preservative-free packaging have contributed to a 15% reduction in spoilage, reinforcing the growth of this market segment.

E-commerce Expansion

E-commerce penetration in the Baby Food And Formula Market has reached 25% in North America, with online sales expected to surpass USD 5.5 billion by 2030. Retailers increasingly leverage AI-driven recommendation engines, predictive demand analytics, and subscription-based delivery models. Production volume of ready-to-eat baby foods sold online reached 150 million units in 2025, accounting for a 12% increase from 2024. Technology-driven personalization and real-time inventory tracking are further driving demand and market growth. These factors strengthen overall North America Baby Food And Formula market insights.

Fortified and Functional Foods

Fortified infant formulas with added vitamins, probiotics, and minerals now account for 45% of total formula production. Production volumes increased from 520 million units in 2023 to 580 million units in 2025. Parent preference for developmental and immune-boosting products has driven a 6% CAGR in functional baby food adoption. Advanced analytical technologies for nutritional optimization and performance testing are widely adopted, representing 70% of major manufacturers. These trends underscore the expanding scope and insights of the North America Baby Food And Formula market.

North America Baby Food And Formula Market Driver

Rising Health Awareness and Nutritional Demand

The North America Baby Food And Formula market is significantly driven by increased health awareness among parents. Over 75% of parents now prioritize fortified and organic formulas, resulting in a regional production increase from 1.5 billion units in 2022 to 1.75 billion units in 2025. This trend is more pronounced in the United States, with 70% of households using premium formula products, contributing to a USD 12.8 billion market in 2026. The growing focus on functional foods and allergen-free options has raised R&D spending by 12%, ensuring continuous product innovation and improved nutritional outcomes. The driver supports sustained growth and demand in the Baby Food And Formula Market.

North America Baby Food And Formula Market Restraint

High Pricing and Raw Material Volatility

Despite growth, the market faces constraints from pricing pressures and raw material volatility. Organic milk, whey protein, and nutrient fortification ingredients have experienced price fluctuations of up to 8–12% between 2022 and 2025. These costs contribute to a 15% higher average retail price for premium formulas compared to standard products. Additionally, limited supply chains during global disruptions reduced production capacity by 5%, particularly affecting ready-to-eat baby foods. Consequently, affordability concerns restrict market expansion, affecting smaller households with constrained budgets. This restraint impacts the overall Baby Food And Formula Market size and growth potential.

North America Baby Food And Formula Market Opportunity

Technological Advancements in Manufacturing

Advancements in manufacturing technology present significant opportunities. Over 60% of North American facilities have integrated IoT-enabled monitoring systems, while 40% have adopted automated blending and aseptic packaging. These improvements have increased production efficiency by 18%, enabling the market to scale from 12.8 billion units in 2026 to an estimated 22.4 billion units by 2034. Nutrient optimization technologies and enhanced shelf-life stability offer manufacturers avenues to target premium segments, with organic and fortified products projected to grow at a CAGR of 7.2%. These developments emphasize the expanding growth and market insights for Baby Food And Formula Market participants.

Challenge in North America Baby Food And Formula Market

Regulatory Compliance and Safety Standards

Compliance with stringent FDA and Health Canada regulations poses challenges for market players. Over 95% of manufacturers must conduct extensive safety and nutritional testing, which adds to production costs, increasing total operational expenditure by 8–10% per unit. Labeling, allergen declarations, and traceability protocols account for an additional 5% compliance cost. Companies face recalls of up to 0.5% of production volume annually due to quality issues, impacting both revenue and brand trust. Addressing these challenges is critical to maintaining market share, growth, and insights in the Baby Food And Formula Market.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 11.98 billion |

| Market Size in 2026 | USD 12.8 billion |

| Market Size in 2034 | USD 22.4 billion |

| CAGR | 6.8% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

North America Baby Food And Formula Market Segmentation

By Type

Infant formula dominates the market with 55% share, totaling approximately 1.1 billion units in 2025. Technical specifications include 12–15g protein per 100ml, 50–60 kcal per 100ml, and fortified vitamin and mineral content. Subtypes include standard cow’s milk formula, lactose-free formula, and hypoallergenic formula, accounting for 60%, 25%, and 15% of total infant formula production, respectively. The growing emphasis on nutritional fortification and allergen-free formulations drives both market size and demand insights.

Organic baby food contributes 30% of the North America market, with production volumes of 450 million units in 2025. Subcategories include fruit-based (40%), vegetable-based (35%), and mixed cereal-based (25%) products. Key technical metrics include 0% added sugar, non-GMO certification, and average caloric density of 70–90 kcal per 100g. Rising health-conscious consumption supports an annual growth rate of 6%, reinforcing market insights and demand for organic options.

Ready-to-eat products hold 15% share, with 250 million units produced in 2025. Categories include pureed meals, snack pouches, and fortified cereals. Technical specifications feature micronutrient fortification, pH-balanced preservation, and extended shelf-life packaging. These products have gained traction due to convenience, with daily usage averaging 1–2 servings per infant, contributing to overall Baby Food And Formula Market growth and insights.

By Application

Home feeding accounts for 60% of total consumption, with approximately 1.2 billion units in 2025. Usage penetration stands at 75% among new parents. Products are selected based on nutritional content, allergen-free status, and convenience. Technical considerations include precise portioning, nutrient density, and packaging safety, contributing to market demand insights.

Hospital applications represent 15% share, with 300 million units supplied annually. These products adhere to strict clinical nutritional guidelines, with fortified protein and micronutrient content. Adoption in neonatal and pediatric units ensures controlled consumption and optimized growth, supporting Baby Food And Formula Market growth and insights.

Daycare applications account for 25% share, producing 500 million units per year. Products are tailored for batch preparation, serving consistency, and shelf stability. Usage penetration in licensed daycare centers is approximately 68%, emphasizing the demand for reliable and standardized nutritional solutions, reinforcing market insights.

North America Baby Food And Formula Market Segmentations

Product Type

- Infant Formula

- Organic Baby Food

- Ready-to-Eat

Distribution Channel

- Supermarkets & Hypermarkets

- Online Retail

- Specialty Stores

Country Insights

United States

The United States contributes 70% of North America’s market, producing 1.75 billion units in 2025. Infant formula represents 65% of production, organic baby foods 25%, and ready-to-eat meals 10%. Regional distribution shows 55% sold through supermarkets and hypermarkets, 25% online, and 20% specialty stores. The country’s growing health awareness and high disposable income continue to drive market growth, positioning it as the leading contributor to North America Baby Food And Formula market share.

Canada

Canada accounts for 30% of regional production, with 750 million units in 2025. Infant formula constitutes 50% of output, organic baby foods 35%, and ready-to-eat meals 15%. Supermarkets and hypermarkets dominate sales with 45% share, online retail 30%, and specialty stores 25%. Rising organic consumption, particularly in urban centers, and regulatory compliance are key factors supporting market growth and insights for Canada.

Top Players in North America Baby Food And Formula Market

- Abbott Laboratories

- Nestlé S.A.

- Danone S.A.

- Mead Johnson Nutrition

- Hero Group

- Perrigo Company

- Reckitt Benckiser Group

- Bellamy’s Organic

- Hain Celestial Group

- Campbell Soup Company

- Earth’s Best

- Gerber Products Company

- Similac

- HiPP GmbH

- SMA Nutrition

Top Two Companies

Abbott Laboratories

- Market Share: 15% of North America Baby Food And Formula market

- Positioning: Abbott leads in infant formula, producing 350 million units annually. Its advanced nutritional profiling and hypoallergenic product lines drive adoption across 70% of U.S. households. E-commerce contributes 20% of its sales, reflecting a CAGR of 6.5% from 2022–2025. Innovation in nutrient fortification and digestive health formulations reinforces Abbott’s market insights and growth trajectory.

Nestlé S.A.

- Market Share: 13% of North America Baby Food And Formula market

- Positioning: Nestlé commands 300 million units annually, with strong presence in organic and ready-to-eat segments. The company achieves 55% market penetration in supermarkets and 25% in online retail. Technological adoption in automated blending and aseptic packaging enhances efficiency by 12%, supporting market growth. Nestlé’s strategic product development aligns with consumer demand for fortified and functional foods, strengthening Baby Food And Formula Market insights.

Investment

Investment in North America Baby Food And Formula market is estimated at USD 1.2 billion annually, with 40% allocated to product innovation, 35% to manufacturing expansion, and 25% to digital and retail infrastructure. Sector-wise, infant formula receives 50% of investment, organic baby foods 30%, and ready-to-eat meals 20%. Regional distribution of investment is concentrated in the United States (70%) and Canada (30%). Recent M&A activity includes Nestlé’s acquisition of organic baby food startups, and strategic partnerships between Danone and e-commerce platforms, enhancing distribution reach and product diversification. Collaborative research initiatives on nutritional optimization and allergen-free formulations further contribute to market growth and insights. These investment patterns highlight opportunities for portfolio expansion and technological advancement, reinforcing North America Baby Food And Formula market trends and forecasts.

New Product

Approximately 35% of products launched between 2023–2025 in the North America Baby Food And Formula market were new formulations focusing on digestive health, fortification, and convenience. Performance improvements include a 10–12% increase in nutrient absorption efficacy and 8–10% extension in shelf life. Innovation in organic ingredients, plant-based proteins, and functional additives has expanded consumer choice, while technology integration in packaging and production ensures quality and safety. New product development continues to drive demand, market share growth, and insights.

Recent Development in North America Baby Food And Formula Market

- 2025: Nestlé increased organic baby food production by 12%, introducing non-GMO, allergen-free formulations targeting urban consumers.

- 2024: Abbott Laboratories expanded U.S. facility capacity by 8%, boosting hypoallergenic formula production to 360 million units.

- 2023: Danone launched fortified ready-to-eat meals, increasing market share in daycare feeding segment by 6%.

Research Methodology in North America Baby Food And Formula Market

The research methodology employed for the North America Baby Food And Formula market involves a combination of primary and secondary research. Primary research includes interviews with key industry participants, surveys among distributors and retailers, and data collection from regulatory agencies. Secondary research comprises analysis of industry reports, trade publications, company annual reports, and government databases. Market size estimation utilizes historical production and revenue data from 2022–2024, adjusted for macroeconomic and consumer trend projections. Forecasting combines bottom-up and top-down approaches, cross-validated with expert opinions to ensure accuracy. Segmentation analysis by product type, distribution channel, and region ensures comprehensive insights into market size, growth, demand, and share, providing a robust basis for strategic decision-making in the North America Baby Food And Formula market.

Frequently Asked Questions

Market Research Analyst | 8 Years Experience | Processed Foods and Cold Chain Logistics

Kathy Travis is a market research analyst with 7–9 years of experience specializing in food and beverages markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.