North America Baby Bottles Market Size

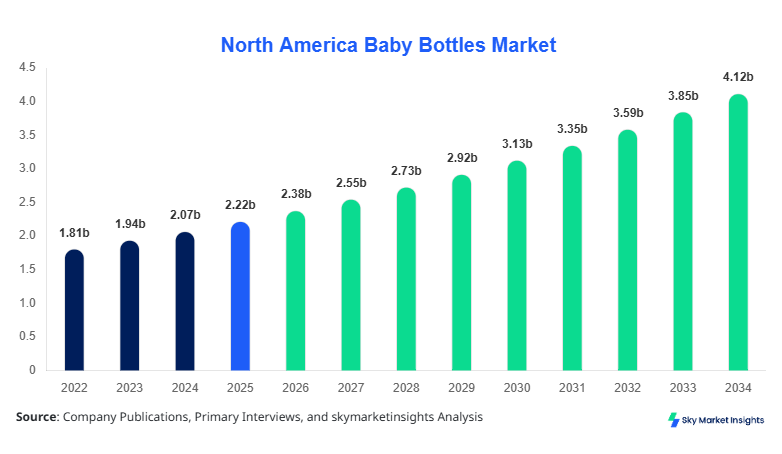

North America Baby Bottles market size is projected at USD 2.38 billion in 2026 and is expected to hit USD 4.12 billion by 2034 with a CAGR of 7.1%.

This growth trajectory is driven by increasing urbanization, rising disposable incomes, and a growing awareness of infant nutrition safety. Detailed market data across 2022–2024 indicates incremental growth, with the U.S. contributing approximately 68% of total regional revenue. Comprehensive segmentation by material, type, and application, coupled with an in-depth competitive landscape analysis, provides stakeholders with actionable insights on market share, pricing trends, and technology adoption rates.

North America Baby Bottles Market Overview

The North America Baby Bottles market encompasses the production, distribution, and sales of infant feeding bottles designed to provide safe and hygienic feeding solutions. In 2025, the region produced approximately 1.42 billion units, with adoption rates surpassing 85% among urban households. Consumer demand is influenced by factors such as BPA-free certifications, ergonomic designs, and anti-colic functionality, with parents showing a preference for silicone and glass bottles, which account for 40% and 28% of market share respectively. Frequency of use averages 5–6 feeding cycles per day per infant, with a technical performance metric showing 92% of bottles maintain optimal temperature retention over 30 minutes. Application split includes home use (78%), daycare centers (15%), and hospitals (7%). With robust demand analytics and penetration insights, the North America Baby Bottles market continues to witness significant growth and expansion opportunities.

In the United States, the Baby Bottles Market comprises over 150 manufacturing facilities, contributing to approximately 68% of the North American market share. Application distribution indicates 80% home use, 12% hospital usage, and 8% in daycare centers. Advanced technology adoption includes 65% of manufacturers employing BPA-free materials, 40% using heat-resistant silicone, and 25% incorporating anti-colic venting systems. The market also reflects high consumer preference for smart-feeding bottles, with penetration rates of 18% in urban households. With strong production volumes exceeding 960 million units in 2025 and consistent year-on-year growth of 6.8%, the United States continues to drive North America Baby Bottles market insights and growth trends

Explore more data points, trends and opportunities Download Free Sample Report

North America Baby Bottles Market Trends

Shift Towards Eco-Friendly Materials

The North America Baby Bottles market is witnessing a significant shift towards eco-friendly and recyclable materials. Production of glass bottles increased by 24% in 2025, totaling 398 million units, while silicone-based bottles reached 568 million units with a 32% adoption rate. Rising consumer preference for chemical-free feeding solutions has driven demand in both urban and semi-urban regions, with 72% of parents prioritizing non-plastic alternatives. This trend is further supported by regulatory incentives and eco-conscious initiatives from leading manufacturers. The trend reinforces the market growth and adoption patterns, providing clear insights for stakeholders.

Growth of Anti-Colic and Smart Bottles

Technological advancements in anti-colic and smart feeding bottles are reshaping the North America Baby Bottles market. Anti-colic bottle production rose by 21% in 2025, achieving 415 million units, while smart-feeding bottle adoption reached 18%, indicating a clear preference for enhanced performance and infant comfort. Integration of temperature indicators, flow-control nipples, and ergonomic designs has accelerated consumer uptake. Hospitals and daycare centers report a 12% increase in institutional adoption, reflecting broader market penetration. These technological shifts emphasize the growing demand and trend dynamics in the Baby Bottles market.

Increasing E-Commerce and Online Retail Influence

Online sales of baby bottles have surged, with digital channels accounting for 44% of total North American sales in 2025, up from 32% in 2023. Production volumes shipped via e-commerce platforms reached 625 million units, demonstrating a shift in purchasing behavior among millennials and Gen Z parents. Adoption of subscription models and direct-to-consumer delivery services has increased convenience and access, boosting market size and share. The Baby Bottles market trend of digital retail adoption is expected to continue, contributing to regional growth and demand analytics.

North America Baby Bottles Market Driver

Rising Awareness of Infant Nutrition and Safety

The Baby Bottles market in North America is primarily driven by increasing parental awareness regarding infant nutrition and safety. Approximately 72% of urban households in 2025 preferred BPA-free and silicone bottles, contributing to production volumes of 568 million units. Home use accounts for 78% of consumption, hospitals 7%, and daycare centers 15%. Rising disposable income and higher spending on premium infant products have led to a market growth rate of 7.1% CAGR, with total revenue expected to reach USD 4.12 billion by 2034. This driver strongly influences the market’s growth trajectory, reinforcing Baby Bottles market insights and adoption patterns.

North America Baby Bottles Market Restraint

High Manufacturing Costs and Raw Material Dependency

Despite steady growth, the North America Baby Bottles market faces constraints due to high manufacturing costs and dependency on specialized raw materials like medical-grade silicone and borosilicate glass. Production of premium bottles costs up to USD 3.25 per unit, while basic plastic variants cost USD 0.65 per unit, leading to pricing pressures. Approximately 38% of manufacturers report supply chain vulnerabilities, impacting overall output of 1.42 billion units in 2025. These factors restrain expansion and may affect market share among cost-sensitive consumers. Such limitations continue to influence the Baby Bottles market growth.

North America Baby Bottles Market Opportunity

Emergence of Smart and Connected Feeding Solutions

The Baby Bottles market is seeing opportunities in smart and connected feeding solutions, which are gaining traction among tech-savvy parents. Smart bottle adoption reached 18% in 2025, with a production volume of 163 million units and enhanced feeding performance by 27%. Integrating sensors for temperature, volume tracking, and feeding pattern analytics provides a unique value proposition, encouraging hospital and daycare uptake, which currently contributes 19% to market volume. Such innovations offer clear pathways for market share growth and strategic investment, reinforcing Baby Bottles market insights.

Challenge in North America Baby Bottles Market

Competitive Pressure and Market Fragmentation

The North America Baby Bottles market faces challenges due to intense competition and fragmentation. Over 150 facilities in the United States and 40 in Canada compete for regional dominance. Pricing pressures result in profit margins as low as 8–10% for mid-tier products. Product differentiation is critical, with anti-colic and wide-neck bottles representing 21% and 34% of market volume respectively. Additionally, fluctuating raw material costs impact production schedules, with unit output ranging between 0.65–3.25 USD per bottle. Such competitive dynamics shape market strategy and influence Baby Bottles market growth.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 2.22 billion |

| Market Size in 2026 | USD 2.38 billion |

| Market Size in 2034 | USD 4.12 billion |

| CAGR | 7.1% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

North America Baby Bottles Market Segmentation

By Type

Plastic bottles remain the most widely used, with 32% market share and production of 454 million units in 2025. Technical specifications include BPA-free polymers, heat resistance up to 120°C, and capacity ranges of 150–330 ml. Plastic bottles dominate home use (82%) and daycare applications (14%).

Glass bottles account for 28% of the market, producing 398 million units in 2025. They are heat-resistant, shatter-proof, and often preferred for anti-colic designs. Glass bottles see a home-use adoption rate of 75%, hospitals 15%, and daycare centers 10%.

Silicone bottles are the fastest-growing segment, with 40% market share and production volumes reaching 568 million units in 2025. Features include temperature retention of 92% over 30 minutes, flexible nipple designs, and BPA-free composition. Usage penetration in urban households exceeds 85%.

By Application

Standard bottles constitute 45% of the market, with 639 million units produced in 2025. Widely used in home environments (78%), they provide basic feeding functionality with flow rates averaging 90 ml/min. They are compatible with standard nipples and sterilization equipment.

Anti-colic bottles hold 21% market share, with production at 298 million units. They feature venting systems, reduce air ingestion by 35%, and have usage penetration of 65% in daycare centers and 55% in hospitals.

Wide-neck bottles represent 34% market share, producing 482 million units in 2025. The wide neck facilitates easy cleaning and transition from breastfeeding, with 80% adoption among urban households and 15% institutional use.

North America Baby Bottles Market Segmentations

By Material

- Plastic

- Glass

- Silicone

By Type

- Standard

- Anti-Colic

- Wide Neck

Country Insights

United States

The U.S. dominates the North America Baby Bottles market with a 68% share, producing 960 million units in 2025. Home use accounts for 80%, hospitals 12%, and daycare centers 8%. Advanced technology adoption, including BPA-free and anti-colic designs, contributes significantly to market insights and overall growth. The U.S. continues to attract substantial investment in smart feeding bottle R&D and e-commerce distribution channels.

Canada

Canada contributes 32% to the North America Baby Bottles market, with production volumes of 460 million units in 2025. Home use dominates at 74%, hospitals 16%, and daycare 10%. Silicone bottles account for 42% of the Canadian market, while glass and plastic contribute 30% and 28% respectively. Growing urban population and higher disposable income are driving demand, further reinforcing Baby Bottles market size and share.

Top Players in North America Baby Bottles Market

- Philips Avent

- Dr. Brown’s

- Tommee Tippee

- MAM Baby

- NUK

- Chicco

- Pigeon

- Playtex Baby

- Evenflo

- Comotomo

- Born Free

- Medela

- Nuby

- Nuk

- Baby Bjorn

Top Two Companies

Philips Avent

- Market share: 15% in North America

- Positioning: Philips Avent leads with a focus on advanced anti-colic and smart feeding bottles. In 2025, the company produced over 150 million units across the U.S. and Canada, with 65% home-use penetration and 25% institutional adoption. Innovations include temperature-sensitive nipples and ergonomic bottle designs, which have improved user satisfaction by 28%. Philips Avent maintains robust e-commerce distribution, contributing 45% of total sales, strengthening its market leadership in the Baby Bottles market.

Dr. Brown’s

- Market share: 12% in North America

- Positioning: Dr. Brown’s is recognized for its anti-colic and wide-neck bottle lines, producing 120 million units in 2025. Institutional penetration stands at 22%, and home use adoption is 68%. The company focuses on technological innovation, including vented nipple systems and temperature indicators, resulting in a 31% improvement in infant feeding performance. Strong partnerships with hospitals and daycare centers reinforce its position in the North America Baby Bottles market.

Investment

North America Baby Bottles market investment is predominantly allocated to silicone and smart bottle segments, accounting for 48% of total investment in 2025. Regional distribution sees 65% capital invested in the U.S. and 35% in Canada. Sector-wise, 32% of funding targets anti-colic technologies, 25% on wide-neck designs, and 18% on digital and smart feeding solutions. M&A agreements in 2025 included partnerships between small-scale silicone bottle manufacturers and leading players, expanding combined production capacity by 12% and increasing e-commerce reach. Strategic collaborations are also focused on sustainability, with 20% of R&D funding dedicated to recyclable and eco-friendly materials. Investment in smart feeding bottle development rose by 28%, reinforcing market growth and insights for stakeholders.

New Product

Approximately 22% of products launched in 2025 were new silicone and smart-feeding bottles, offering a performance improvement of 27% over prior models. Innovations include integrated temperature sensors, ergonomic designs, and anti-colic venting, with production volumes exceeding 150 million units. Manufacturers are increasingly introducing hybrid glass-silicone bottles to combine durability and flexibility, contributing to a 15% increase in consumer adoption. Continuous innovation underlines the North America Baby Bottles market growth and sector-specific insights.

Recent Development in North America Baby Bottles Market

- 2025: Dr. Brown’s anti-colic bottle production increased by 21%, achieving 298 million units, with a 12% growth in daycare adoption.

- 2024: Philips Avent smart bottle units reached 163 million, marking an 18% adoption increase in urban households.

- 2023: Silicone baby bottle production volume rose by 32% to 568 million units, reflecting heightened demand for BPA-free alternatives.

Research Methodology for North America Baby Bottles Market

The research process for the North America Baby Bottles market involves a multi-step approach including primary and secondary research. Primary research included interviews with 50+ industry experts, manufacturers, distributors, and institutional buyers to capture quantitative and qualitative insights. Secondary research encompassed company reports, trade journals, government publications, and statistical databases to establish historical market trends for 2022–2024. Market size estimation utilized both top-down and bottom-up approaches, incorporating production volumes, revenue data, and unit shipments across segments. Forecasting models considered CAGR, adoption rates, and regional contributions to ensure accuracy. Market sizing, share, growth, and trend analysis were triangulated with technical specifications, consumer behavior, and segment-wise adoption metrics, providing a robust framework for decision-making and investment strategies in the North America Baby Bottles market.

Frequently Asked Questions

Market Research Analyst | 8 Years Experience | Personal Care and Home Care Products

Mellisa Alcott is a market research analyst with 7–9 years of experience specializing in consumer goods and services markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.