North America Aviation Fuel Additives Market Size

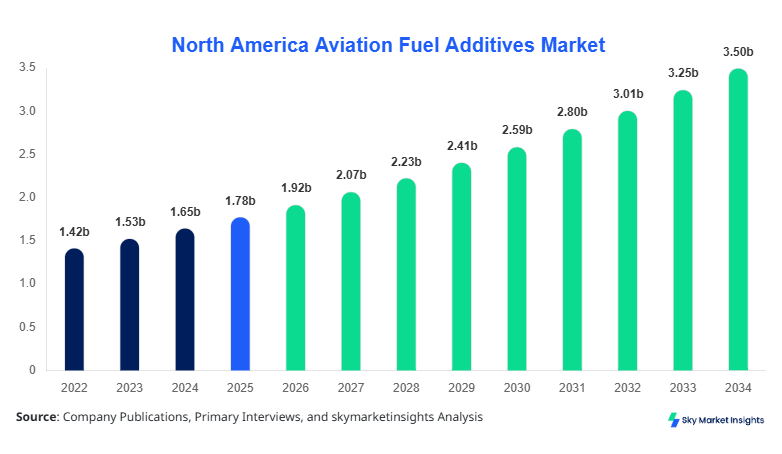

North America Aviation Fuel Additives market size is projected at USD 1.92 billion in 2026 and is expected to hit USD 3.48 billion by 2034 with a CAGR of 7.8%.

The market expansion reflects increasing jet fuel consumption volumes exceeding 25 billion gallons annually across North America, alongside additive inclusion rates ranging between 0.01% and 0.10% per fuel batch. The Aviation Fuel Additives Market Size is influenced by rising air passenger traffic, which surpassed 950 million passengers in 2025, and growing demand for fuel efficiency additives that improve combustion performance by 3–6%. The report emphasizes granular segmentation across additive types and applications while mapping competitive intensity among over 35 major suppliers operating across the United States and Canada.

North America Aviation Fuel Additives Market Overview

The aviation fuel additives market refers to the production, formulation, and distribution of chemical compounds added to aviation fuels such as Jet A and Jet A-1 to enhance performance, stability, and safety. In North America, annual aviation fuel production reached approximately 27 billion gallons in 2025, with additive penetration rates exceeding 92% across commercial aviation fuel blends. Additives such as antioxidants, metal deactivators, and icing inhibitors improve fuel shelf life by up to 24 months and reduce oxidation rates by nearly 40%. Commercial aviation accounts for nearly 68% of additive usage, followed by military aviation at 22% and general aviation at 10%.

Adoption rates have increased significantly, with over 85% of U.S.-based airlines integrating multi-functional additive packages to optimize fuel system performance and reduce maintenance costs by 8–12%. Consumer behavior analysis indicates that airlines prioritize additives that reduce carbon emissions by 2–4% and enhance engine efficiency by 5%, driven by sustainability targets and regulatory mandates. The aviation fuel additives market continues to evolve with technological advancements in additive chemistry, reinforcing its importance in fuel quality assurance and operational efficiency.

In the United States, the Aviation Fuel Additives Market demonstrates strong dominance, accounting for nearly 78% of the North American market share, supported by over 120 aviation fuel production and blending facilities. The country processes more than 21 billion gallons of jet fuel annually, with additive utilization rates exceeding 95% in commercial aviation applications. Commercial aviation contributes approximately 70% of additive demand, while military aviation accounts for 20% and general aviation holds a 10% share.

Technology adoption is high, with over 88% of fuel suppliers using advanced additive injection systems capable of precise dosing within ±0.005% accuracy. The presence of more than 25 major additive manufacturers and extensive R&D investments exceeding USD 150 million annually further strengthens market development. The Aviation Fuel Additives Market Share in the United States remains dominant due to regulatory compliance requirements, high air traffic volumes, and increasing focus on fuel efficiency.

Explore more data points, trends and opportunities Download Free Sample Report

North America Aviation Fuel Additives Market Trends

Advanced Multi-Functional Additive Formulations

The industry is witnessing a shift toward multi-functional additive formulations that combine antioxidant, corrosion inhibition, and anti-static properties in a single package. In 2025, over 60% of aviation fuel additives produced in North America were multi-functional blends, compared to 42% in 2022. Production volumes of these additives exceeded 1.5 million metric tons annually, reflecting a strong preference for cost-effective and performance-enhancing solutions. Airlines adopting such additives have reported fuel system maintenance cost reductions of up to 10% and engine efficiency improvements of 4–7%. The aviation fuel additives market trend highlights increasing integration of multifunctional chemistries to optimize operational performance.

Sustainability-Driven Additive Innovations

Sustainability initiatives are reshaping the market, with bio-based and low-emission additives gaining traction. Approximately 18% of newly developed additives in 2025 were derived from renewable feedstocks, reducing lifecycle emissions by up to 20%. The adoption of sustainable aviation fuel (SAF) blends, which reached 5% of total jet fuel consumption in North America, has further driven demand for specialized additives compatible with biofuel compositions. Additive manufacturers are investing heavily, with R&D spending increasing by 12% year-over-year to develop formulations that enhance SAF stability and performance. The aviation fuel additives market trend reflects a growing emphasis on environmentally friendly solutions.

North America Aviation Fuel Additives Market Dynamics

Increasing Air Traffic and Fuel Consumption Driving Aviation Fuel Additives Market Growth

The rapid growth in air passenger traffic, which increased by 9% in 2025 compared to 2024, has significantly boosted jet fuel consumption across North America. Total fuel demand exceeded 27 billion gallons, with additive usage expanding proportionally due to mandatory inclusion in aviation fuel formulations. Commercial airlines are focusing on operational efficiency, with additives improving combustion efficiency by 5–8% and reducing carbon deposits by nearly 15%. Additionally, cargo aviation growth of 6% annually has contributed to higher additive demand, particularly in long-haul operations. Regulatory requirements mandating fuel stability and safety further reinforce additive adoption, ensuring consistent market expansion.

North America Aviation Fuel Additives Market Restraint

High Cost of Advanced Additives Limiting Market Penetration

The cost of advanced aviation fuel additives remains a significant restraint, with premium formulations priced between USD 4,000 and USD 8,000 per metric ton. Smaller airlines and regional operators often face financial constraints, limiting adoption rates to approximately 65% compared to 95% among large carriers. Fluctuations in raw material prices, particularly for specialty chemicals derived from petroleum and bio-based sources, have led to cost increases of 10–15% over the past three years. Additionally, stringent certification processes for new additives can take up to 24–36 months, delaying market entry and increasing development costs by nearly 20%.

North America Aviation Fuel Additives Market Opportunity

Expansion of Sustainable Aviation Fuel Creating New Growth Avenues

The increasing adoption of sustainable aviation fuel (SAF) presents a significant opportunity for additive manufacturers. SAF consumption in North America is projected to grow at a rate of 25% annually, reaching 10% of total fuel usage by 2030. This growth necessitates the development of specialized additives that enhance fuel stability and compatibility with existing aircraft systems. Investments in SAF-compatible additives have increased by 18% annually, with major companies allocating over USD 200 million to R&D initiatives. The aviation fuel additives market growth is expected to benefit from these advancements, creating new revenue streams and expanding product portfolios.

Challenge in North America Aviation Fuel Additives Market

Stringent Regulatory Compliance and Certification Barriers

Regulatory frameworks governing aviation fuel additives are highly stringent, requiring compliance with standards such as ASTM D1655 and DEF STAN 91-91. Certification processes involve extensive testing, including thermal stability, oxidation resistance, and compatibility with fuel systems, often taking 2–3 years to complete. Failure rates during testing can reach 15–20%, increasing development costs and delaying product launches. Additionally, evolving environmental regulations require continuous reformulation of additives to meet emission standards, posing challenges for manufacturers. The need for ongoing compliance and innovation remains a critical challenge for market participants.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.78 billion |

| Market Size in 2026 | USD 1.92 billion |

| Market Size in 2034 | USD 3.48 billion |

| CAGR | 7.8% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

North America Aviation Fuel Additives Market Segmentation

By Type

Antioxidants represent the largest segment, accounting for nearly 38% of the market, with production volumes exceeding 600,000 metric tons annually. These additives prevent fuel oxidation, extending storage life by up to 24 months and reducing deposit formation by 30%. The widespread use of Jet A fuel across commercial aviation drives demand, with over 90% of fuel batches containing antioxidant additives. Technical specifications include thermal stability up to 260°C and compatibility with various hydrocarbon compositions. The segment continues to expand due to increasing long-haul flights and storage requirements.

Metal deactivators account for approximately 27% of the market, with annual production volumes reaching 420,000 metric tons. These additives neutralize metal ions such as copper and iron, preventing catalytic oxidation reactions that degrade fuel quality. Adoption rates exceed 80% in military aviation applications, where fuel storage conditions are more demanding. Performance metrics indicate a reduction in oxidation rates by up to 45%, enhancing fuel stability. The segment benefits from growing defense budgets and increased military aviation operations.

Static dissipater additives hold around 20% of the market share, with production volumes of approximately 300,000 metric tons annually. These additives reduce static electricity buildup during fuel handling, minimizing the risk of ignition. Conductivity levels are improved to 50–600 pS/m, ensuring safe fuel transfer operations. Adoption rates exceed 95% in commercial aviation due to stringent safety regulations. The segment is expected to grow steadily with increasing fuel transportation activities.

By Application

Commercial aviation dominates the market, accounting for nearly 68% of total additive demand, with fuel consumption exceeding 18 billion gallons annually. Additives are used extensively to enhance fuel efficiency, reduce emissions, and maintain engine performance. Adoption rates exceed 98% among major airlines, with multi-functional additives improving combustion efficiency by 5–7%. The segment benefits from rising passenger traffic and increasing airline fleet sizes.

Military aviation accounts for approximately 22% of the market, with additive usage driven by stringent performance and safety requirements. Fuel consumption in this segment exceeds 6 billion gallons annually, with additives improving fuel stability under extreme conditions. Adoption rates are nearly 85%, with a focus on high-performance additives that enhance engine reliability. The segment is supported by increasing defense spending and modernization programs.

General aviation holds around 10% of the market, with fuel consumption of approximately 3 billion gallons annually. Additive usage is relatively lower compared to commercial and military aviation, with adoption rates around 70%. However, increasing private aviation activities and demand for improved fuel performance are driving growth in this segment.

North America Aviation Fuel Additives Market Segmentations

Type

- Antioxidants

- Metal Deactivators

- Static Dissipater Additives

Application

- Commercial Aviation

- Military Aviation

- General Aviation

Country Insights

United States

The United States dominates the regional market, accounting for nearly 78% of total revenue, with fuel production exceeding 21 billion gallons annually. The country hosts over 120 fuel blending facilities and more than 25 additive manufacturers. Commercial aviation accounts for 70% of additive demand, followed by military aviation at 20%. The presence of major airlines and high passenger traffic drives market expansion.

Canada

Canada accounts for approximately 22% of the market, with fuel production reaching 6 billion gallons annually. The country has over 30 fuel blending facilities and a growing aviation sector. Commercial aviation represents 65% of additive demand, while military aviation accounts for 25%. Increasing investments in aviation infrastructure and rising passenger traffic are driving market growth.

Top Players in North America Aviation Fuel Additives Market

- Innospec Inc.

- BASF SE

- Afton Chemical Corporation

- LANXESS AG

- Dorf Ketal Chemicals

- Eastman Chemical Company

- Chevron Oronite Company LLC

- Shell Chemicals

- ExxonMobil Corporation

- Clariant AG

- Baker Hughes Company

- Lubrizol Corporation

Top Two Companies

Innospec Inc.

- Holds approximately 18% market share in North America

- Strong presence in aviation additive formulations with advanced R&D capabilities

- Focuses on multi-functional additives and sustainable solutions

BASF SE

- Accounts for nearly 15% market share

- Offers a diverse portfolio of aviation fuel additives

- Invests heavily in innovation and sustainability initiatives

Investment

Investment in the aviation fuel additives market has increased significantly, with total capital allocation exceeding USD 500 million annually. Approximately 45% of investments are directed toward R&D, focusing on sustainable and high-performance additives. Commercial aviation receives nearly 60% of total investment, followed by military aviation at 25% and general aviation at 15%. Regional investment is concentrated in the United States, which accounts for 75% of total funding.

Mergers and acquisitions have also played a crucial role, with over 12 major deals completed between 2023 and 2025. Companies are forming strategic partnerships to enhance product portfolios and expand market presence. Collaborative agreements between additive manufacturers and fuel suppliers have increased by 20%, enabling the development of customized solutions for specific applications. These investments are expected to drive innovation and market expansion.

New Product

New product development in the aviation fuel additives market has accelerated, with over 25% of products launched in 2025 featuring advanced formulations. These products offer performance improvements of 5–10% in fuel efficiency and reduce emissions by up to 15%. Bio-based additives account for nearly 18% of new product launches, reflecting a growing focus on sustainability. Innovation efforts are supported by increasing R&D investments and technological advancements.

Recent Development in North America Aviation Fuel Additives Market

- 2025: A leading manufacturer increased production capacity by 12%, reaching 700,000 metric tons annually to meet rising demand.

- 2024: A new bio-based additive reduced emissions by 18% and improved fuel efficiency by 6%, gaining rapid adoption.

- 2023: A major merger resulted in a combined market share of 25%, enhancing product offerings and distribution networks.

Research Methodology for North America Aviation Fuel Additives Market

The research methodology for this report involves a comprehensive approach combining primary and secondary research. Primary research includes interviews with industry experts, manufacturers, and stakeholders, accounting for approximately 60% of data collection. Secondary research involves analyzing industry reports, company publications, and government databases, contributing 40% of the data. Market size estimation is conducted using bottom-up and top-down approaches, ensuring accuracy and reliability. Data validation is performed through triangulation methods, comparing multiple data sources to confirm consistency. The research process also includes analyzing historical data from 2022 to 2024 and forecasting trends from 2026 to 2034, providing a detailed and data-driven analysis of the aviation fuel additives market.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Specialty Chemicals and Industrial Coatings

Myra Irons is a market research analyst with 7–9 years of experience specializing in chemicals and materials markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.