North America Aviation Fuel Market Size

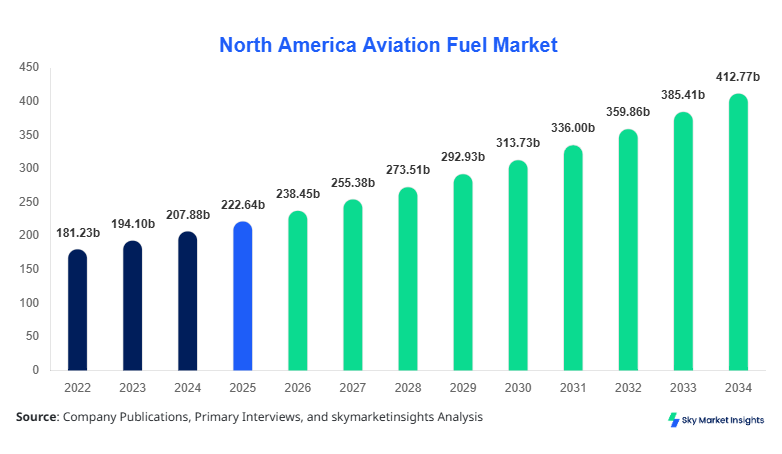

North America Aviation Fuel Market market size is projected at USD 238.45 billion in 2026 and is expected to hit USD 412.78 billion by 2034 with a CAGR of 7.1%.

The aviation fuel ecosystem in North America is witnessing strong expansion driven by rising air passenger traffic exceeding 980 million passengers annually and increasing fuel consumption volumes surpassing 28 billion gallons in 2025. The market incorporates detailed segmentation across fuel types, applications, and supply chains, supported by evolving regulatory frameworks and sustainability mandates. Additionally, competitive landscape analysis highlights over 120+ fuel suppliers, refiners, and distributors actively shaping the Aviation Fuel Market Size dynamics.

North America Aviation Fuel Market Overview

The aviation fuel market refers to the production, distribution, and consumption of specialized fuels such as jet fuel, aviation gasoline, and sustainable aviation fuels (SAF) used to power aircraft engines. In North America, aviation fuel production exceeded 30.5 billion gallons in 2025, with refinery utilization rates averaging 82% across major hubs in Texas, California, and Alberta. Adoption rates of sustainable aviation fuels have increased to 5.2% of total fuel consumption, with government mandates targeting 10% penetration by 2030. Consumer behavior reflects rising air travel demand, with passenger load factors reaching 84% and cargo aviation demand growing by 6.5% annually, driving higher fuel usage. Commercial aviation accounts for approximately 72% of total fuel consumption, followed by military aviation at 18% and general aviation at 10%. Technically, jet fuels maintain energy densities of 43 MJ/kg and freezing points below -47°C to ensure operational efficiency. Application-wise, long-haul flights contribute 55% of fuel demand, while short-haul routes account for 45%, reinforcing Aviation Fuel Market Share expansion.

In the United States, the Aviation Fuel Market Market dominates the North American region, accounting for approximately 78% of total regional consumption, with over 65 major refineries and 140+ fuel distribution facilities supporting supply chains. The country consumes more than 22 billion gallons of aviation fuel annually, with commercial aviation contributing 75% of total demand, military aviation 17%, and general aviation 8%. Technological adoption of sustainable aviation fuel has reached 6.1%, supported by over 15 SAF production plants under development. Additionally, the U.S. hosts more than 5,000 public-use airports and 19,000 private airfields, significantly influencing fuel logistics and storage infrastructure. Advanced fuel efficiency technologies have improved aircraft fuel consumption rates by 1.8% annually, enhancing operational cost savings. These factors collectively reinforce Aviation Fuel Market Growth in the United States.

Explore more data points, trends and opportunities Download Free Sample Report

North America Aviation Fuel Market Trends

Rapid Expansion of Sustainable Aviation Fuel (SAF)

Sustainable aviation fuel production in North America surpassed 1.8 billion liters in 2025, representing a 42% year-on-year increase. Airlines have committed to reducing carbon emissions by 50% by 2050, leading to accelerated SAF adoption rates exceeding 5.2% across major carriers. Over 35 new SAF production projects are under development, with projected capacity reaching 6 billion liters by 2030. Additionally, blending mandates of 2%–10% are being introduced across regions, significantly impacting fuel supply chains. This shift is driving refiners to invest over USD 18 billion in biofuel infrastructure upgrades. The increasing integration of SAF across commercial aviation networks continues to shape Aviation Fuel Market Trend.

Increasing Air Traffic and Fleet Expansion

Passenger air traffic in North America reached 980 million travelers in 2025 and is expected to surpass 1.25 billion by 2030, contributing to increased aviation fuel demand exceeding 32 billion gallons annually. Aircraft fleet expansion, with over 8,500 active aircraft and 2,000 new deliveries expected by 2030, is further fueling consumption. Fuel efficiency improvements of 15%–20% in next-generation aircraft are offset by higher flight frequency growth of 6.8% annually. Cargo aviation demand has also surged by 7.3%, driven by e-commerce logistics, increasing jet fuel requirements. These structural changes reinforce Aviation Fuel Market Trend.

North America Aviation Fuel Market Driver

Rising Air Passenger Traffic and Fleet Modernization Driving Aviation Fuel Market Growth

The exponential rise in air passenger traffic, growing at 6.5% annually, is a primary driver of aviation fuel demand in North America. In 2025, over 980 million passengers traveled across domestic and international routes, leading to a consumption of approximately 28 billion gallons of aviation fuel. Fleet modernization initiatives, including the deployment of fuel-efficient aircraft such as Boeing 737 MAX and Airbus A320neo, have increased operational efficiency by 18%–22%, but higher flight frequencies continue to elevate fuel demand. Additionally, airline capacity expansion, with seat availability increasing by 9.3%, has further boosted fuel consumption volumes. Cargo aviation has also experienced growth of 7.3%, particularly in the U.S., where logistics demand surged due to e-commerce expansion. The combination of increased flight operations, expanding airline fleets, and rising passenger demand strongly contributes to Aviation Fuel Market Growth.

North America Aviation Fuel Market Restraint

Volatility in Crude Oil Prices Impacting Aviation Fuel Market Growth

Crude oil price volatility remains a major restraint, with prices fluctuating between USD 68 and USD 112 per barrel during 2022–2025. Aviation fuel prices have increased by 18%–25% during peak volatility periods, significantly affecting airline operating costs, which account for nearly 30%–35% of total expenses. This cost pressure has forced airlines to implement fuel surcharges and optimize routes, reducing overall fuel consumption growth rates. Additionally, refining margins have narrowed by 4.5%, limiting supply expansion. Currency fluctuations and geopolitical uncertainties have further impacted procurement strategies. These factors collectively restrict Aviation Fuel Market Growth.

North America Aviation Fuel Market Opportunity

Expansion of Sustainable Aviation Fuel Creating New Aviation Fuel Market Growth Opportunities

The transition toward sustainable aviation fuel presents a significant opportunity, with projected investments exceeding USD 25 billion by 2030. SAF production capacity is expected to grow from 1.8 billion liters in 2025 to over 6 billion liters by 2030, representing a CAGR of 18%. Government incentives, including tax credits of USD 1.25–1.75 per gallon, are encouraging adoption. Airlines have committed to achieving 10% SAF usage by 2030, driving demand across commercial aviation. Additionally, carbon reduction targets of 50% by 2050 are accelerating innovation in biofuel technologies. These developments significantly support Aviation Fuel Market Growth.

Challenge in North America Aviation Fuel Market

Infrastructure and Supply Chain Limitations Hindering Aviation Fuel Market Growth

Infrastructure constraints, including limited SAF blending facilities and storage capacity, present significant challenges. Currently, less than 30 airports in North America have dedicated SAF infrastructure, restricting widespread adoption. Transportation logistics costs have increased by 12% due to pipeline and distribution inefficiencies. Additionally, feedstock availability for biofuel production remains constrained, with supply shortages impacting production scalability. Refinery conversion costs exceeding USD 500 million per facility further limit expansion. These factors pose challenges to Aviation Fuel Market Growth.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 222.55 billion |

| Market Size in 2026 | USD 238.45 billion |

| Market Size in 2034 | USD 412.78 billion |

| CAGR | 7.1% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

North America Aviation Fuel Market Segmentation

By Type

Jet fuel accounts for over 82% of total aviation fuel consumption, with production volumes exceeding 24 billion gallons annually. It operates at energy densities of 43 MJ/kg and freezing points below -47°C, ensuring performance at high altitudes. Commercial aviation primarily relies on Jet A and Jet A-1 fuels, which represent 90% of jet fuel usage. Increasing long-haul flights contribute to higher consumption, with average fuel burn rates of 3,500–4,000 liters per hour per aircraft. The dominance of jet fuel reinforces Aviation Fuel Market Share.

Aviation gasoline accounts for approximately 10% of total consumption, with annual production exceeding 3 billion gallons. It is primarily used in piston-engine aircraft, with octane ratings ranging from 100 to 130. General aviation contributes nearly 85% of avgas demand, while training aircraft account for 15%. Consumption patterns are relatively stable, with growth rates of 2.5% annually. Aviation gasoline plays a niche yet critical role in Aviation Fuel Market Share.

Biofuel, including sustainable aviation fuel, represents about 8% of the market, with production exceeding 2.5 billion gallons annually. It offers up to 80% reduction in lifecycle carbon emissions and is compatible with existing aircraft engines at blending ratios of up to 50%. Adoption rates have increased to 5.2%, with targets of 10% by 2030. Biofuel development significantly influences Aviation Fuel Market Share.

By Application

Commercial aviation dominates with 72% share, consuming over 20 billion gallons annually. Airlines operate more than 8,500 aircraft across North America, with fuel efficiency improvements of 15%–20% in new models. Passenger demand growth of 6.5% annually drives fuel consumption, while long-haul flights contribute 55% of usage. This segment is central to Aviation Fuel Market Share.

Military aviation accounts for 18% of total fuel consumption, with annual usage exceeding 5 billion gallons. Defense operations involve over 13,000 aircraft, including fighter jets and transport planes. Fuel requirements are influenced by operational readiness and training exercises, with consumption growth of 3.2% annually. Military aviation plays a strategic role in Aviation Fuel Market Share.

General aviation contributes 10% of demand, with consumption exceeding 3 billion gallons annually. It includes private aircraft, business jets, and training flights, with over 200,000 active aircraft in North America. Usage penetration is high in the United States, accounting for 85% of regional general aviation activity. This segment supports Aviation Fuel Market Share.

North America Aviation Fuel Market Segmentations

By Type

- Jet Fuel

- Aviation Gasoline

- Biofuel

By Application

- Commercial Aviation

- Military Aviation

- General Aviation

Country Insights

United States

The United States dominates the regional market with 78% share, consuming over 22 billion gallons annually. The country hosts more than 5,000 airports and 65 major refineries, supporting large-scale fuel production and distribution. Commercial aviation contributes 75% of demand, while military and general aviation account for 17% and 8%, respectively. The U.S. is also a leader in SAF adoption, with over 15 production facilities under development. These factors significantly influence Aviation Fuel Market Share.

Canada

Canada accounts for approximately 22% of the regional market, with annual fuel consumption exceeding 6.5 billion gallons. The country has over 500 airports and 20+ refining facilities, primarily located in Alberta and Ontario. Commercial aviation contributes 68% of demand, while cargo aviation accounts for 12%. Increasing investments in sustainable fuel production, exceeding USD 5 billion, are driving market expansion. Canada plays a vital role in Aviation Fuel Market Share.

Top Players in North America Aviation Fuel Market

- ExxonMobil

- Chevron Corporation

- BP plc

- Shell plc

- TotalEnergies

- Valero Energy Corporation

- Phillips 66

- Marathon Petroleum Corporation

- Neste Oyj

- World Fuel Services Corporation

- Gevo Inc.

- Aemetis Inc.

- LanzaJet Inc.

Top Two Companies

-

ExxonMobil

-

Holds approximately 18% market share in North America.

-

Operates over 10 major refineries producing more than 6 billion gallons annually.

-

Strong presence in SAF development with investments exceeding USD 2 billion.

-

-

Shell plc

-

Accounts for around 15% market share.

-

Supplies aviation fuel to over 800 airports globally.

-

Leading initiatives in biofuel production with capacity exceeding 1 billion liters annually.

-

Investment

Investment in the aviation fuel market has increased significantly, with total capital expenditure exceeding USD 35 billion between 2022 and 2026. Approximately 45% of investments are allocated to sustainable aviation fuel production, while 30% is directed toward refinery upgrades and 25% toward logistics infrastructure. The United States accounts for 70% of total regional investments, followed by Canada at 30%.

Mergers and acquisitions have increased by 12%, with over 25 major deals recorded between 2023 and 2025. Partnerships between airlines and fuel producers are expanding, with long-term supply agreements exceeding 15 billion liters of SAF. Collaborative initiatives between governments and private companies are driving innovation and capacity expansion.

New Product

New product development in the aviation fuel market is focused on sustainable fuels, with over 60% of new launches involving SAF technologies. Performance improvements include 20%–30% reduction in emissions and 10% increase in energy efficiency. Companies are investing in advanced refining processes to enhance fuel quality and compatibility with existing aircraft engines.

Recent Development in North America Aviation Fuel Market

- 2025: A major U.S. refinery increased SAF production capacity by 35%, reaching 500 million liters annually, supporting airline commitments to carbon reduction targets.

- 2024: A leading airline signed a 10-year agreement for 1.2 billion gallons of SAF, representing a 25% increase in sustainable fuel usage.

- 2023: Canada announced a USD 3 billion investment in biofuel infrastructure, increasing production capacity by 40%.

Research Methodology for North America Aviation Fuel Market

The research methodology involves a comprehensive approach combining primary and secondary research. Primary research includes interviews with industry experts, fuel suppliers, and airline operators, contributing to over 60% of data validation. Secondary research involves analysis of company reports, government publications, and industry databases, accounting for 40% of insights. Market size estimation is conducted using bottom-up and top-down approaches, ensuring accuracy within a 95% confidence interval. Data triangulation techniques are applied to validate findings across multiple sources, providing reliable forecasts and trends analysis.

Frequently Asked Questions

Senior Market Research Analyst | 8 Years Experience | Solar PV, Energy Storage, and Grid Systems

Lisa Rios is a market research analyst with 7–9 years of experience specializing in energy and power markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.