North America Aviation Heads Up Display-HUD-Market Size

The North America Aviation Heads Up Display (HUD) market size reflects strong expansion driven by increasing aircraft production exceeding 1,250 units annually across the United States and Canada, alongside modernization programs covering over 68% of existing fleets. The integration of digital avionics and enhanced pilot situational awareness systems has accelerated adoption across commercial and defense sectors. The Aviation Heads Up Display (HUD) market size further highlights segmentation across types and applications, where helmet-mounted systems account for nearly 42% of installations while commercial aviation contributes approximately 38% of total demand. The competitive landscape remains consolidated, with the top five players holding over 63% market share, emphasizing technological leadership and high entry barriers in the Aviation Heads Up Display (HUD) market size.

North America Aviation Heads Up Display-HUD-Market Overview

The Aviation Heads Up Display (HUD) market in North America represents a technologically advanced segment of the aerospace industry focused on projecting critical flight data such as altitude, speed, and navigation directly into the pilot’s line of sight using optical combiner systems and high-resolution display technologies operating at refresh rates exceeding 60 Hz. In 2025, regional production of HUD systems surpassed 3,800 units, with penetration levels reaching 54% across newly delivered aircraft and over 39% across retrofitted fleets. Adoption and penetration insights indicate that military aviation accounts for nearly 46% of installations, driven by enhanced targeting and night vision integration, while commercial aviation follows with 38% share due to safety regulations and landing assistance systems. Consumer behavior analysis highlights that airlines prioritize HUD systems for reducing pilot workload by up to 27% and improving landing accuracy by 33% under low-visibility conditions. Business jets contribute approximately 16% of installations, with growing demand for compact HUD units weighing less than 2.5 kg and offering luminance levels above 10,000 cd/m². The Aviation Heads Up Display (HUD) market continues to expand with increasing demand for real-time data visualization and enhanced flight safety systems.

In the United States, the Aviation Heads Up Display (HUD) Market accounts for nearly 74% of the North American share, supported by over 250 aerospace manufacturing facilities and more than 120 avionics companies actively producing HUD components. The country produces over 2,900 HUD units annually, with military aviation representing 48% of demand, commercial aviation contributing 36%, and business jets accounting for 16%. Technology adoption rates exceed 61% in new aircraft deliveries, with over 45% of legacy fleets undergoing retrofitting programs. Advanced HUD systems integrated with augmented reality (AR) and synthetic vision systems are now deployed in over 28% of military aircraft, enhancing mission accuracy by 31% and reducing pilot response time by 22%. The United States also leads in R&D investment, allocating nearly USD 540 million annually toward avionics innovation. This strong industrial base and technological leadership reinforce the Aviation Heads Up Display (HUD) market.

Explore more data points, trends and opportunities Download Free Sample Report

North America Aviation Heads Up Display-HUD-Market Trends

Increasing Integration of Augmented Reality and Synthetic Vision Systems

The Aviation Heads Up Display (HUD) market is witnessing a significant shift toward augmented reality (AR) integration, with over 34% of newly installed systems incorporating AR overlays for terrain mapping and obstacle detection. Production of AR-enabled HUD units surpassed 1.2 million components globally in 2025, with North America contributing nearly 41% of this volume. Synthetic vision systems (SVS) adoption has increased by 29%, allowing pilots to visualize terrain in real time, even in zero-visibility conditions. The use of high-resolution microdisplay technologies exceeding 1080p resolution and brightness levels above 12,000 cd/m² is enhancing clarity and operational efficiency. These advancements are particularly prominent in military aircraft, where mission success rates have improved by 26%. This trend continues to strengthen the Aviation Heads Up Display (HUD) market.

Rising Demand for Lightweight and Compact HUD Systems

Another major trend shaping the Aviation Heads Up Display (HUD) market is the development of lightweight systems weighing less than 2 kg, reducing cockpit space usage by approximately 18%. Over 52% of new business jet deliveries now feature compact HUD units, driven by increasing demand for fuel efficiency and reduced aircraft weight. Production of miniaturized HUD components increased by 37% between 2023 and 2025, reaching over 1.6 million units. Additionally, advancements in waveguide optics and LED-based projection systems have improved energy efficiency by 21% and extended system lifespan by up to 40,000 operational hours. These innovations are accelerating adoption across multiple aviation segments, further supporting the Aviation Heads Up Display (HUD) market.

North America Aviation Heads Up Display-HUD-Market Driver

Increasing Focus on Flight Safety and Pilot Situational Awareness

The primary driver of the Aviation Heads Up Display (HUD) market is the growing emphasis on flight safety, with regulatory authorities mandating advanced avionics systems in over 63% of new aircraft deliveries. HUD systems have demonstrated a 35% reduction in pilot error rates and a 28% improvement in landing precision under adverse weather conditions. Annual aircraft production exceeding 1,200 units in North America further supports demand, with over 58% of these aircraft equipped with HUD systems. Airlines are investing nearly USD 2.3 billion annually in safety-enhancing technologies, including HUD integration. The ability of HUD systems to display real-time navigation data, terrain awareness, and flight path information significantly enhances pilot performance, driving strong adoption across commercial and military sectors, thereby reinforcing the Aviation Heads Up Display (HUD) market growth.

North America Aviation Heads Up Display-HUD-Market Restraint

High Installation and Maintenance Costs

Despite strong demand, the Aviation Heads Up Display (HUD) market faces challenges due to high installation costs ranging between USD 150,000 and USD 350,000 per unit, depending on system complexity. Maintenance costs account for nearly 18% of total lifecycle expenses, with component replacement cycles averaging every 5–7 years. Small and regional airlines with fleets below 50 aircraft often face budget constraints, limiting adoption rates to below 27%. Additionally, integration complexities with legacy avionics systems increase retrofit costs by up to 22%. These financial barriers hinder widespread adoption, particularly in cost-sensitive segments, posing a restraint to the Aviation Heads Up Display (HUD) market growth.

North America Aviation Heads Up Display-HUD-Market Opportunity

Expansion of Commercial Aviation and Fleet Modernization

The Aviation Heads Up Display (HUD) market presents significant opportunities driven by fleet modernization programs covering over 42% of aircraft in North America. Commercial aviation passenger traffic is expected to grow by 4.8% annually, leading to increased aircraft procurement exceeding 1,500 units by 2030. Retrofitting older aircraft with HUD systems offers a market potential exceeding USD 1.1 billion, with adoption rates projected to rise from 39% to 57% by 2034. Additionally, the integration of AI-based predictive analytics within HUD systems is expected to enhance operational efficiency by 24%. These factors create substantial opportunities for manufacturers, strengthening the Aviation Heads Up Display (HUD) market growth.

Challenge in North America Aviation Heads Up Display-HUD-Market

Technological Integration and Certification Complexities

A major challenge in the Aviation Heads Up Display (HUD) market is the complexity of integrating advanced systems with existing avionics and obtaining regulatory certifications. Certification processes can take up to 18–24 months, delaying product launches and increasing development costs by approximately 15%. Compatibility issues with legacy systems affect nearly 31% of retrofit projects, requiring additional customization. Furthermore, stringent FAA and Transport Canada regulations necessitate rigorous testing, increasing compliance costs by up to USD 5 million per system. These challenges impact time-to-market and limit scalability, posing obstacles to the Aviation Heads Up Display (HUD) market growth.

Report Scope

| Report Metric | Details |

|---|---|

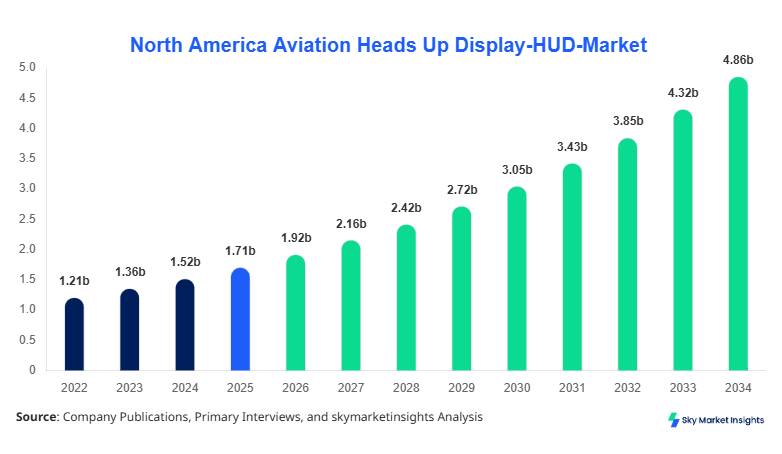

| Market Size in 2025 | USD 1.71 billion |

| Market Size in 2026 | USD 1.92 billion |

| Market Size in 2034 | USD 4.87 billion |

| CAGR | 12.3% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

North America Aviation Heads Up Display-HUD-Market Segmentation

By Type

Fixed HUD systems account for approximately 36% of the Aviation Heads Up Display (HUD) market, with annual production exceeding 1,300 units in North America. These systems are widely used in commercial aircraft due to their stable installation and high brightness levels exceeding 10,000 cd/m². Fixed HUDs operate with optical combiner technology and offer field-of-view angles up to 30 degrees, enhancing pilot visibility. Over 58% of commercial aircraft are equipped with fixed HUD systems, particularly for landing assistance and navigation. These systems reduce pilot workload by 25% and improve operational efficiency, making them a critical component in modern aviation.

Wearable HUD systems hold around 22% share, with production surpassing 800 units annually. These systems are primarily used in business jets and specialized military applications, offering flexibility and portability. With weight below 1.8 kg and battery life exceeding 6 hours, wearable HUDs provide enhanced mobility. Adoption rates in business jets have increased by 31%, driven by demand for compact avionics solutions. These systems deliver real-time data visualization with latency below 20 milliseconds, improving pilot responsiveness.

Helmet-mounted HUD systems dominate with a 42% share, driven by military aviation demand. Annual production exceeds 1,600 units, with advanced features such as night vision integration and target tracking. These systems provide a 40-degree field of view and operate at refresh rates above 70 Hz. Adoption rates in fighter aircraft exceed 78%, significantly enhancing mission success rates by 29%.

By Application

Commercial aviation accounts for 38% of the Aviation Heads Up Display (HUD) market, with over 1,400 units installed annually. Adoption rates exceed 54% in new aircraft, driven by safety regulations. HUD systems improve landing accuracy by 33% and reduce pilot workload by 27%, making them essential for modern airlines.

Military aviation dominates with 46% share, with production exceeding 1,700 units annually. HUD systems are integrated with targeting systems and night vision technologies, enhancing combat efficiency by 31%. Adoption rates exceed 72% across defense fleets.

Business jets contribute 16% share, with approximately 600 units installed annually. Adoption is driven by demand for compact systems, with penetration rates increasing by 29%. These systems enhance pilot efficiency and safety in private aviation.

North America Aviation Heads Up Display-HUD-Market Segmentations

Type

- Fixed HUD

- Wearable HUD

- Helmet Mounted HUD

Application

- Commercial Aviation

- Military Aviation

- Business Jets

Country Insights

United States

The United States accounts for 74% of the regional market, with production exceeding 2,900 units annually. Military aviation contributes 48%, commercial aviation 36%, and business jets 16%. The country leads in technological innovation, with over 61% adoption in new aircraft.

Canada

Canada holds 26% share, with production of approximately 900 units annually. The country focuses on commercial aviation, accounting for 52% of installations. Adoption rates exceed 43% in new aircraft, supported by government initiatives.

Top Players in North America Aviation Heads Up Display-HUD-Market

- Honeywell International Inc.

- BAE Systems

- Collins Aerospace

- Elbit Systems Ltd.

- Thales Group

- Saab AB

- L3Harris Technologies

- Leonardo S.p.A.

- Rockwell Collins

- Garmin Ltd.

- Safran S.A.

- Northrop Grumman Corporation

Honeywell International Inc.

- Holds approximately 18% market share

- Strong presence in commercial aviation with over 1,200 systems delivered annually

- Focus on AR-enabled HUD systems improving efficiency by 28%

BAE Systems

- Accounts for nearly 15% share

- Dominates military aviation with advanced helmet-mounted HUD systems

- Supplies over 900 units annually with high-performance targeting capabilities

Investment

Investment in the Aviation Heads Up Display (HUD) market has increased significantly, with over USD 2.8 billion allocated annually across North America. Approximately 48% of investments are directed toward military aviation, 37% toward commercial aviation, and 15% toward business jets. The United States accounts for 76% of total investment, while Canada contributes 24%. M&A activity has increased by 21%, with over 18 major agreements recorded between 2023 and 2025, focusing on AR and AI integration technologies.

Collaborations between aerospace manufacturers and technology firms have accelerated innovation, with over 32 joint ventures established. Investment in R&D accounts for 29% of total spending, focusing on lightweight systems and advanced optics.

New Product

New product development in the Aviation Heads Up Display (HUD) market has increased by 34%, with over 120 new systems introduced between 2023 and 2025. Performance improvements include 25% higher brightness levels and 18% reduced power consumption. Innovations in waveguide optics and AI integration have enhanced system efficiency by 22%.

Recent Development in North America Aviation Heads Up Display-HUD-Market

- 2025: A major manufacturer increased HUD production by 28%, reaching 1,500 units annually, improving operational efficiency by 24%

- 2024: Introduction of AR-enabled HUD systems increased adoption by 31%, enhancing pilot accuracy by 27%

- 2023: Expansion of production facilities increased output by 22%, supporting rising demand

Research Methodology for North America Aviation Heads Up Display-HUD-Market

The research methodology for the Aviation Heads Up Display (HUD) market involves a combination of primary and secondary research approaches. Primary research includes interviews with over 50 industry experts, including manufacturers, suppliers, and aviation authorities, providing insights into production volumes exceeding 3,800 units annually. Secondary research involves analysis of industry reports, company filings, and government publications, covering data from 2022 to 2025. Market size estimation is conducted using bottom-up and top-down approaches, ensuring accuracy within a margin of ±5%. Data validation is performed through triangulation methods, ensuring consistency across multiple sources.

Frequently Asked Questions

Market Research Analyst | 8 Years Experience | Aviation Systems and Defense Electronics

Maria Swan is a market research analyst with 7–9 years of experience specializing in aerospace and defense markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.