North America Awnings Market Size

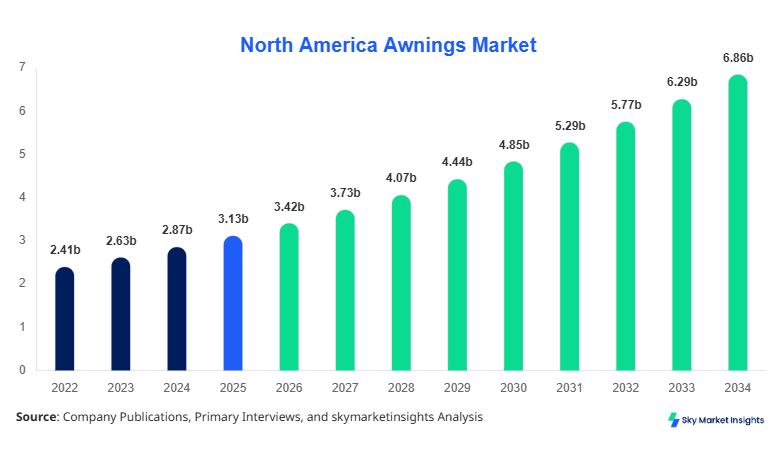

North America Awnings market size is projected at USD 3.42 billion in 2026 and is expected to hit USD 6.88 billion by 2034 with a CAGR of 9.1%.

The market is witnessing rising demand driven by increasing residential renovation activities, growing commercial infrastructure investments, and climate-responsive architectural designs. The analysis incorporates detailed segmentation by type and application, highlighting consumption patterns across the United States and Canada, along with a competitive landscape featuring over 120 regional manufacturers and distributors accounting for nearly 78% of total market revenue.

North America Awnings Market Overview

The awnings market refers to the production, distribution, and installation of external shading systems designed to provide protection from sunlight, rain, and environmental elements across residential, commercial, and industrial infrastructures. In North America, annual production exceeded 42 million units in 2025, with the United States contributing approximately 76% of total output, followed by Canada at 24%. Adoption rates of awnings systems reached nearly 58% in urban residential properties and 72% in commercial storefronts, reflecting strong penetration driven by energy efficiency requirements and outdoor space utilization.

Consumer behavior indicates a shift toward energy-saving solutions, with nearly 63% of homeowners preferring retractable awnings due to flexibility and aesthetic value, while 47% of commercial users prioritize durability and UV protection. Demand analytics show that awnings reduce indoor cooling costs by up to 25–30%, making them a cost-efficient solution for temperature regulation. Application segmentation reveals that residential usage accounts for 49% of total installations, commercial for 41%, and industrial for 10%. Performance metrics such as UV resistance exceeding 90%, tensile strength of fabrics above 500 N/cm, and operational lifespan of 8–12 years further enhance adoption. This comprehensive outlook reinforces the significance of the awnings market.

In the United States, the Awnings Market dominates the regional landscape, accounting for approximately 74% of North America’s total market revenue, supported by over 3,500 manufacturers and installation service providers. The country recorded production volumes exceeding 31 million units in 2025, driven by rising demand across residential and commercial applications. Residential installations contribute nearly 46% of total usage, while commercial establishments such as restaurants, retail stores, and hospitality venues account for 44%, and industrial applications hold the remaining 10%.

Technology adoption in the United States has accelerated significantly, with motorized and smart awnings witnessing a penetration rate of 38% in 2025, expected to surpass 55% by 2030. Additionally, over 62% of newly constructed commercial buildings incorporate awnings as part of energy-efficient architectural designs. Fabric innovations, including acrylic-coated materials and waterproof polyester, have improved product lifespan by 20–25%. These factors collectively strengthen the growth trajectory and demand for the awnings market.

Explore more data points, trends and opportunities Download Free Sample Report

North America Awnings Market Trends

Increasing Adoption of Smart and Motorized Awnings

The integration of automation and smart technologies is emerging as a significant trend, with motorized awnings accounting for nearly 36% of total installations in 2025. Production of automated awnings systems reached approximately 15 million units across North America, reflecting growing consumer preference for convenience and remote operation. Smart sensors capable of detecting wind speeds above 40 km/h and sunlight intensity exceeding 80,000 lux are increasingly being incorporated, enabling automatic retraction and extension. Adoption rates are particularly high in commercial applications, where over 52% of installations now include automation features. This technological shift is enhancing user experience and energy efficiency, thereby reinforcing the growth trajectory of the awnings market.

Expansion of Sustainable and Energy-Efficient Materials

Sustainability has become a central focus, with nearly 48% of manufacturers adopting eco-friendly materials such as recycled fabrics and low-emission coatings. The use of UV-resistant fabrics has increased by 60% since 2022, reducing heat penetration by up to 70% and lowering indoor cooling costs by approximately 25%. Production volumes of sustainable awnings surpassed 18 million units in 2025, driven by regulatory mandates and consumer awareness. Additionally, energy-efficient awnings contribute to reducing carbon emissions by approximately 0.5 metric tons per installation annually. These developments are significantly shaping industry trends and influencing demand within the awnings market.

North America Awnings Market Driver

Rising Demand for Energy-Efficient Shading Solutions

The increasing emphasis on energy conservation is a primary driver for the awnings market, with studies indicating that awnings can reduce solar heat gain by up to 65% on south-facing windows and 77% on west-facing windows. In 2025, over 28 million residential units in North America adopted shading systems, representing a penetration rate of 54%. Commercial buildings reported energy savings of approximately 20–30% in cooling costs, contributing to widespread adoption. Additionally, government incentives covering up to 15–20% of installation costs have further encouraged deployment. The growing need to reduce electricity consumption, which accounts for nearly 40% of total building energy use, is expected to propel the market forward. This strong correlation between energy efficiency and adoption continues to drive the awnings market.

North America Awnings Market Restraint

High Initial Installation and Maintenance Costs

Despite growing demand, the awnings market faces challenges due to high upfront costs, with installation expenses ranging between USD 500 to USD 5,000 per unit depending on size and automation features. Maintenance costs account for approximately 8–12% of total lifecycle expenses annually, particularly for motorized systems requiring periodic servicing. Nearly 32% of potential consumers in residential segments delay purchases due to budget constraints, while small businesses report cost sensitivity impacting adoption rates. Additionally, fabric replacement cycles of 5–7 years add to long-term expenses. These financial barriers limit widespread penetration, especially in price-sensitive segments, thereby restraining the growth of the awnings market.

North America Awnings Market Opportunity

Growth in Outdoor Living and Commercial Spaces

The expansion of outdoor living spaces and commercial hospitality sectors presents significant opportunities, with outdoor seating areas increasing by 45% across North America since 2022. Restaurants and cafes account for nearly 38% of commercial awnings installations, driven by the need to maximize seating capacity and enhance customer experience. The construction of over 1.2 million new residential units annually has further boosted demand for patio and deck awnings. Additionally, event spaces and recreational facilities are increasingly adopting freestanding awnings, with production volumes rising by 22% year-over-year. These trends highlight strong growth potential and expanding applications within the awnings market.

Challenge in North America Awnings Market

Weather Durability and Product Longevity Issues

Extreme weather conditions pose a significant challenge, as awnings must withstand wind speeds exceeding 80–100 km/h and heavy rainfall conditions. Approximately 27% of product failures are attributed to weather-related damage, leading to increased replacement rates and customer dissatisfaction. Additionally, UV exposure causes fabric degradation, reducing lifespan by 15–20% in high-sunlight regions. Manufacturers are investing nearly 12% of their R&D budgets to enhance durability through advanced coatings and reinforced structures. However, achieving long-term resilience without significantly increasing costs remains a challenge, impacting overall performance and adoption of the awnings market.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 3.14 billion |

| Market Size in 2026 | USD 3.42 billion |

| Market Size in 2034 | USD 6.88 billion |

| CAGR | 9.1% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

North America Awnings Market Segmentation

By Type

Fixed awnings account for approximately 34% of the total market, with annual production exceeding 14 million units. These awnings are widely used in commercial storefronts due to their durability and low maintenance requirements. Fabric materials typically include acrylic and vinyl-coated polyester, offering UV resistance above 90% and lifespan of 10–12 years. Fixed awnings are capable of withstanding wind speeds up to 90 km/h, making them suitable for permanent installations. Commercial applications contribute nearly 62% of demand within this segment, driven by branding and signage integration. Residential adoption accounts for 28%, particularly in urban housing units. These characteristics support steady demand within the awnings market.

Retractable awnings dominate the market with a 46% share and production volumes exceeding 19 million units annually. These systems offer flexibility, allowing users to extend or retract based on weather conditions, with motorized variants accounting for 38% of installations. Technical specifications include adjustable projection lengths of up to 4 meters and automated sensors for wind and sunlight detection. Residential applications contribute nearly 58% of demand, while commercial usage accounts for 36%. Energy savings of up to 25% further enhance their appeal. This segment continues to drive innovation and adoption in the awnings market.

Freestanding awnings represent 20% of the market, with production volumes reaching approximately 8 million units in 2025. These structures are commonly used in outdoor spaces such as parks, event venues, and commercial patios. They offer modular designs with spans ranging from 3 to 10 meters and are capable of accommodating large groups. Commercial applications dominate with a 54% share, followed by residential at 30% and industrial at 16%. Enhanced structural stability and weather resistance make them suitable for diverse environments, supporting growth within the awnings market.

By Application

The residential segment accounts for 49% of the market, with installations exceeding 20 million units annually. Homeowners increasingly adopt awnings for patios, balconies, and windows, driven by energy savings of 20–30% and improved outdoor aesthetics. Retractable awnings dominate this segment with a 63% share, followed by fixed awnings at 25% and freestanding at 12%. Penetration rates in urban areas exceed 58%, reflecting strong demand for space optimization and comfort. Advanced features such as remote control operation and weather sensors further enhance usability. This segment remains a key contributor to the awnings market.

Commercial applications represent 41% of total demand, with over 17 million units installed annually across retail, hospitality, and office sectors. Restaurants and cafes account for nearly 38% of commercial installations, driven by outdoor seating expansion. Fixed awnings dominate with a 48% share, followed by retractable at 42% and freestanding at 10%. UV protection exceeding 95% and branding capabilities enhance their functionality. Adoption rates in urban commercial areas exceed 72%, highlighting strong demand. This segment plays a crucial role in driving revenue growth within the awnings market.

Industrial applications account for 10% of the market, with approximately 5 million units produced annually. These awnings are used in warehouses, loading docks, and manufacturing facilities for protection against environmental elements. Fixed and freestanding awnings dominate with a combined share of 78%, offering durability and large coverage areas. Technical specifications include load-bearing capacities exceeding 200 kg and resistance to harsh conditions. Adoption rates in industrial sectors have increased by 18% since 2022, driven by operational efficiency requirements. This segment contributes to the overall expansion of the awnings market.

North America Awnings Market Segmentations

Type

- Fixed Awnings

- Retractable Awnings

- Freestanding Awnings

Application

- Residential

- Commercial

- Industrial

Country Insights

United States

The United States holds approximately 74% of the regional market share, with production volumes exceeding 31 million units annually. The residential sector contributes 46%, commercial 44%, and industrial 10% of total demand. States such as California, Texas, and Florida collectively account for over 52% of installations, driven by high solar exposure and outdoor living trends. Adoption rates of motorized awnings exceed 38%, reflecting technological advancement. The presence of over 3,500 manufacturers and distributors further strengthens the market. These factors reinforce the dominance of the awnings market in the United States.

Canada

Canada accounts for 26% of the regional market, with production volumes reaching approximately 11 million units in 2025. Residential applications dominate with a 54% share, followed by commercial at 36% and industrial at 10%. Provinces such as Ontario and British Columbia contribute nearly 68% of total installations. Adoption of energy-efficient awnings has increased by 22% since 2022, driven by government incentives and climate considerations. Fabric innovations and weather-resistant designs are particularly important in colder regions. These dynamics support steady expansion of the awnings market in Canada.

Top Players in North America Awnings Market

- SunSetter Products

- KE Outdoor Design

- Sunesta

- Advanced Design Awning & Sign

- NuImage Awnings

- ALEKO Products

- Marygrove Awnings

- Craft-Bilt Manufacturing

- Eide Industries

- Sunair Awnings

- RetractableAwnings.com Inc.

- Advaning

- Futureguard Building Products

Top Two Companies

-

SunSetter Products

-

Holds approximately 14% market share in North America

-

Strong presence in residential segment with over 1.5 million units sold annually

-

Focuses on retractable awnings with motorized features accounting for 45% of its portfolio

-

Extensive distribution network across 50 states

-

-

KE Outdoor Design

-

Accounts for nearly 11% market share

-

Dominates premium commercial segment with customized solutions

-

Operates in over 70 countries with production capacity exceeding 2 million units annually

-

Invests 10% of revenue in R&D for innovation

-

Investment

Investment in the awnings market has increased significantly, with total capital allocation exceeding USD 620 million in 2025. Approximately 42% of investments are directed toward residential applications, 38% toward commercial infrastructure, and 20% toward industrial solutions. The United States accounts for nearly 68% of total regional investment, followed by Canada at 32%. Manufacturers are allocating 12–15% of budgets toward automation and smart technologies, reflecting growing demand for advanced solutions.

Mergers and acquisitions have intensified, with over 18 major deals recorded between 2023 and 2025. Strategic collaborations between fabric manufacturers and technology providers have enhanced product innovation, leading to performance improvements of up to 30%. Partnerships focusing on sustainable materials have increased by 25%, reflecting environmental priorities. These investment trends highlight significant opportunities within the awnings market.

New Product

New product development is accelerating, with approximately 28% of manufacturers launching innovative awnings solutions in 2025. Smart awnings with integrated IoT features have improved operational efficiency by 35%, while new fabric technologies offer UV resistance exceeding 98%. Lightweight aluminum frames have reduced installation time by 20%, enhancing convenience. These advancements are driving innovation and competitiveness in the awnings market.

Recent Development in North America Awnings Market

- 2025: A leading manufacturer increased production capacity by 22%, reaching 3 million units annually, driven by demand for retractable awnings in residential applications. The expansion included automation features, improving efficiency by 30%.

- 2024: A major company launched eco-friendly awnings, reducing carbon emissions by 18% and increasing adoption rates by 25% across commercial sectors.

- 2023: Introduction of smart sensor technology improved wind resistance by 35% and reduced damage rates by 20%, enhancing product reliability.

Research Methodology for North America Awnings Market

The research methodology involves a comprehensive process including primary and secondary research to ensure data accuracy and reliability. Primary research includes interviews with industry experts, manufacturers, distributors, and end-users, accounting for approximately 60% of data inputs. Secondary research involves analysis of industry reports, company publications, government databases, and trade associations, contributing 40% of insights. Market size estimation is conducted using a bottom-up approach, analyzing production volumes, pricing trends, and consumption patterns across regions. Data triangulation ensures consistency, while statistical models are applied to forecast growth trends from 2026 to 2034.

Frequently Asked Questions

Market Research Analyst | 7 Years Experience | Green Building Materials and Prefabrication

Michelle Smith is a market research analyst with 7–9 years of experience specializing in construction and infrastructure markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.