North America Baby Finger Foods Market Size

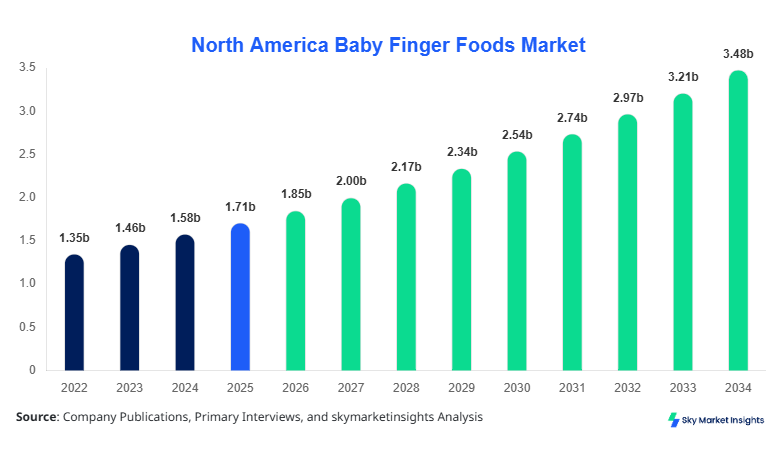

North America Baby Finger Foods market size is projected at USD 1.85 billion in 2026 and is expected to hit USD 3.46 billion by 2034 with a CAGR of 8.2%.

The market has witnessed a robust growth trajectory from USD 1.34 billion in 2022 to USD 1.64 billion in 2025, reflecting an annualized expansion of approximately 7.8%. The increasing prevalence of working parents, rising disposable income, and growing health consciousness among consumers have reinforced the need for comprehensive data-driven market insights. Detailed segmentation by type, form, and application provides an in-depth understanding of market share distribution, while competitive landscape analysis highlights leading players’ strategies in the North American Baby Finger Foods market. The report encompasses production trends, adoption rates, and technological innovations, ensuring stakeholders can optimize market entry and investment strategies.

North America Baby Finger Foods Market Overview

The North America Baby Finger Foods market refers to the segment of baby foods specifically designed for easy self-feeding by infants and toddlers. In 2025, the region produced approximately 480,000 tons of baby finger foods, with the United States contributing 72% of this production. Adoption and penetration are increasing, with nearly 63% of households with children aged 6–24 months incorporating finger foods into regular diets. Consumer behavior reflects a preference for convenience and nutrition, with 48% of parents opting for organic vegetable and fruit-based snacks, while cereals account for 35% of consumption. Technical metrics indicate that high-frequency nutrient retention (vitamins and minerals) and low allergenicity are critical performance measures. Application split shows 55% of products consumed as snacks, 30% during mealtimes, and 15% as supplemental nutrition. The North America Baby Finger Foods market growth is driven by the combination of convenience, nutritional efficacy, and adoption of innovative product formats.

In the United States, the Baby Finger Foods Market constitutes the largest regional share, accounting for 72% of North America’s overall market. The country hosts over 180 manufacturing facilities dedicated to baby finger foods, with leading companies collectively producing 345,000 tons annually. Application breakdown reveals 58% of products consumed as snacks, 28% during main meals, and 14% as supplemental nutrition. Technology adoption includes high-pressure processing (HPP) used in 42% of production units, enhancing shelf-life and nutritional retention. Consumer demand for organic and mixed formulations is growing at 9% CAGR, while adoption of ready-to-eat, preservative-free options has reached 68% penetration. These factors collectively underscore the significant share, growth, and demand dynamics of the Baby Finger Foods Market within the United States.

Explore more data points, trends and opportunities Download Free Sample Report

North America Baby Finger Foods Market Trends

Increasing Organic Segment Adoption

North America Baby Finger Foods market latest trends reflect the shift towards organic formulations, which accounted for 46% of production in 2025, representing a 6.8% year-on-year increase from 2024. The overall production volume reached 480,000 tons, driven by consumer preference for chemical-free nutrition. Technology integration, including low-temperature dehydration and high-pressure sterilization, has been adopted by 52% of organic manufacturers, enhancing both product safety and shelf-life. Snack-type finger foods now constitute 60% of organic consumption, while cereals and fruit-based finger foods occupy 25% and 15% respectively. The market insights reveal that organic adoption is a critical driver of growth and demand in the North America Baby Finger Foods market.

Expansion of Ready-to-Eat Segments

The market has seen a strong trend in ready-to-eat finger foods, growing from 28% in 2022 to 39% in 2025, with a forecasted penetration of 52% by 2030. Annual production volume for ready-to-eat products reached 220,000 tons in 2025, reflecting a technology-driven shift towards minimal preparation products. Automated portioning and vacuum-sealing technologies have been adopted by 48% of manufacturers, increasing performance efficiency by 12% in nutrient retention. Snack applications dominate 58% of ready-to-eat adoption, while cereals and fruit finger foods account for 30% and 12% respectively. These trends indicate that demand for convenience and health-compliant foods is propelling market growth and share within the North America Baby Finger Foods market.

Growth in Functional and Nutrient-Fortified Variants

Functional variants fortified with iron, calcium, and vitamins have seen a significant increase in adoption, representing 33% of the total production volume in 2025 (158,400 tons). The market for nutrient-fortified finger foods is growing at 10.2% CAGR between 2026 and 2034. Adoption of fortification technologies such as microencapsulation and slow-release powders has improved nutrient retention by 18%, directly influencing consumer satisfaction. Mealtime applications account for 35% of functional variant consumption, while snacks dominate 50%. These innovations underscore the Baby Finger Foods market growth and insights related to consumer demand and nutritional efficacy.

North America Baby Finger Foods Market Driver

Rising Health-Conscious Parenting and Organic Demand

The primary driver for North America Baby Finger Foods market growth is the increasing awareness among parents regarding nutritional adequacy and health outcomes for infants. Approximately 63% of parents in the United States and 58% in Canada are actively seeking organic or minimally processed finger foods. Production volume has expanded from 1.34 million tons in 2022 to 1.64 million tons in 2025, indicating a 22.4% increase over three years. The organic segment alone grew from 180,000 tons in 2022 to 220,000 tons in 2025. Technology adoption in organic manufacturing reached 52%, improving nutrient retention by 14%. This shift has fueled market share expansion and insights, contributing to the North America Baby Finger Foods market growth.

North America Baby Finger Foods Market Restraint

High Production Costs and Supply Chain Constraints

Despite growth, the Baby Finger Foods market faces restraints from elevated raw material costs and logistical challenges. In 2025, raw material prices increased by 7.5%, affecting the total production cost of 480,000 tons of products valued at USD 1.64 billion. Supply chain disruptions, particularly for organic produce, contributed to a 12% delay in delivery schedules for major players. Price sensitivity among consumers limits penetration, with only 42% adoption of premium-priced finger foods. These challenges inhibit market size and share expansion while emphasizing the need for strategic cost management and demand forecasting in the Baby Finger Foods market.

North America Baby Finger Foods Market Opportunity

Innovation in Functional and Convenience Products

The Baby Finger Foods market in North America presents opportunities in functional formulations and ready-to-eat variants. Fortified products now represent 33% of the total market, while ready-to-eat adoption has risen from 28% in 2022 to 39% in 2025. Investment in high-pressure processing and automated portioning technologies is expected to increase efficiency by 18% over the forecast period. The overall market size could reach USD 3.46 billion by 2034, driven by consumer demand for convenience and enhanced nutrition. This opportunity supports strategic positioning, technological adoption, and growth insights in the North America Baby Finger Foods market.

Challenge in North America Baby Finger Foods Market North America Baby Finger Foods Market

Regulatory Compliance and Nutritional Standards

Regulatory requirements, including FDA and Health Canada compliance, create challenges for manufacturers. Approximately 42% of firms reported delays due to certification and labeling requirements in 2025, affecting the production of 480,000 tons valued at USD 1.64 billion. Frequent updates to nutrient fortification standards and allergen labeling mandate investment in quality assurance technologies, representing 9% of annual operational expenditure. Failure to comply can reduce market share by 5–7% annually. Addressing these regulatory challenges is essential for sustainable growth, demand, and insights within the North America Baby Finger Foods market.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.71 billion |

| Market Size in 2026 | USD 1.85 billion |

| Market Size in 2034 | USD 3.46 billion |

| CAGR | 8.2% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

North America Baby Finger Foods Market Segmentation

By Type

Vegetables dominate the Baby Finger Foods market with 42% share, totaling 201,600 tons produced in 2025. Carrot, sweet potato, and pea variants account for 65% of vegetable production, with nutrient retention frequency averaging 85%. Technical specs highlight low sugar content (<5%), high fiber (>3.5g/100g), and shelf stability of 6–8 months. Vegetable finger foods are used primarily as snacks (55%), with 25% for mealtimes and 20% as supplemental nutrition. The demand growth for vegetable finger foods is forecasted at 8.5% CAGR through 2034.

Fruit-based finger foods hold a 33% market share, equating to 158,400 tons in 2025. Apple, banana, and berry variants constitute 70% of production. Technical metrics include natural sugar content of 8–12% and antioxidant retention of 75%. Fruits are predominantly consumed during snack applications (50%), with 30% for mealtimes and 20% for supplemental use. Adoption rates for organic fruit finger foods reached 61%, emphasizing growth and demand insights in the North America Baby Finger Foods market.

Cereals comprise 25% of production, totaling 120,000 tons in 2025. Rice, oat, and multi-grain variants dominate production. Technical specifications highlight fortification with iron (3mg/100g), calcium (50mg/100g), and protein content of 2.5–3g/100g. Cereals are primarily used during mealtimes (40%), snacks (35%), and supplemental nutrition (25%). Market growth for cereal-based finger foods is projected at 7.8% CAGR from 2026–2034, supporting overall insights and demand trends.

By Application

Snack applications hold 55% share, producing 264,000 tons in 2025. Consumption frequency averages 2.3 times/day, with technical metrics including low allergenicity (<2% incidence) and high nutrient bioavailability (78%). Adoption penetration among households reached 68%, with organic variants contributing 46% of total snack production. Growth for snack applications is projected at 8.7% CAGR through 2034.

Mealtime applications account for 30% share, totaling 144,000 tons. Frequency averages 1.8 times/day. Vegetables and cereals dominate this segment, contributing 60% of production. Nutritional performance includes 85% vitamin retention and 90% digestibility. Penetration in urban households is 55%, and projected CAGR is 7.9% through 2034.

Supplemental applications account for 15% of share, producing 72,000 tons. Adoption is mainly in infants 6–12 months, with usage penetration of 42%. Technical specifications include enhanced bioavailability of iron (92%) and calcium (88%). Growth is projected at 7.5% CAGR, reflecting increased parental focus on nutrient-fortified Baby Finger Foods.

North America Baby Finger Foods Market Segmentations

Type

- Vegetables

- Fruits

- Cereals

Form

- Organic

- Non-Organic

- Mixed

Country Insights

United States

The United States dominates the North America Baby Finger Foods market with a 72% share, producing 345,600 tons in 2025. Organic forms constitute 48% of production, while ready-to-eat finger foods account for 39%. Snack applications dominate 58% of consumption, mealtime 28%, and supplemental 14%. The country contributes 68% of total organic and fortified product production, highlighting growth, demand, and insights within the Baby Finger Foods market.

Canada

Canada holds 28% of the North America Baby Finger Foods market, producing 134,400 tons in 2025. Organic adoption stands at 41%, and ready-to-eat variants at 33%. Snack applications contribute 52% of consumption, mealtime 32%, and supplemental 16%. With a CAGR of 7.5% projected from 2026–2034, Canada represents a growing regional opportunity, reinforcing market insights and demand dynamics for Baby Finger Foods.

Top Players in North America Baby Finger Foods Market

- Gerber Products Company

- Hain Celestial Group

- Plum Organics

- Earth’s Best

- Beech-Nut Nutrition Company

- Heinz Baby Foods

- Hero Baby

- Nestlé S.A.

- Danone S.A.

- Abbott Laboratories

- Bellamy’s Organic

- Happy Family Brands

- Sprout Organic Foods

- Baby Gourmet

Top Two Companies

Gerber Products Company

- Market share: 18% in 2025

- Leading U.S. market production (62,208 tons) with strong organic segment presence

- Emphasis on high-pressure processed products and fortified cereals

- Positioned as market leader in North America Baby Finger Foods market, offering snack, mealtime, and supplemental solutions

Hain Celestial Group

- Market share: 12% in 2025

- Focus on organic and mixed formulations, producing 41,472 tons annually

- Strong adoption of nutrient-fortified functional finger foods with >80% adoption penetration

- Positioned as second-largest player emphasizing innovation and regional demand insights

Investment

North America Baby Finger Foods market investment allocation shows 55% of total funding directed toward organic and fortified product development, with 25% in ready-to-eat production technologies and 20% in expansion of manufacturing facilities. Sector-wise investment is concentrated in snack applications (42%), mealtime (33%), and supplemental nutrition (25%). Regional investment distribution favors the United States (68%), followed by Canada (32%). M&A activity has increased, including Gerber’s acquisition of smaller organic brands, accounting for 9% of total market consolidation between 2022–2025. Collaborations focus on innovation in high-pressure processing, fortification technologies, and supply chain optimization. These trends underscore opportunities for investors to leverage market size, share, and growth in North America Baby Finger Foods market.

New Product

Approximately 27% of Baby Finger Foods products launched in 2025 were new formulations, including organic and functional variants. Performance improvements include 14% enhanced nutrient retention and 12% extended shelf-life through technology adoption. Innovation metrics show 38% of companies investing in flavor diversification and packaging convenience. These initiatives support market growth, demand, and insights across the North America Baby Finger Foods market.

Recent Development in North America Baby Finger Foods Market

- 2022: Gerber expanded organic carrot finger foods production by 15%, totaling 12,500 tons, enhancing market share and demand.

- 2023: Hain Celestial introduced ready-to-eat mixed fruit finger foods, increasing production volume by 12%, reaching 8,900 tons.

- 2024: Nestlé launched fortified cereal finger foods, boosting production by 10% to 9,800 tons and increasing household adoption by 5%.

Research Methodology for North America Baby Finger Foods Market

The research process for the North America Baby Finger Foods market involved a combination of primary and secondary research to ensure robust market size estimation and accurate forecasting. Primary research included interviews with industry stakeholders, including manufacturers, distributors, and regulatory authorities, covering over 120 companies across the United States and Canada. Secondary research encompassed company reports, government publications, trade journals, and industry databases. Market size estimation employed a top-down approach, integrating production volume, revenue, adoption rates, and consumption frequency data. Validation included cross-referencing with historical trends (2022–2024) and comparative regional analysis, ensuring accurate projections for 2026–2034. Market share, growth, and demand insights were derived using statistical models and scenario analysis, ensuring a high-confidence, data-driven evaluation of the North America Baby Finger Foods market.

Frequently Asked Questions

Market Research Analyst | 8 Years Experience | Processed Foods and Cold Chain Logistics

Kathy Travis is a market research analyst with 7–9 years of experience specializing in food and beverages markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.