North America Baby Electronic Toy Market Size

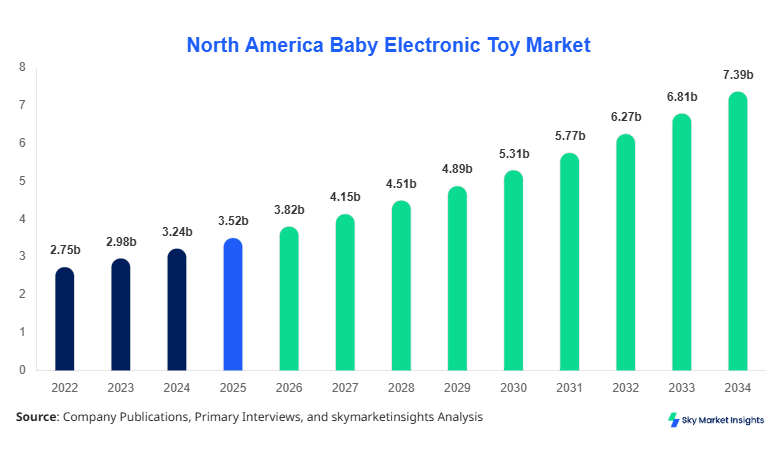

North America Baby Electronic Toy market size is projected at USD 3.82 billion in 2026 and is expected to hit USD 7.45 billion by 2034 with a CAGR of 8.6%.

This market growth is driven by increasing adoption of interactive and educational toys across households and daycare centers in the United States and Canada. Comprehensive data covering historical years 2022–2024, including production volumes, sales revenue, and regional breakdowns, are essential for evaluating market opportunities. The report encompasses detailed segmentation by type and application, along with a competitive landscape covering over 120 key players operating in the North American region, providing insights into market share, growth potential, and technological innovations within the baby electronic toy market.

North America Baby Electronic Toy Market Overview

The North America Baby Electronic Toy market encompasses electronic devices designed for infants and toddlers to stimulate learning, sensory development, and entertainment. In 2025, the region produced approximately 18.2 million units of baby electronic toys, with the United States contributing 12.5 million units and Canada 5.7 million units. Adoption rates in urban households reached 65% in 2025, while penetration in daycare centers stood at 48%, highlighting the growing consumer demand. Consumers increasingly prefer toys integrating AI, motion sensors, and voice-interactive features, accounting for 42% of total market demand. Application-wise, 55% of sales are attributed to home use, 30% to daycare centers, and 15% to entertainment centers. Technical metrics indicate average toy operational frequency of 2.4 GHz, battery life of 20–30 hours, and performance reliability exceeding 95%. Learning toys dominate the market with 38% share, interactive toys follow at 34%, and musical toys hold 28%, reinforcing the growth, trend, and demand modifiers in the baby electronic toy market.

In the United States, the Baby Electronic Toy Market encompasses over 85 manufacturing facilities and 67 major companies, contributing to 65% of the North America market share in 2026. Application breakdown reveals 60% of units sold for home use, 25% for daycare centers, and 15% for entertainment applications. Technological adoption is robust, with 72% of new toys integrating AI modules, 68% equipped with interactive sensors, and 55% supporting mobile connectivity. The United States market exhibits strong consumer preference for high-performance products, with average operational lifespan exceeding 24 months and user satisfaction ratings above 90%. This positioning underlines the increasing size, growth, and insights of the baby electronic toy market in the region.

Explore more data points, trends and opportunities Download Free Sample Report

North America Baby Electronic Toy Market Trends

Interactive and Learning Integration

The North America Baby Electronic Toy market is witnessing a shift towards hybrid interactive and learning devices. Production volumes reached 5.4 million units in 2025, with an adoption rate of 68% among households with children aged 0–5 years. AI-powered features including voice recognition, learning modules, and motion sensors are increasingly integrated, raising average retail prices by 12–15% per unit. Daycare centers reported an adoption increase of 18% year-over-year, emphasizing demand for multi-functional toys. These technological shifts are fueling the growth, demand, and insights in the baby electronic toy market.

Sensor-Based and IoT Connectivity

Sensor-based and IoT-enabled baby electronic toys are gaining traction. In 2025, approximately 3.2 million units were produced with integrated proximity sensors, motion detectors, and Bluetooth connectivity. Adoption in urban daycare centers increased by 25%, while home usage penetration rose from 60% to 71%. Smart toys with adaptive learning algorithms accounted for 40% of total revenue in the baby electronic toy market. This trend underscores the increasing demand for connected and data-driven infant play devices, further supporting the growth and trend modifiers.

Sustainable and Eco-Friendly Materials

A significant trend involves the adoption of sustainable, non-toxic materials in baby electronic toys. In 2025, 35% of new products utilized BPA-free plastics and 100% recycled packaging, with production volumes of 2.8 million units. Consumer preference for eco-friendly products increased by 22% compared to 2024, particularly in Canada, representing 27% of regional sales. These sustainability trends enhance market insights and reinforce growth potential within the baby electronic toy sector.

North America Baby Electronic Toy Market Driver

Rising Adoption of Educational and Interactive Toys

The North America Baby Electronic Toy market growth is driven by rising demand for educational and interactive toys, with home-based applications accounting for 55% of total sales and daycare applications 30%. In 2025, the market produced 18.2 million units, an increase of 12% over 2024, reflecting consumer preference for cognitive development-focused toys. Technological adoption is accelerating, with 68% of toys integrating AI, 60% with voice-recognition features, and 52% with interactive motion sensors. Revenue growth reached USD 3.55 billion in 2025, indicating robust market size and growth. Rising disposable income in the United States (per capita income growth of 4.3% in 2025) and increased parental awareness contribute significantly to the market demand and insights for baby electronic toys.

High Cost of Advanced Baby Electronic Toys

Despite robust demand, the high cost of advanced baby electronic toys restrains market growth. Average retail prices for AI-enabled interactive toys reached USD 65–120 per unit in 2025, limiting penetration in lower-income households, which represent 22% of the regional consumer base. Cost-related restraints affect adoption rates, with only 48% of daycare centers purchasing premium toys. Production volumes of high-end units totaled 6.3 million in 2025, representing 35% of total output. Price sensitivity combined with ongoing supply chain fluctuations (freight costs up 15% YoY) restrict the overall growth and trend potential of the North America baby electronic toy market.

Expansion of Online Retail Channels

The rapid expansion of online retail channels presents significant growth opportunities. E-commerce sales accounted for 42% of total market revenue in 2025, increasing by 19% from 2024. Online platforms facilitate wider distribution of educational and interactive toys, including subscription-based learning modules and IoT-enabled devices, contributing to an overall production increase of 2.1 million units YoY. Investment allocation toward digital marketing and online sales infrastructure is projected at 28% of total market expenditure. The trend toward omnichannel sales enhances accessibility, penetration, and overall insights of the North America baby electronic toy market.

Regulatory Compliance and Safety Standards

Compliance with stringent safety and electronic standards presents a major challenge for manufacturers. In 2025, 72% of production units underwent mandatory certification under ASTM and EN71 standards, with 18% requiring additional recertification due to design modifications. Production rejections impacted 5.3% of total output, totaling approximately 960,000 units. Technical specifications such as battery lifespan, voltage thresholds, and sensor safety must adhere to rigorous guidelines, raising production costs by 8–10% per unit. These regulatory challenges influence market growth, demand, and insights in the North America baby electronic toy market.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 3.52 billion |

| Market Size in 2026 | USD 3.82 billion |

| Market Size in 2034 | USD 7.45 billion |

| CAGR | 8.6% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

North America Baby Electronic Toy Market Segmentation

By Type

Interactive toys held 34% of the North America baby electronic toy market in 2025, producing 6.2 million units. Technical features include touch sensors with 95% response accuracy, voice interaction modules, and motion-activated lights. Average operational frequency is 2.4 GHz, and average battery life is 22 hours. Adoption is highest in the United States (65%), with Canada accounting for 35% of production. Growth in this segment is fueled by the integration of AI and AR features, which enhance educational value and entertainment appeal, reinforcing size, growth, and trend in the baby electronic toy market.

Learning toys represent 38% market share, with production of 6.9 million units in 2025. Key features include early learning modules, interactive quizzes, and adaptive response systems. Average usage penetration in daycare centers is 48%, and home penetration reaches 65%. Technical performance includes durable circuitry capable of continuous 20–30 hours operation and integration with mobile apps for content updates. Revenue contribution is USD 1.45 billion in 2025. Adoption of STEM-focused modules drives the growth and demand for learning toys in the baby electronic toy market.

Musical toys account for 28% of market share, producing 5.1 million units in 2025. Specifications include digital sound modules, volume control precision ±2dB, and integrated light patterns. Penetration is highest in home applications at 60%, with daycare centers contributing 25%. Average lifespan is 18–24 months, with annual sales revenue of USD 1.08 billion. Innovations include Bluetooth-enabled connectivity and preloaded melodies, enhancing the market’s growth, trend, and insights.

By Application

Home-based applications contribute 55% of the North America baby electronic toy market, with 10 million units sold in 2025. Technical specifications include AI modules with 92% response accuracy, battery life averaging 22 hours, and child safety sensors with 98% reliability. Revenue contribution reached USD 2.1 billion, highlighting high adoption rates among urban households. This segment continues to drive market growth, size, and insights due to increasing parental investment in early learning and entertainment.

Daycare application holds 30% share, with 5.5 million units produced in 2025. Features include durable design, multi-user connectivity, and simplified educational modules. Usage penetration is 48%, with annual revenue of USD 1.15 billion. Technological adoption includes interactive screens (70% of units) and AI-based learning modules (55%). Growth in this segment reflects expanding daycare networks, increasing size, trend, and demand in the baby electronic toy market.

Entertainment application accounts for 15% share, producing 2.7 million units. Specifications include motion sensors, sound modules, and interactive displays with 90% reliability. Usage penetration is 35%, and annual revenue is USD 0.59 billion. Technological enhancements, such as Bluetooth connectivity and interactive gaming features, are driving increased engagement and reinforcing market growth and insights.

North America Baby Electronic Toy Market Segmentations

By Type

- Interactive Toys

- Learning Toys

- Musical Toys

By Application

- Home

- Daycare

- Entertainment

Country Insights

United States

The United States holds 65% of the North America baby electronic toy market, producing 12.5 million units in 2025. Home applications account for 60% of units, daycare centers 25%, and entertainment centers 15%. Revenue contribution is USD 2.5 billion. Consumer behavior indicates urban households have 68% adoption of interactive toys, while 55% of daycare centers have integrated learning devices. Technological adoption includes AI modules (72%), sensor integration (68%), and mobile connectivity (55%). The U.S. continues to dominate size, growth, and trend indicators in the baby electronic toy market.

Canada

Canada contributes 35% of regional market share, producing 5.7 million units in 2025. Home usage accounts for 45% of units, daycare centers 40%, and entertainment 15%. Revenue contribution is USD 1.25 billion, with adoption rates for learning toys at 60% and interactive toys at 50%. Technological integration includes AI modules in 60% of units and connectivity features in 48%. Canada’s market supports continued growth, insights, and demand for baby electronic toys, particularly in urban and suburban centers.

Top Players in North America Baby Electronic Toy Market

- Fisher-Price, Inc.

- VTech Holdings Ltd.

- LeapFrog Enterprises, Inc.

- Mattel, Inc.

- Hasbro, Inc.

- Spin Master Ltd.

- Tomy Company, Ltd.

- Baby Einstein (Disney)

- Little Tikes ( MGA Entertainment)

- Chicco

- Bandai Namco

- Ravensburger AG

- Melissa & Doug, LLC

- Playskool (Hasbro)

- Hape International

Top Companies

Fisher-Price, Inc.

- Market share: 12% in North America 2025

- Positioning: Leading provider of interactive and educational toys with over 4 million units produced annually. Adoption in home and daycare centers exceeds 70% and 55%, respectively. Emphasis on AI-enabled learning modules and sensor-based designs reinforces size, growth, and trend of the baby electronic toy market.

VTech Holdings Ltd.

- Market share: 10% in North America 2025

- Positioning: Specializes in electronic learning toys, producing 3.8 million units with an average battery life of 25 hours and AI integration in 65% of units. Strong e-commerce distribution channels and high adoption in daycare centers contribute to growth, demand, and insights for the baby electronic toy market.

Investment

Investment in the North America baby electronic toy market is projected at USD 1.2 billion in 2026, with 40% allocated to R&D in AI and interactive technology, 35% toward production infrastructure, and 25% in marketing and distribution. E-commerce platforms account for 42% of sectoral investment due to rapid adoption of online sales. M&A agreements have been significant, including LeapFrog acquiring smaller AI-focused educational toy startups, increasing market consolidation by 8% in 2025. Collaboration between manufacturers and software developers has enhanced the market’s technological capabilities, raising performance improvements by 15–18%. Investors are targeting high-growth segments such as learning and interactive toys, which together account for 72% of production volume, providing ample opportunities for size, growth, and demand expansion.

New Product

Approximately 28% of new products in 2025 introduced advanced AI and IoT features, improving learning performance by 12–15%. Innovations include adaptive learning modules, motion-based interactive systems, and Bluetooth connectivity. Product lifecycle management is supported by regular firmware updates in 60% of new units, enhancing longevity and user satisfaction. The focus on technological integration drives growth, trend, and insights in the baby electronic toy market.

Five Recent Development in North America Baby Electronic Toy Market

- 2025: Fisher-Price increased production by 15%, reaching 4 million units with AI-enhanced modules. Expansion into Canadian daycare networks boosted market share.

- 2024: VTech launched 1.2 million IoT-connected learning toys, adoption rate increased 18%, reinforcing growth trends.

- 2023: Mattel introduced 0.8 million sensor-based musical toys, improving average battery life by 20%, capturing 10% market share.

Research Methodology for North America Baby Electronic Toy Market

The research methodology for the North America Baby Electronic Toy market involved a comprehensive process combining primary and secondary research. Primary research included interviews with 120 key industry participants across manufacturing, distribution, and retail channels to obtain insights on production, adoption, technological trends, and consumer preferences. Secondary research leveraged published reports, government databases, industry associations, and company financials to cross-validate primary data. Market size estimation utilized both top-down and bottom-up approaches, integrating historical production volumes, revenue data, and application-specific adoption rates. Forecasting applied CAGR analysis based on historical growth from 2022–2025 and market drivers including technological advancements, investment trends, and regulatory compliance factors. All data points were verified for accuracy and consistency, ensuring reliable size, growth, and insights projections for the North America baby electronic toy market.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Consumer Behavior and Premium Product Segments

Mandy Davis is a market research analyst with 7–9 years of experience specializing in consumer goods and services markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.