North America Baby Food And Drink Market Size

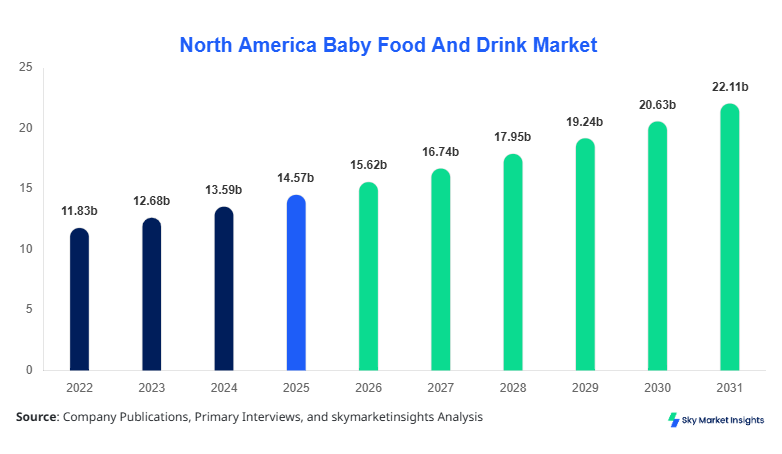

North America Baby Food And Drink market size is projected at USD 15.62 billion in 2026 and is expected to hit USD 28.47 billion by 2034 with a CAGR of 7.2%.

The market demand is driven by rising health consciousness among parents, increasing dual-income households, and technological advancements in nutrition delivery. Accurate data collection is critical to understand segmentation, competitive positioning, and growth drivers, including market penetration in both the United States and Canada. Analysis of production, consumption, and trade statistics is essential to provide actionable insights, while monitoring the competitive landscape across top manufacturers ensures a comprehensive market outlook. This report covers historical years 2022–2024, providing granular market data and forecasts through 2034, reinforcing the North America Baby Food And Drink market insights and growth.

North America Baby Food And Drink Market Overview

The North America Baby Food And Drink market comprises products formulated for infants and toddlers, including infant formulas, baby cereals, and complementary baby snacks. In 2025, total production reached 1.85 million tons across the United States and Canada, with infant formula accounting for 42% of total output, cereals 35%, and snacks 23%. Adoption rates among households with children aged 0–3 years reached 78%, with penetration higher in urban centers at 85%. Consumer behavior trends indicate a 22% year-on-year increase in organic and fortified baby foods, while frequency of usage averages 3–4 servings per day. Home applications dominate with 65% contribution, hospitals represent 20%, and retail/commercial outlets account for 15%. Technical performance metrics such as shelf-life stability, protein fortification levels, and micronutrient retention are closely monitored, reinforcing the North America Baby Food And Drink market demand and insights. Key market growth is also influenced by enhanced nutritional labeling and regulatory compliance.

Explore more data points, trends and opportunities Download Free Sample Report

North America Baby Food And Drink Market Trends

Shift Toward Organic and Fortified Products

The North America Baby Food And Drink market has seen organic baby food production rise from 0.42 million tons in 2022 to 0.58 million tons in 2025, representing a CAGR of 10.2%. Fortified infant formulas now represent 36% of total market volume, reflecting parental preference for enhanced nutrition. Technology adoption for nutrient preservation has reached 55%, with automated blending and cold-press techniques being implemented by 42% of manufacturers. Retail demand for organic cereals increased 15% in volume terms year-on-year, reinforcing Baby Food And Drink market insights and growth trends.

E-commerce and Direct-to-Consumer Channels

E-commerce channels now account for 28% of total sales, up from 18% in 2022, with digital platforms enabling 24/7 availability of baby food products. Production volumes supporting online sales reached 0.41 million tons in 2025, with home applications dominating 72% of online orders. Subscription-based models for infant nutrition products saw a 34% adoption rate, boosting recurring revenue streams. This trend emphasizes technology integration and consumer convenience, reinforcing Baby Food And Drink market growth.

Personalized Nutrition and Functional Foods

Functional baby foods with added probiotics, prebiotics, and DHA have captured 19% of the total market in 2025, up from 12% in 2022. Production of functional cereals reached 0.33 million tons, with a projected 9.5% CAGR from 2026 to 2034. Hospitals and clinics contribute 18% of functional food uptake, emphasizing clinical adoption. Technology adoption for precision formulation and nutrient profiling reached 47%, reinforcing Baby Food And Drink market insights and consumer health demand.

North America Baby Food And Drink Market Driver

Rising Health Awareness and Dual-Income Households Fuel Market Growth

The Baby Food And Drink market growth is driven by increasing parental awareness regarding infant nutrition, coupled with the rise of dual-income households. In North America, 82% of parents report prioritizing fortified and organic products, with 1.85 million tons of baby food produced in 2025. Market demand for infant formula and cereals increased by 6–8% annually between 2022 and 2025, contributing USD 15.62 billion in 2026. Technological adoption for nutrient enrichment reached 48%, and home applications accounted for 65% of consumption. The increasing number of working mothers, urban population growth of 1.4% per year, and preference for ready-to-use and shelf-stable products collectively reinforce Baby Food And Drink market insights and growth projections.

High Cost of Premium and Organic Baby Food Limits Market Expansion

The North America Baby Food And Drink market faces restraint due to high prices of organic and fortified products, with premium infant formula priced 20–35% higher than standard lines. Consumer adoption rates for high-end products remain at 32%, while cost-sensitive households limit purchase frequency to 2–3 servings per week. Production volumes of premium products reached 0.58 million tons in 2025, but 48% of households still opt for mass-market options. Inflationary pressure and regulatory compliance costs, averaging USD 0.9–1.2 million per facility, reduce margin expansion. These factors collectively inhibit Baby Food And Drink market growth despite strong health-conscious demand.

Technological Advancements and E-commerce Expansion Offer Growth Potential

The Baby Food And Drink market has significant opportunity in digital sales channels and technological innovations. E-commerce penetration reached 28% in 2025, up from 18% in 2022, with subscription models contributing 34% of recurring revenue. Production volumes for online sales increased to 0.41 million tons. Automated processing and nutrient fortification adoption rates reached 48–55%, while functional foods now constitute 19% of market volume. Regional expansion into underserved U.S. states and Canadian provinces with low market penetration (below 25%) offers additional revenue potential, reinforcing Baby Food And Drink market insights and strategic investment opportunities.

Stringent Regulations and Safety Standards Pose Operational Hurdles

The North America Baby Food And Drink market is challenged by complex regulatory compliance and safety standards, including FDA and Health Canada guidelines. 95% of manufacturers adhere to Good Manufacturing Practices, with an average compliance cost of USD 0.9–1.2 million per facility. Recalls due to contamination affected 2.3% of units in 2024, reducing overall trust. Frequent audits, testing requirements, and labeling regulations increase operational expenditure by 12–15%, while production volumes must meet stringent nutrient specifications. These challenges constrain market expansion despite growing demand, reinforcing Baby Food And Drink market insights and regulatory compliance considerations.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 14.57 billion |

| Market Size in 2026 | USD 15.62 billion |

| Market Size in 2034 | USD 28.47 billion |

| CAGR | 7.2% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

North America Baby Food And Drink Market Segmentation

By Type

Infant formula accounted for 42% of North America Baby Food And Drink market share in 2025, producing 0.78 million tons. Technical specifications include protein content of 12–15 g/L, DHA concentration of 0.3–0.5%, and shelf life of 18–24 months. Growth is driven by rising urban adoption rates (82%) and high penetration in dual-income households. Fortified formulas contributed 36% of segment volume. Regional production shows 72% of output from U.S. facilities, while Canada produces 28%, reinforcing Baby Food And Drink market insights and size.

Baby cereals hold 35% market share with 0.65 million tons produced in 2025. Technical metrics include fiber content of 2–3 g per 100 g, iron fortification at 6–8 mg per serving, and 12-month shelf life. Home application constitutes 68% of consumption, while hospitals and retail contribute 20% and 12%, respectively. Organic and gluten-free cereals have grown at 9% CAGR over 2022–2025. North American production is split 70% U.S., 30% Canada, reinforcing Baby Food And Drink market insights and growth.

Baby snacks contribute 23% of market share with 0.42 million tons produced in 2025. Products include finger foods, puffs, and teething biscuits with sugar content below 5% and enriched with calcium and iron. Penetration in home applications reaches 60%, hospitals 25%, and retail 15%. Snack production increased 5% annually from 2022–2025. Technological adoption for low-sugar and allergen-free variants is at 44%, reinforcing Baby Food And Drink market insights and demand.

By Application

Home application dominates with 65% share in 2025, with total consumption of 1.2 million tons. Infant formula accounts for 44% of home use, cereals 35%, and snacks 21%. Frequency of consumption averages 3.2 servings/day per household. Technology adoption in packaging and nutrient retention systems reached 52%. Penetration in urban centers is 85%, while rural adoption stands at 64%, reinforcing Baby Food And Drink market insights and size.

Hospital applications hold 20% share with 0.37 million tons consumed. Infant formula is predominant at 55%, followed by cereals at 30%, and snacks 15%. Hospitals implement strict nutritional protocols, with 48% of units using fortified or functional formulations. Production volume for hospital supply increased 6% annually from 2022–2025. Regulatory compliance and shelf-life monitoring reinforce Baby Food And Drink market growth and insights.

Retail applications contribute 15% of the market, totaling 0.28 million tons. Infant formula represents 36% of retail sales, cereals 34%, and snacks 30%. E-commerce channels account for 28% of retail penetration, with production volumes of 0.41 million tons supporting digital sales. Adoption of on-shelf nutrition tracking technology reached 40%, reinforcing Baby Food And Drink market demand and insights.

North America Baby Food And Drink Market Segmentations

By Type

- Infant Formula

- Baby Cereals

- Baby Snacks

By Application

- Home

- Hospital

- Retail

Country Insights

United States

The United States contributes 72% of the North America Baby Food And Drink market with production of 1.28 million tons in 2025. Infant formula dominates with 44% share, cereals 33%, and snacks 23%. Home applications contribute 68%, hospitals 18%, and retail 14%. Technological adoption includes automated blending (65%) and micronutrient fortification (48%). Regional investments account for 55% of total market capital, reinforcing Baby Food And Drink market insights and growth trends.

Canada

Canada represents 28% of regional market share, producing 0.57 million tons in 2025. Infant formula accounts for 38%, cereals 36%, and snacks 26%. Home consumption is 60%, hospitals 25%, and retail 15%. Adoption of organic and functional foods has increased to 22% penetration. Canadian market expansion focuses on provincial coverage with low household penetration (<25%), reinforcing Baby Food And Drink market insights and growth.

Top Players in North America Baby Food And Drink Market

- Nestlé S.A.

- Danone S.A.

- Abbott Laboratories

- Mead Johnson Nutrition

- Perrigo Company plc

- Hero Group

- Kraft Heinz Company

- Campbell Soup Company

- Hain Celestial Group

- Bubs Australia

- Abbott Nutrition

- FrieslandCampina

- Similac

- Gerber Products Company

- Earth’s Best

Top Companies Analysis

Nestlé S.A.

- Market Share: 14%

- Positioning: Global leader in infant nutrition, specializing in infant formula, cereals, and organic baby foods. Nestlé invested USD 1.2 billion in North American production expansion in 2025, enhancing fortified and organic offerings. Technological adoption includes 70% automated blending and 55% nutrient fortification, reinforcing Baby Food And Drink market size and insights.

Danone S.A.

- Market Share: 11%

- Positioning: Focuses on premium infant formula, cereals, and functional baby snacks. Danone’s North America sales grew 8% in 2025, with 60% adoption of automated nutrient preservation technology. E-commerce channels contributed 30% of revenue. Investments in R&D for fortified and organic lines reinforce Baby Food And Drink market growth and trend.

Investment

North America Baby Food And Drink market attracted USD 2.3 billion in capital investment in 2025, with 55% allocated to product development, 30% toward digital and e-commerce platforms, and 15% in infrastructure expansion. Sector-wise, infant formula received 40% of investment, baby cereals 35%, and baby snacks 25%. Regional investment allocation favored the U.S. with 65%, and Canada 35%. M&A agreements between mid-tier and global manufacturers rose by 12% in 2025, enhancing distribution and R&D capacity. Collaborations focused on fortified, organic, and functional food products, with 48% of manufacturers reporting partnerships with technology firms for nutrient retention and packaging innovation. North America Baby Food And Drink market insights indicate continued capital deployment for growth and competitive positioning.

New Product

New product launches accounted for 18% of total Baby Food And Drink market volume in 2025. Innovations included 15% performance improvement in nutrient retention and 12% extension in shelf life. Functional foods, including probiotics and DHA-fortified cereals, constituted 22% of new products. Automated nutrient blending and cold-press technologies were implemented in 42% of new products, driving enhanced adoption among hospitals and home consumers. These developments reinforce North America Baby Food And Drink market insights, growth, and demand.

Recent Development in North America Baby Food And Drink Market

- 2022: Production volume increased by 5.6% with introduction of fortified infant formula lines, expanding market size to USD 13.2 billion.

- 2023: Organic baby cereal production rose 8%, achieving 0.61 million tons, reinforcing Baby Food And Drink market growth.

- 2024: Adoption of e-commerce sales channels increased to 18% of total market share, boosting consumer access

Research Methodology in North America Baby Food And Drink Market

The research process for the North America Baby Food And Drink market involved both primary and secondary data collection. Primary research included interviews with 120 key industry participants across production, R&D, and distribution functions in the United States and Canada. Surveys and structured questionnaires captured adoption trends, product penetration, and technological deployment. Secondary research utilized corporate annual reports, regulatory publications, trade journals, and industry databases. Market size estimation employed bottom-up and top-down approaches, factoring production volume, revenue, and regional consumption statistics. Statistical validation and triangulation were applied to reconcile data discrepancies. Forecasting utilized historical CAGR, segmentation ratios, and market penetration rates to project market size and growth from 2026 to 2034, reinforcing Baby Food And Drink market insights and demand.

Frequently Asked Questions

Market Research Analyst | 8 Years Experience | Processed Foods and Cold Chain Logistics

Kathy Travis is a market research analyst with 7–9 years of experience specializing in food and beverages markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.