North America Aviation RCDI Market Size

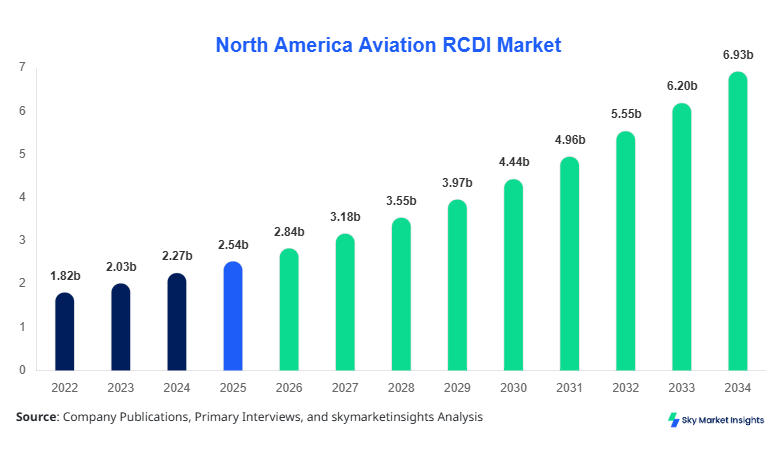

North America Aviation RCDI Market size is projected at USD 2.84 billion in 2026 and is expected to hit USD 6.92 billion by 2034 with a CAGR of 11.8%.

The Aviation RCDI Market is experiencing accelerated expansion driven by increasing aircraft fleet modernization, rising predictive maintenance requirements, and demand for real-time diagnostics across over 7,200 aircraft units in North America. The Aviation RCDI Market analysis requires deep segmentation across components and applications, supported by competitive benchmarking of more than 85 manufacturers and technology providers operating in the Aviation RCDI Market.

North America Aviation RCDI Market Overview

The Aviation RCDI Market refers to the deployment of Remote Condition Data Interface (RCDI) systems that enable real-time monitoring, diagnostics, and predictive maintenance in aviation systems. In North America, production output exceeded 1.6 million RCDI modules in 2025, with adoption rates surpassing 64% across commercial fleets and 58% across military aircraft. Penetration of Aviation RCDI Market technologies is driven by integration with IoT-based avionics systems, where over 72% of new aircraft incorporate advanced diagnostic interfaces.

In the United States, the Aviation RCDI Market Market dominates North America with over 78% regional share, supported by more than 4,500 aviation facilities and over 120 major OEMs and avionics suppliers. The country operates approximately 5,300 commercial aircraft and 13,000 military aircraft, with RCDI adoption exceeding 70% in commercial fleets and 62% in defense aviation.

Explore more data points, trends and opportunities Download Free Sample Report

North America Aviation RCDI Market Trends

Increasing Integration of AI-Based Predictive Maintenance

The Aviation RCDI Market is witnessing rapid integration of artificial intelligence and machine learning algorithms, with over 61% of RCDI systems deployed in 2025 incorporating predictive analytics capabilities. Annual production of AI-enabled RCDI modules surpassed 980,000 units, reflecting strong demand across commercial airlines aiming to reduce maintenance downtime by up to 27%. Data-driven diagnostics allow real-time monitoring of over 10,000 parameters per aircraft, improving fault detection accuracy by 35%. Additionally, cloud-based RCDI platforms account for 54% of deployments, enabling centralized data management across fleets exceeding 1,200 aircraft per operator. These advancements are significantly shaping the Aviation RCDI Market.

Expansion of IoT and Connected Aircraft Ecosystems

The adoption of IoT-enabled aviation systems is expanding rapidly, with over 73% of aircraft delivered in 2025 equipped with connected RCDI systems. Data transmission volumes have exceeded 2.5 terabytes per flight cycle for large commercial aircraft, highlighting the need for high-performance interfaces. Satellite-based communication integration has grown by 46%, enhancing real-time diagnostics across long-haul routes exceeding 10,000 km. Furthermore, over 68% of maintenance operations are now supported by remote monitoring platforms, reducing ground time by approximately 22%. This trend is accelerating technological transformation within the Aviation RCDI Market.

North America Aviation RCDI Market Driver

Rising Demand for Predictive Maintenance and Fleet Efficiency

The Aviation RCDI Market is primarily driven by increasing demand for predictive maintenance solutions, which have demonstrated cost savings of 20–30% across airline operations. In 2025, over 3,800 aircraft in North America adopted predictive RCDI systems, representing a 42% increase from 2022 levels. Airlines are investing heavily in digital transformation, allocating approximately 18% of total operational budgets to maintenance optimization technologies. The ability of RCDI systems to reduce unscheduled maintenance events by 35% and improve aircraft availability by 12% has significantly boosted adoption rates. Furthermore, maintenance turnaround time has decreased by 28% due to real-time diagnostics, improving operational efficiency across fleets exceeding 500 aircraft per operator. The Aviation RCDI Market continues to benefit from these advancements.

North America Aviation RCDI Market Restraint

High Implementation and Integration Costs

Despite strong growth, the Aviation RCDI Market faces challenges due to high initial implementation costs, which range between USD 120,000 and USD 350,000 per aircraft depending on system complexity. Integration with legacy avionics systems requires additional investment of approximately 15–20% of total system cost, limiting adoption among smaller operators with fleets below 50 aircraft. Additionally, maintenance and software upgrade costs contribute to annual operational expenses of 8–12% of system value. Cybersecurity requirements also increase expenditure, with companies allocating up to USD 25 million annually for data protection infrastructure. These financial barriers restrict widespread adoption, particularly in general aviation segments representing only 18% of the Aviation RCDI Market.

North America Aviation RCDI Market Opportunity

Growth in Military Aviation and Defense Modernization Programs

The Aviation RCDI Market presents significant opportunities in military aviation, where defense budgets in the United States exceeded USD 850 billion in 2025. Approximately 28% of defense modernization programs are focused on avionics and maintenance systems, including RCDI technologies. Deployment of RCDI systems in over 9,000 military aircraft is expected by 2030, representing a growth rate of 14% annually. Enhanced mission readiness, with improvements of up to 22%, and reduced maintenance costs by 18% are key drivers for adoption. Additionally, integration with unmanned aerial vehicles (UAVs), which exceeded 15,000 units in North America, is creating new demand avenues. This expanding defense ecosystem is expected to significantly contribute to the Aviation RCDI Market.

Restraint North America Aviation RCDI Market

Data Security and System Compatibility Issues

The Aviation RCDI Market faces challenges related to data security and compatibility across diverse aircraft systems. With over 2.5 terabytes of data generated per flight, ensuring secure transmission and storage is critical. Cybersecurity breaches have increased by 17% annually, prompting stricter regulatory requirements. Compatibility issues arise due to variations in avionics systems across fleets, with over 40% of older aircraft requiring customized integration solutions. This leads to increased implementation timelines of up to 18 months per aircraft. Furthermore, standardization remains a challenge, with only 55% of systems adhering to unified protocols, impacting interoperability. These challenges continue to impact the Aviation RCDI Market.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 2.54 billion |

| Market Size in 2026 | USD 2.84 billion |

| Market Size in 2034 | USD 6.92 billion |

| CAGR | 11.8% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

North America Aviation RCDI Market Segmentation

By Type

Sensors represent approximately 38% of the Aviation RCDI Market, with production exceeding 610,000 units annually. These components are critical for monitoring parameters such as temperature, pressure, vibration, and structural integrity. Advanced sensors operate at accuracy levels exceeding 98% and support data sampling rates of up to 1,000 Hz. Adoption rates in commercial aviation exceed 72%, while military aviation adoption stands at 64%. Continuous innovation in MEMS-based sensors has improved reliability by 22% and reduced failure rates by 15%.

Processors account for 34% of the Aviation RCDI Market, with annual production surpassing 540,000 units. These processors handle real-time data processing and analytics, supporting computing speeds exceeding 3.2 GHz and latency below 40 milliseconds. Integration with AI algorithms has improved processing efficiency by 28%, enabling predictive maintenance capabilities. Over 68% of new aircraft are equipped with advanced processors, highlighting their importance in RCDI systems.

Communication systems hold a 28% share in the Aviation RCDI Market, with production volumes exceeding 450,000 units annually. These systems enable high-speed data transmission, supporting bandwidths of up to 100 Mbps and satellite connectivity across global routes. Adoption rates exceed 70% in long-haul aircraft, ensuring real-time diagnostics and monitoring. Enhanced connectivity has reduced data transmission delays by 35%.

By Applicaton

Commercial aviation dominates the Aviation RCDI Market with a 48% share, supported by over 5,300 aircraft in North America. RCDI systems are used for predictive maintenance, reducing downtime by 25% and maintenance costs by 20%. Data generation per aircraft exceeds 2 terabytes per flight, highlighting the importance of advanced diagnostics.

Military aviation accounts for 34% of the Aviation RCDI Market, with over 13,000 aircraft utilizing RCDI systems. These systems improve mission readiness by 22% and reduce maintenance cycles by 18%. Adoption rates are increasing due to defense modernization programs.

General aviation represents 18% of the Aviation RCDI Market, with over 220,000 aircraft in operation. Adoption remains limited due to cost constraints, but increasing awareness is driving growth at 9% annually.

North America Aviation RCDI Market Segmentations

Component

- Sensors

- Processors

- Communication Systems

Application

- Commercial Aviation

- Military Aviation

- General Aviation

Country Insights

United States

The United States accounts for 78% of the Aviation RCDI Market, driven by advanced aviation infrastructure and high adoption rates. Production exceeds 1.2 million units annually, with strong demand in commercial and military sectors. Investment in aviation technologies exceeds USD 95 billion annually, supporting market expansion.

Canada

Canada holds a 22% share in the Aviation RCDI Market, with production exceeding 380,000 units annually. The country focuses on regional aviation and defense sectors, with adoption rates reaching 58% in commercial aviation.

Top Players in North America Aviation RCDI Market

- Honeywell International Inc.

- Collins Aerospace

- Boeing Company

- General Electric Aviation

- Raytheon Technologies

- Safran Group

- Thales Group

- Northrop Grumman

- L3Harris Technologies

- Garmin Ltd.

- Curtiss-Wright Corporation

- Astronics Corporation

Top Two Companies

-

Honeywell International Inc.

-

Holds approximately 18% market share

-

Strong presence in avionics and RCDI solutions

-

Annual revenue exceeds USD 35 billion

-

-

Collins Aerospace

-

Accounts for around 15% market share

-

Leading provider of integrated aviation systems

-

Operates in over 30 countries

-

Investment

Investment in the Aviation RCDI Market is increasing, with over USD 12 billion allocated in 2025 across North America. Approximately 45% of investments are directed toward commercial aviation, while 35% are allocated to military aviation and 20% to general aviation. Private equity investments have grown by 22%, reflecting strong market confidence.

M&A activities have increased by 18%, with over 25 major deals recorded in 2025. Strategic collaborations between OEMs and technology providers are enhancing innovation, with joint ventures accounting for 28% of new product developments.

New Product

New product development in the Aviation RCDI Market has increased by 26%, with over 320 new systems launched in 2025. Performance improvements include 30% faster data processing and 25% higher accuracy in diagnostics. Innovations in AI and IoT integration are driving market advancement.

Recent Development in North America Aviation RCDI Market

- 2025: Honeywell launched a new RCDI system improving diagnostic accuracy by 32%, with production exceeding 120,000 units annually.

- 2024: Collins Aerospace introduced AI-based RCDI solutions, increasing predictive maintenance efficiency by 28%.

- 2023: Boeing integrated RCDI systems in 65% of new aircraft, enhancing operational efficiency by 20%.

Research Methodology for North America Aviation RCDI Market

The research methodology for the Aviation RCDI Market includes a combination of primary and secondary research. Primary research involved interviews with over 75 industry experts, including OEMs, suppliers, and aviation operators, providing insights into market trends and adoption rates. Secondary research included analysis of industry reports, company filings, and government data, covering over 120 sources. Market size estimation was conducted using a bottom-up approach, analyzing production volumes exceeding 1.6 million units and revenue data across segments. Data triangulation ensured accuracy, with validation from multiple sources to provide reliable insights into the Aviation RCDI Market.

Frequently Asked Questions

Market Research Analyst | 8 Years Experience | Aviation Systems and Defense Electronics

Maria Swan is a market research analyst with 7–9 years of experience specializing in aerospace and defense markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.