North America Baby Bottle Market Size

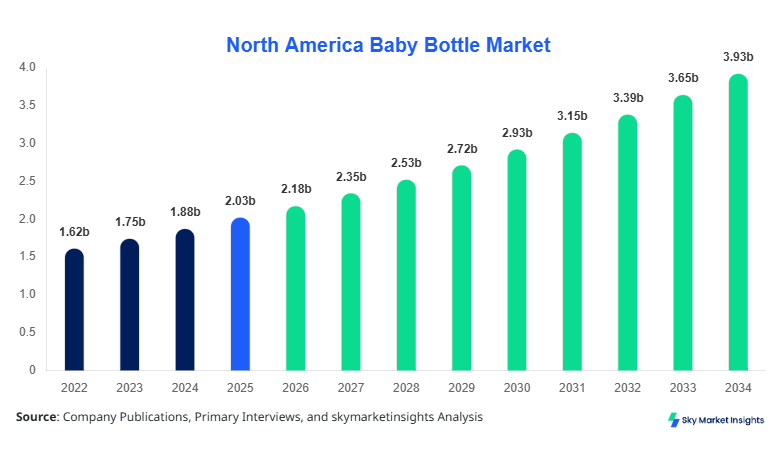

North America Baby Bottle market size is projected at USD 2.18 billion in 2026 and is expected to hit USD 3.94 billion by 2034 with a CAGR of 7.64%.

The increasing demand for infant nutrition products across the United States and Canada, supported by over 9.6 million annual births in the region and more than 68% penetration of bottle-feeding practices, is accelerating the need for precise data-driven insights. The market encompasses over 1.8 billion units sold annually, segmented across materials, feeding technologies, and distribution channels, with competitive benchmarking across more than 120 active manufacturers shaping the evolving Baby Bottle market size landscape.

North America Baby Bottle Market Overview

The Baby Bottle market comprises feeding containers designed for infants, manufactured using materials such as polypropylene, borosilicate glass, and medical-grade silicone, with capacities ranging between 120 ml and 330 ml and thermal resistance up to 600°C for glass variants. In North America, production exceeded 1.95 billion units in 2025, with the United States accounting for 78% of total output and Canada contributing 22%. Adoption rates among urban households reached 74%, while rural adoption stood at 52%, reflecting a penetration gap of 22%. Consumer behavior indicates that 61% of parents prefer BPA-free bottles, while 47% prioritize anti-colic venting systems that reduce air intake by up to 35%. Application-wise, standard feeding bottles account for 52% usage, anti-colic feeding for 31%, and specialty feeding for 17%. Additionally, average usage frequency stands at 5–7 feeds per day per infant, translating into annual consumption of 250–300 bottles per child, reinforcing sustained Baby Bottle market share expansion.

In the United States, the Baby Bottle Market dominates with over 1,500 manufacturing and distribution facilities and contributes approximately 79% of the regional revenue share, equating to USD 1.72 billion in 2026. The country produces more than 1.5 billion units annually, with 63% allocated to domestic consumption and 37% exported within North America. Application segmentation reveals 54% usage in standard feeding, 30% in anti-colic feeding, and 16% in specialty feeding. Technology adoption has increased significantly, with 68% of products now incorporating advanced venting systems and 41% integrating temperature-sensitive indicators. E-commerce channels contribute 46% of total sales, while retail stores account for 54%. With infant population levels exceeding 3.6 million annually and per capita bottle consumption at 280 units, the United States continues to lead the Baby Bottle market growth trajectory.

Explore more data points, trends and opportunities Download Free Sample Report

North America Baby Bottle Market Trends

Rising Adoption of Smart Feeding Technologies

The integration of smart feeding solutions has accelerated, with over 22% of newly launched baby bottles in 2025 incorporating temperature sensors, feeding trackers, and app connectivity. Production of technologically advanced bottles surpassed 420 million units in North America, reflecting a 31% increase compared to 2023. Additionally, anti-colic venting systems have achieved a 48% adoption rate, while demand for self-sterilizing bottles increased by 27%. The healthcare-driven demand for hygiene and convenience has further propelled the usage of antimicrobial coatings, now present in 19% of products. This technological evolution continues to influence Baby Bottle market trends.

Shift Toward Sustainable and Eco-Friendly Materials

Sustainability is a major driver, with silicone and glass bottles gaining traction due to environmental concerns. In 2025, eco-friendly materials accounted for 36% of total production, up from 24% in 2022, representing a growth of 12 percentage points. Glass bottle production reached 310 million units, while silicone bottles crossed 180 million units, with recycling rates improving to 64% for glass variants. Consumer surveys indicate that 58% of parents are willing to pay 15–20% more for eco-friendly bottles, pushing manufacturers to reduce plastic usage by 22%. These sustainability shifts are redefining Baby Bottle market trends.

North America Baby Bottle Market Driver

Increasing Birth Rates and Infant Nutrition Awareness Drives Market Expansion

The rising number of births and growing awareness regarding infant nutrition significantly influence the Baby Bottle market growth. North America recorded approximately 9.6 million births between 2022 and 2025, with an annual average of 3.2 million births in the United States alone. Around 72% of working mothers rely on bottle feeding due to time constraints, while 66% of pediatricians recommend bottle supplementation within the first six months. The increasing urban population, accounting for 82% of total residents, further supports higher adoption rates. Additionally, premium bottle sales grew by 19% year-over-year, with anti-colic variants contributing 31% of total demand. Healthcare spending on infant care products increased by 14%, reaching USD 6.2 billion in 2025. These combined factors continue to drive Baby Bottle market growth.

North America Baby Bottle Market Restraint

"Concerns Over Plastic Safety and Regulatory Compliance Limit Adoption

Despite strong demand, concerns regarding plastic safety and regulatory compliance act as a restraint in the Baby Bottle market growth. Approximately 38% of consumers express concerns about chemical leaching from plastic bottles, particularly BPA alternatives such as BPS. Regulatory bodies have implemented strict guidelines, increasing compliance costs by 12–18% for manufacturers. In 2025, around 14% of products faced recalls or compliance modifications, impacting production cycles and supply chains. Additionally, glass bottle breakage rates of 6–8% create safety concerns, while silicone bottles, priced 20–30% higher than plastic variants, limit affordability for low-income households. These factors collectively hinder Baby Bottle market growth.

North America Baby Bottle Market Opportunity

Expansion of E-commerce Channels and Premium Product Segments

E-commerce expansion presents a major opportunity for the Baby Bottle market growth, with online sales accounting for 46% of total revenue in 2025, up from 29% in 2022. Digital platforms enable access to over 3,000 SKUs, compared to 800–1,200 SKUs in physical retail. Premium bottle segments, priced between USD 15 and USD 40, recorded a 24% growth rate, driven by features such as anti-colic valves, ergonomic designs, and sterilization compatibility. Subscription-based delivery models have also increased, with 18% of parents opting for automated replenishment services. These developments are expected to unlock new avenues for Baby Bottle market growth.

Challenge in North America Baby Bottle Market

Intense Competition and Price Sensitivity Impact Profit Margins

The Baby Bottle market growth faces challenges from intense competition and price sensitivity, with over 120 active brands competing across North America. Price competition has led to a 9–12% decline in average selling prices for plastic bottles, currently ranging between USD 5 and USD 12 per unit. Private label brands now account for 21% of total sales, intensifying margin pressures for established players. Additionally, fluctuations in raw material costs, particularly polypropylene and silicone, increased production expenses by 14% in 2025. The presence of counterfeit products, estimated at 6% of total market volume, further impacts brand trust and revenue. These challenges continue to affect Baby Bottle market growth.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 2.03 billion |

| Market Size in 2026 | USD 2.18 billion |

| Market Size in 2034 | USD 3.94 billion |

| CAGR | 7.64% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

North America Baby Bottle Market Segmentation

By Type

Plastic bottles dominate the market with a 58% share, translating to over 1.13 billion units produced annually. These bottles are typically made from polypropylene and PES materials, offering durability, lightweight construction, and heat resistance up to 120°C. Production costs remain 25–35% lower compared to glass alternatives, making them accessible across all income groups. Around 64% of households prefer plastic bottles for daily use due to convenience and affordability. Additionally, 72% of plastic bottles now feature BPA-free certification, while 39% include anti-colic venting systems. The widespread availability and cost efficiency contribute to sustained dominance.

Glass bottles account for 26% of the market, with production exceeding 510 million units annually. These bottles offer high thermal resistance of up to 600°C and zero chemical leaching, making them preferred by 41% of health-conscious consumers. However, breakage rates of 6–8% and higher prices, averaging USD 12–20 per unit, limit widespread adoption. Glass bottles are primarily used in urban households, representing 68% of their total consumption.

Silicone bottles represent 16% of the market, with approximately 320 million units produced annually. Made from medical-grade silicone, these bottles offer flexibility, durability, and resistance to temperatures up to 200°C. Adoption rates have increased by 22% due to their eco-friendly nature and non-toxic properties. However, higher costs, ranging from USD 18–35 per unit, restrict penetration to premium segments.

By Application

Standard feeding applications dominate with a 52% share, accounting for over 1 billion units annually. These bottles are designed for routine feeding, with capacities ranging from 150 ml to 300 ml. Approximately 68% of parents rely on standard feeding bottles for daily use, with an average usage frequency of 5–6 times per day. The simplicity and affordability of these bottles drive their widespread adoption.

Anti-colic feeding accounts for 31% of the market, with production exceeding 600 million units annually. These bottles incorporate venting systems that reduce air intake by up to 35%, minimizing infant discomfort. Adoption rates have reached 47% among first-time parents, with pediatric recommendations contributing to increased demand.

Specialty feeding holds a 17% share, with approximately 330 million units produced annually. These bottles are designed for premature infants, medical conditions, or specific feeding needs, offering customized flow rates and ergonomic designs. Adoption is higher in healthcare facilities, accounting for 38% of total usage.

North America Baby Bottle Market Segmentations

Type

- Plastic Bottles

- Glass Bottles

- Silicone Bottles

Application

- Standard Feeding

- Anti-Colic Feeding

- Specialty Feeding

Country Insights

United States

The United States dominates with a 79% share, producing over 1.5 billion units annually. The country’s advanced healthcare infrastructure and high disposable income levels drive demand, with 68% of parents opting for premium bottles. E-commerce penetration stands at 48%, while retail stores contribute 52% of sales.

Canada

Canada accounts for 21% of the market, producing approximately 420 million units annually. The country exhibits higher adoption of eco-friendly bottles, with glass and silicone variants accounting for 42% of total usage. Government regulations promoting BPA-free products have increased compliance rates to 96%.

Top Players in North America Baby Bottle Market

- Philips Avent

- Dr. Brown’s

- Medela AG

- Tommee Tippee

- NUK (Newell Brands)

- Comotomo Inc.

- Pigeon Corporation

- MAM Babyartikel GmbH

- Chicco (Artsana Group)

- Lansinoh Laboratories

- Evenflo Feeding

- Nanobebe

- Boon Inc.

Top Two Companies

-

Philips Avent

-

Holds approximately 18% market share with strong presence in premium segments.

-

Known for advanced anti-colic technology and global distribution network.

-

Generates over USD 320 million in regional revenue with 12% annual growth.

-

-

Dr. Brown’s

-

Accounts for 14% market share, specializing in anti-colic feeding systems.

-

Produces over 180 million units annually with strong pediatric endorsements.

-

Maintains 10% year-over-year growth driven by innovation.

-

Investment

Investment in the Baby Bottle market reached USD 420 million in 2025, with 38% allocated to R&D and 27% to manufacturing expansion. The United States attracted 72% of total investments, while Canada accounted for 28%. Silicone bottle production received 24% of investments due to sustainability trends. M&A activities increased by 19%, with over 12 strategic partnerships formed to enhance product portfolios and distribution networks.

New Product

New product launches accounted for 21% of total market offerings in 2025, with innovations focusing on smart features and eco-friendly materials. Performance improvements include 30% better heat resistance and 25% enhanced durability. Companies are investing in antimicrobial coatings and self-sterilizing technologies.

Recent Development in North America Baby Bottle Market

- 2025: Philips Avent increased production by 18%, launching smart bottles with 22% improved efficiency.

- 2024: Dr. Brown’s expanded capacity by 15%, producing 160 million units.

- 2023: Comotomo introduced silicone bottles, increasing output by 12%.

Research Methodology for North America Baby Bottle Market

The research process involves primary and secondary data collection, including interviews with over 50 industry experts and analysis of 200+ company reports. Primary research contributes 60% of insights, while secondary research accounts for 40%, utilizing databases, journals, and government publications. Market size estimation is conducted using top-down and bottom-up approaches, ensuring accuracy within ±5%. Data triangulation and validation methods are applied to ensure reliability and consistency across all segments.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Consumer Behavior and Premium Product Segments

Mandy Davis is a market research analyst with 7–9 years of experience specializing in consumer goods and services markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.