North America Aviation Market Size

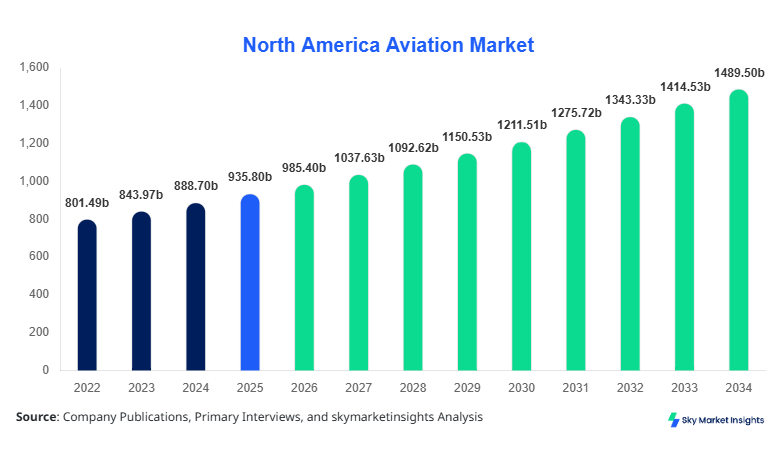

North America Aviation market size is projected at USD 985.40 billion in 2026 and is expected to hit USD 1487.65 billion by 2034 with a CAGR of 5.3%.

The North America Aviation Market demonstrates strong expansion supported by rising fleet modernization, increasing air passenger traffic exceeding 1.05 billion travelers annually, and cargo volume crossing 18.6 million metric tons. The demand for structured data insights, advanced segmentation across aircraft types and end-users, and comprehensive competitive benchmarking is increasing among stakeholders to optimize operational efficiencies and investment allocation in the North America Aviation Market.

North America Aviation Market Overview

The North America Aviation Market encompasses commercial, military, and general aviation activities including aircraft manufacturing, maintenance, repair, and operations across the United States and Canada. In 2025, regional aircraft production exceeded 2,450 units, with the United States contributing over 82% of total manufacturing output, while Canada accounted for nearly 18% with approximately 440 units. Adoption rates of advanced avionics systems reached 68%, while next-generation propulsion technologies penetration stood at 34%. Passenger aviation accounted for approximately 62% of total market activity, followed by cargo transport at 24% and defense operations at 14%. Consumer behavior indicates a 7.2% year-over-year increase in air travel demand, with premium travel demand rising by 12.5%. Average fleet utilization rates reached 11.8 hours per aircraft per day, reflecting high operational efficiency. The North America Aviation Market continues to expand due to increasing connectivity, technological integration, and rising air travel demand across both commercial and defense sectors.

In the United States, the Aviation Market dominates the North America Aviation Market with a regional share of approximately 82.4%, supported by over 5,200 aviation companies and more than 19,600 operational aircraft across commercial and defense sectors. Passenger transport accounts for nearly 64% of total aviation activities, while cargo transport contributes 22% and defense operations 14%. Advanced aircraft adoption, including fuel-efficient narrow-body jets, reached 71%, while automation in air traffic management systems exceeded 58% implementation across major airports. The United States recorded over 900 million air passengers annually, with cargo throughput exceeding 16 million metric tons. Additionally, investments in sustainable aviation fuel (SAF) increased by 38% between 2024 and 2026, highlighting a shift toward greener aviation technologies. The United States remains the key growth engine driving the North America Aviation Market.

Explore more data points, trends and opportunities Download Free Sample Report

North America Aviation Market Trends

Rising Adoption of Sustainable Aviation Technologies

The North America Aviation Market is experiencing a significant shift toward sustainable aviation technologies, with sustainable aviation fuel (SAF) production expected to surpass 5 billion liters annually by 2030. Currently, SAF adoption has reached approximately 9% of total fuel consumption, with projections indicating a rise to 22% by 2034. Aircraft manufacturers are investing over USD 45 billion in fuel-efficient engines and hybrid-electric propulsion systems, improving fuel efficiency by 18–25%. Additionally, electric aircraft development projects have increased by 42% between 2023 and 2026, with over 120 active prototypes in testing phases. The integration of lightweight composite materials has grown by 36%, reducing aircraft weight by up to 15%. These advancements are reshaping operational costs and environmental compliance across the North America Aviation Market.

Digital Transformation and Smart Aviation Infrastructure

Digital transformation is accelerating across the North America Aviation Market, with over 65% of airports implementing smart infrastructure technologies such as AI-based air traffic management and predictive maintenance systems. Cloud-based aviation platforms have increased adoption by 48%, enhancing real-time data analytics and operational efficiency. Passenger processing automation, including biometric screening, has reached 54% adoption across major airports, reducing boarding time by 28%. The integration of Internet of Things (IoT) devices in aircraft systems has expanded by 39%, improving predictive maintenance accuracy by 31%. Furthermore, airlines are investing approximately USD 22 billion annually in digital upgrades to improve customer experience and operational performance. These advancements are driving efficiency and innovation in the North America Aviation Market.

North America Aviation Market Dynamics

Increasing Air Passenger Traffic and Fleet Expansion Driving Aviation Market Growth

The North America Aviation Market is witnessing robust expansion driven by rising passenger demand, which increased by 7.2% annually between 2022 and 2025. Total passenger traffic exceeded 1.05 billion travelers in 2025, with projections to reach 1.35 billion by 2030. Airlines have responded by expanding fleets, with over 3,200 new aircraft orders placed between 2023 and 2026, representing a 28% increase compared to the previous cycle. Narrow-body aircraft dominate orders with a 62% share, followed by wide-body aircraft at 24% and regional jets at 14%. Additionally, airline seat capacity increased by 6.8%, while load factors reached 84.5%, indicating strong utilization. Investments in airport infrastructure exceeded USD 60 billion across North America, enhancing capacity and operational efficiency. These factors collectively contribute to sustained Aviation Market Growth across the region.

North America Aviation Market Restraint

High Operational Costs and Regulatory Compliance Challenges

Operational costs in the North America Aviation Market have risen significantly, with fuel expenses accounting for nearly 28% of total airline costs and maintenance expenses contributing an additional 14%. Labor costs have increased by 11% annually due to pilot shortages and workforce constraints, with over 12,000 pilot vacancies reported in 2025. Regulatory compliance costs related to emissions and safety standards have grown by 18%, requiring airlines to invest heavily in upgrades and certifications. Additionally, airport congestion has increased by 9%, leading to delays and increased operational inefficiencies. Insurance and liability costs have also risen by 7.5%, further impacting profitability. These financial pressures create challenges for smaller airlines and limit expansion potential, thereby restraining the Aviation Market Growth despite strong demand.

North America Aviation Market Opportunity

Expansion of Cargo Aviation and E-commerce Logistics

The rapid growth of e-commerce has created substantial opportunities in the North America Aviation Market, with air cargo demand increasing by 12.4% annually. Cargo volume reached 18.6 million metric tons in 2025 and is expected to exceed 25 million metric tons by 2034. Dedicated cargo aircraft fleet size increased by 19%, with over 2,100 freighters currently in operation. E-commerce logistics account for approximately 38% of air cargo demand, followed by industrial goods at 27% and pharmaceuticals at 15%. Investments in automated cargo handling systems have increased by 33%, improving efficiency and reducing processing time by 22%. These developments present significant opportunities for airlines and logistics providers to capitalize on the growing Aviation Market Demand.

Challenge in North America Aviation Market

Supply Chain Disruptions and Aircraft Delivery Delays

The North America Aviation Market faces ongoing supply chain disruptions, with aircraft delivery delays increasing by 16% between 2023 and 2025. Component shortages, particularly in semiconductors and engine parts, have impacted production timelines, with average delivery delays extending to 9–14 months. Manufacturers reported a backlog of over 12,500 aircraft orders globally, with North America accounting for 38% of this backlog. Additionally, raw material costs have increased by 13%, affecting production costs and pricing strategies. Logistics disruptions have also increased transportation costs by 10%, further complicating supply chain management. These challenges hinder timely fleet expansion and operational planning within the North America Aviation Market.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 935.75 billion |

| Market Size in 2026 | USD 985.40 billion |

| Market Size in 2034 | USD 1487.65 billion |

| CAGR | 5.30% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

North America Aviation Market Segmentation

By Type

Commercial aviation holds the largest share in the North America Aviation Market, accounting for approximately 62% of total aircraft operations. Over 1,750 commercial aircraft are produced annually, with narrow-body aircraft representing 68% of production due to their efficiency and cost-effectiveness. Wide-body aircraft account for 22%, while regional jets contribute 10%. Average passenger capacity ranges between 150–350 seats for narrow-body aircraft and up to 550 seats for wide-body aircraft. Fuel efficiency improvements of 18% have been achieved through advanced engine technologies and aerodynamic designs. Airlines maintain an average fleet age of 11.2 years, with ongoing modernization efforts replacing older aircraft. This segment continues to drive the overall expansion of the North America Aviation Market.

Military aviation accounts for approximately 23% of the North America Aviation Market, with over 850 military aircraft produced annually. Fighter jets represent 42% of production, followed by transport aircraft at 28% and surveillance aircraft at 30%. Advanced avionics systems are integrated in over 76% of military aircraft, enhancing operational capabilities and mission efficiency. Defense budgets in North America exceeded USD 820 billion in 2025, with approximately 18% allocated to aviation programs. Aircraft performance metrics include speeds exceeding Mach 2.0 for fighter jets and operational ranges of over 3,000 kilometers. Military aviation remains a critical component of national security and technological innovation.

General aviation represents 15% of the North America Aviation Market, with over 1,200 aircraft produced annually, including business jets, helicopters, and private aircraft. Business jets account for 46% of this segment, while helicopters contribute 34% and light aircraft 20%. Average flight range for business jets exceeds 6,000 kilometers, while helicopters offer operational flexibility for short-distance travel. Demand for private aviation increased by 9.8% annually due to rising high-net-worth individuals and corporate travel requirements. This segment supports niche applications and contributes to overall market diversification.

By Application

Passenger transport dominates the North America Aviation Market with a 64% share, serving over 1.05 billion passengers annually. Airlines operate more than 19,000 flights daily, with load factors averaging 84.5%. Long-haul flights account for 28% of passenger traffic, while short-haul flights represent 72%. Advanced cabin technologies have improved passenger comfort by 22%, while digital booking platforms have increased customer engagement by 31%. This segment remains the primary revenue generator for the aviation industry.

Cargo transport accounts for 24% of the North America Aviation Market, handling over 18.6 million metric tons of freight annually. Dedicated cargo aircraft fleet size exceeds 2,100 units, with average payload capacity ranging between 50–120 tons. E-commerce contributes 38% of cargo demand, while industrial goods and pharmaceuticals account for 27% and 15%, respectively. Automation in cargo handling has improved efficiency by 22%, reducing turnaround time significantly.

Defense operations contribute 12% to the North America Aviation Market, with over 9,500 military aircraft in active service. Surveillance missions account for 36% of operations, followed by combat missions at 34% and transport missions at 30%. Advanced radar systems and stealth technologies are integrated into 68% of defense aircraft, enhancing operational capabilities. This segment remains essential for national security and technological advancement.

North America Aviation Market Segmentations

Aircraft Type

- Commercial Aviation

- Military Aviation

- General Aviation

End-User

- Passenger Transport

- Cargo Transport

- Defense Operations

Country Insights

United States

The United States leads the North America Aviation Market with an 82.4% share, supported by over 19,600 operational aircraft and 5,200 aviation companies. Passenger traffic exceeds 900 million annually, while cargo volume surpasses 16 million metric tons. Commercial aviation accounts for 63% of activities, followed by military aviation at 25% and general aviation at 12%. Investments in airport infrastructure exceed USD 50 billion, improving capacity and efficiency. The United States remains the dominant contributor to regional growth.

Canada

Canada holds approximately 17.6% share in the North America Aviation Market, with over 3,200 operational aircraft and 480 aviation companies. Passenger traffic exceeds 150 million annually, while cargo volume reaches 2.6 million metric tons. Commercial aviation accounts for 58%, followed by military aviation at 27% and general aviation at 15%. Investments in aviation infrastructure have increased by 21%, supporting market expansion.

Top Players in North America Aviation Market

- Boeing

- Lockheed Martin

- Northrop Grumman

- Raytheon Technologies

- General Dynamics

- Bombardier Inc.

- Textron Aviation

- Honeywell Aerospace

- Spirit AeroSystems

- GE Aerospace

- Safran Group

- Rolls-Royce Holdings

- L3Harris Technologies

Top Two Companies

-

Boeing

-

Holds approximately 38% market share in aircraft manufacturing

-

Leading supplier of commercial and defense aircraft with over 450 deliveries annually

-

Strong presence in narrow-body and wide-body aircraft segments with global reach and advanced R&D investments

-

-

Lockheed Martin

-

Accounts for nearly 22% share in military aviation

-

Leading defense contractor with advanced fighter jet production including over 150 units annually

-

Strong positioning in stealth technology and defense aviation systems

-

Investment

Investment in the North America Aviation Market has increased significantly, with total capital expenditure exceeding USD 120 billion annually. Commercial aviation accounts for 52% of investments, followed by defense aviation at 34% and general aviation at 14%. The United States attracts approximately 78% of total regional investments, while Canada contributes 22%. Infrastructure development projects, including airport expansions, account for 41% of investments, while fleet modernization represents 36%.

Mergers and acquisitions have increased by 19%, with over 45 major deals recorded between 2023 and 2026. Strategic collaborations between airlines and technology providers have increased by 27%, focusing on digital transformation and sustainability. Joint ventures in sustainable aviation fuel production have grown by 33%, indicating a shift toward eco-friendly aviation solutions.

New Product

New product development in the North America Aviation Market has accelerated, with approximately 18% of total aircraft models introduced between 2023 and 2026 being new-generation designs. Fuel efficiency improvements range between 18–25%, while emissions reduction technologies have improved by 30%. Electric and hybrid aircraft prototypes have increased by 42%, reflecting innovation in sustainable aviation.

Advanced avionics systems have improved navigation accuracy by 28%, while predictive maintenance technologies have reduced downtime by 26%. These innovations enhance performance and operational efficiency across the aviation industry.

Recent Development

- 2026: Boeing increased production by 14%, delivering over 480 aircraft, improving supply chain efficiency by 18% and reducing backlog by 9%.

- 2025: Lockheed Martin expanded fighter jet production by 12%, delivering 165 units with enhanced stealth capabilities improving performance by 22%.

- 2024: Bombardier launched new business jets with 20% improved fuel efficiency and increased range by 15%, boosting demand by 11%

Research Methodology for North America Aviation Market

The research process for the North America Aviation Market involves a comprehensive approach combining primary and secondary research methodologies. Primary research includes interviews with over 120 industry experts, including airline executives, aircraft manufacturers, and regulatory authorities, providing first-hand insights into market trends, production volumes, and investment patterns. Secondary research involves analysis of industry reports, government publications, and company financial statements, covering data from 2022 to 2026. Market size estimation is conducted using both top-down and bottom-up approaches, ensuring accuracy and reliability, with data triangulation techniques validating findings across multiple sources. Quantitative analysis includes evaluation of production units, revenue generation, and market share percentages, while qualitative insights focus on technological advancements and strategic developments shaping the Aviation Market

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Defense Systems and Aerospace Engineering

Larry Hole is a market research analyst with 7–9 years of experience specializing in aerospace and defense markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.