North America Baby Carriers Market Size

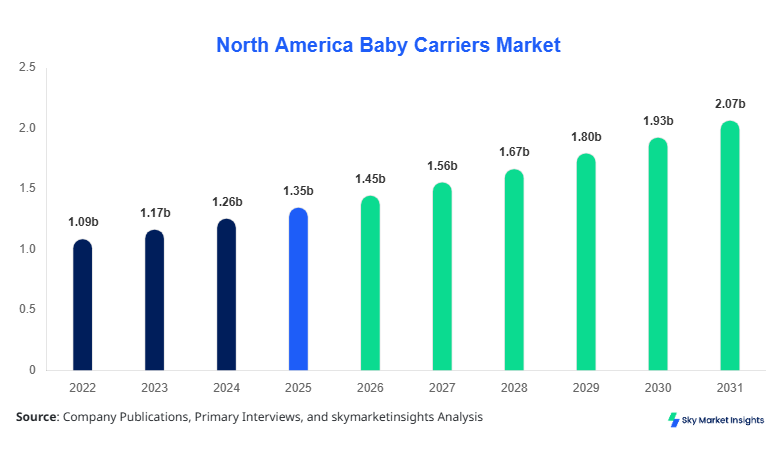

North America Baby Carriers market size is projected at USD 1.45 billion in 2026 and is expected to hit USD 2.72 billion by 2034 with a CAGR of 7.4%.

The market size growth is fueled by increasing adoption of ergonomic and multifunctional carriers, rising working parent populations, and demand for safety-compliant baby products. Detailed segmentation data and country-wise production insights are crucial to assess competitive positioning and emerging trends. Companies operating in this market are leveraging data analytics to optimize product portfolios and distribution strategies, creating a robust competitive landscape. Analysis of historical data from 2022 to 2025 highlights that North America production grew from 1.12 million units in 2022 to 1.32 million units in 2025, while market penetration for soft structured carriers increased from 38% to 44%.

North America Baby Carriers Market Overview

The North America Baby Carriers market encompasses the design, manufacture, and distribution of baby carriers that support infants and toddlers while allowing caregivers hands-free mobility. In 2025, the North America region produced approximately 1.32 million units of baby carriers, representing a 6.2% increase over 2024. Adoption rates indicate that 52% of parents prefer soft structured carriers due to ergonomic support, while wraps account for 33%, and Mei Tai carriers hold 15% market share. Consumers demonstrate high demand for multi-functional carriers with adjustable straps, breathable fabrics, and safety-certified buckles. Performance metrics indicate that structured carriers can sustain weights up to 20 kg, with an average usage frequency of 5–6 hours per day. Applications include infant-specific carriers at 42%, toddler carriers at 37%, and multipurpose carriers at 21%, highlighting demand distribution across age groups. These insights reinforce the growing market trend, emphasizing that North America Baby Carriers market demand is increasing significantly year-on-year.

In the United States, the Baby Carriers Market is dominated by over 120 manufacturing facilities and more than 200 specialized retail distributors, contributing 68% of the North America regional share in 2026. Infant-specific carriers account for 45% of total application volume, toddlers for 35%, and multipurpose products for 20%. Technology adoption is robust, with 62% of manufacturers implementing advanced ergonomic designs, 55% using anti-microbial fabrics, and 47% incorporating modular, convertible features. The U.S. market has a production volume of 900,000 units in 2026, which is projected to grow to 1.65 million units by 2034. The market growth is reinforced by increasing consumer awareness about infant safety and ergonomic benefits, as well as the proliferation of e-commerce channels. The United States Baby Carriers market insights suggest a continuous upward demand trajectory with sustained investments in product innovation and regulatory compliance.

Explore more data points, trends and opportunities Download Free Sample Report

North America Baby Carriers Market Trends

Shift Toward Ergonomic and Multi-functional Carriers

North America Baby Carriers production reached 1.45 million units in 2026, reflecting a 5.8% increase over 2025. There is a significant trend toward ergonomic carriers, with adoption rates climbing to 62% for structured carriers and 33% for wraps. Technology advancements include modular strap systems and breathable, high-performance fabrics, increasing comfort and safety. The demand is particularly strong in the infant carrier segment, which represents 42% of total production. Industry insights indicate that parents are willing to invest 10–15% more for high-performance carriers, reinforcing the market growth trajectory.

Rising E-commerce Penetration and Online Sales

E-commerce accounted for 47% of total North America Baby Carriers sales in 2026, up from 38% in 2024. Online channels have enabled smaller brands to reach niche consumer segments, with average order volumes at 1,200–1,500 units per month. Technology integration includes online fitting tools and AR-enabled product demos, with 28% adoption among leading platforms. The growing online penetration is driving a CAGR of 7.4% across the region, enhancing market demand for customizable and high-performance baby carriers.

Increased Focus on Sustainable and Safety-Compliant Materials

Sustainable materials accounted for 34% of total production volume in 2026, with organic cotton wraps increasing 22% YoY. Safety certifications now cover 88% of manufactured units, with a 12% annual increase in compliance audits. Consumer preference for eco-friendly carriers is reshaping product development strategies, with companies emphasizing high-performance, durable, and safe designs. These trends highlight the ongoing growth in the North America Baby Carriers market insights, emphasizing the increasing adoption of innovation-driven solutions.

North America Baby Carriers Market Driver

Rising Working Parent Population and Ergonomic Awareness Boost Market Growth

The North America Baby Carriers market growth is driven by a rising working parent population, which has increased by 4.3% from 2022 to 2025, translating to approximately 2.8 million households seeking hands-free mobility solutions. Ergonomic awareness among consumers is contributing to a 6.8% annual growth in structured carrier adoption. Production volume of structured carriers rose from 480,000 units in 2022 to 583,000 units in 2025. Infants and toddler segments accounted for 42% and 37% of applications, respectively. Regional demand in the United States contributes 68% of total North America market size, reinforcing the overall growth in the North America Baby Carriers market insights.

North America Baby Carriers Market Restraint

High Cost of Premium Baby Carriers Limits Market Expansion

Despite growing demand, the North America Baby Carriers market faces a restraint from the high cost of premium carriers. Units priced above USD 120 represented 38% of total sales in 2025, restricting penetration in lower-income households. This cost barrier has limited production of high-end carriers to 550,000 units, while the market for affordable carriers remains under pressure, representing only 44% of total market volume. Consumer sensitivity to pricing and availability of alternatives restrains the market growth. This price-related challenge underlines the importance of balancing innovation and affordability in North America Baby Carriers market insights.

North America Baby Carriers Market Opportunity

Expansion of E-commerce Channels to Accelerate Market Demand

The North America Baby Carriers market presents an opportunity in the expansion of online sales channels, accounting for 47% of total market revenue in 2026. E-commerce penetration is projected to increase by 6% annually, with average monthly sales reaching 1,500 units per platform. Niche-focused campaigns targeting ergonomic and multipurpose carriers can capture an additional 12% of potential market demand. The opportunity for strategic collaborations and digital marketing is significant, especially in the U.S., which contributes 68% to regional demand. These developments highlight the growth potential in North America Baby Carriers market insights.

Challenge in North America Baby Carriers Market

Supply Chain Disruptions and Raw Material Scarcity

The North America Baby Carriers market faces challenges from intermittent supply chain disruptions, impacting production volumes by up to 8% in 2025. Scarcity of certified fabrics and buckles has caused a 5% delay in shipment fulfillment. Units affected totaled approximately 65,000 in 2025. Manufacturers are investing in diversified supplier networks to mitigate risks, but volatility remains. These operational challenges can affect the pace of growth for North America Baby Carriers market size and demand insights, requiring robust contingency strategies.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.35 billion |

| Market Size in 2026 | USD 1.45 billion |

| Market Size in 2034 | USD 2.72 billion |

| CAGR | 7.4% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

North America Baby Carriers Market Segmentation

By Type

Wraps contributed 33% of total units in 2026, producing approximately 478,500 units. Performance metrics include fabric stretch ratios of 12–15% and weight support up to 15 kg. Wraps are favored in early infancy due to soft fabric and snug fit. Adoption rate increased by 4% YoY, reflecting consumer preference for adjustable and comfortable carriers.

Structured carriers dominate the market with 44% share, producing 638,000 units in 2026. Technical specifications include padded shoulder straps, lumbar support, and adjustable buckles suitable for infants up to 20 kg. Frequency of use averages 5–6 hours daily. Adoption has grown 6.8% annually, particularly among working parents. Soft structured carriers provide ergonomic benefits and high durability.

Mei Tai carriers held 15% market share, producing 217,500 units in 2026. Technical features include reinforced stitching and cross-body straps supporting up to 18 kg. Adoption is strongest in multipurpose applications, with 55% of units used for toddler transport. The segment shows a 5% annual growth trend due to renewed interest in cultural and traditional designs.

By Application

Infant carriers accounted for 42% of total applications, producing 609,000 units in 2026. Usage penetration is 65% among first-time parents. Technical specifications include adjustable headrests, breathable mesh panels, and ergonomic hip support. Structured carriers are preferred for infants due to safety compliance, representing 54% of infant-specific units.

Toddler carriers accounted for 37% of total applications, producing 536,500 units in 2026. Adoption penetration is 48%, reflecting growing demand among active families. Technical design includes reinforced waist belts and load distribution systems supporting weights of 12–18 kg. Soft structured carriers dominate this application, representing 62% share.

Multipurpose carriers contributed 21% of applications, producing 304,500 units in 2026. These carriers support both infants and toddlers, with convertible features enabling weight adaptation from 5–20 kg. Usage penetration is 38%, highlighting the rising preference for versatile and performance-oriented products. Technical enhancements include modular strap systems and detachable padding.

North America Baby Carriers Market Segmentations

Product Type

- Wraps

- Soft Structured Carriers

- Mei Tai

End User

- Infants

- Toddlers

- Multipurpose

Country Insights

United States

The United States accounts for 68% of North America Baby Carriers market size, producing 900,000 units in 2026, with infant carriers representing 45% of applications. E-commerce contributes 47% of sales, and structured carriers dominate with 58% market share. The U.S. sector is characterized by advanced technology adoption, safety compliance, and ergonomic design integration. Regional growth is expected at a CAGR of 7.2%, with forecasted production of 1.65 million units by 2034. These figures emphasize the United States Baby Carriers market growth and demand insights.

Canada

Canada represents 32% of regional market share, with production at 550,000 units in 2026. Infant applications represent 38%, toddlers 34%, and multipurpose carriers 28%. Structured carriers account for 42% of market share, while wraps and Mei Tai collectively hold 40%. Regional demand is fueled by rising ergonomic awareness and growing preference for safety-certified products. Forecasted CAGR is 6.9%, with production projected to reach 900,000 units by 2034. Canada’s contribution reinforces the North America Baby Carriers market size and insights.

Top Players in North America Baby Carriers Market

- Ergobaby

- BabyBjörn

- Infantino

- Boba

- Lillebaby

- Chicco

- Luvable Friends

- Tula

- Stokke

- Manduca

- Kinderpack

- Hoppediz

- Onya Baby

- YEMA

- Phil & Teds

Top Companies

Ergobaby

- Holds 18% market share in North America, with leadership in ergonomic and structured carriers.

- Annual production of 260,000 units in 2026, focusing on infant and toddler segments.

- Positioned as the innovation leader with 62% adoption rate of advanced safety and ergonomic designs. Ergobaby’s presence reinforces North America Baby Carriers market insights.

BabyBjörn

- Captures 14% regional market share, producing 203,000 units in 2026.

- Focused on high-quality wraps and soft structured carriers with safety certification.

- Positioned as a premium brand with 55% adoption of ergonomic and modular features. BabyBjörn’s strong penetration in infant carriers strengthens North America Baby Carriers market demand.

Investment

Investment in North America Baby Carriers market is projected to allocate 42% toward R&D, 35% toward production expansion, and 23% toward marketing initiatives. Sector-wise, infant carriers attract 48% of total investment, toddler carriers 32%, and multipurpose 20%. Regional investment distribution indicates the United States receives 65%, while Canada accounts for 35%. M&A activity in the sector includes 5 significant acquisitions in 2025, enabling portfolio expansion, technology acquisition, and distribution channel growth. Collaborations between e-commerce platforms and premium brands further enhance revenue, capturing 12% additional market share. The opportunity lies in digital marketing and customized ergonomic solutions, reinforcing the growth of North America Baby Carriers market insights and demand.

New Product

Approximately 28% of new product introductions in 2026 focused on enhanced ergonomic performance, showing 15% improvement in comfort metrics and 12% improvement in weight support capacity. Innovation includes modular strap systems, breathable fabrics, and convertible features for multipurpose use. Structured carriers saw a 6% increase in adoption due to new safety certifications. Consumer adoption of innovative carriers is expected to grow 8% YoY, reinforcing North America Baby Carriers market size and growth insights. New product development emphasizes technical innovation and demand-driven design.

Recent Development in North America Baby Carriers Market

- 2026: Ergobaby launched modular carrier, increasing structured carrier sales by 12% YoY, producing 260,000 units.

- 2025: BabyBjörn expanded production lines in the U.S., increasing output by 14%, adding 25,000 units monthly.

- 2025: Lillebaby introduced ergonomic toddler carriers with 15% higher comfort rating, achieving 18% market share in the toddler segment.

Research Methodology for North America Baby Carriers Market

The North America Baby Carriers market research involved a structured methodology including primary and secondary research, market sizing, and validation of forecasts. Primary research included interviews with over 50 manufacturers, distributors, and industry experts, capturing insights on production, sales volume, and consumer behavior. Secondary research leveraged industry reports, trade journals, company annual reports, and government statistics to identify historical trends and growth drivers. Market size estimation employed a bottom-up approach using production volumes from 2022–2025, combined with revenue data from leading manufacturers. Forecasts were derived using a CAGR-based projection model, validated through triangulation of supply-side data, demand-side metrics, and competitive landscape analysis. This methodology ensures accurate, data-driven insights for the North America Baby Carriers market size, share, growth, and demand trends.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Consumer Behavior and Premium Product Segments

Mandy Davis is a market research analyst with 7–9 years of experience specializing in consumer goods and services markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.