North America Aviation Adhesives And Sealants Market Size

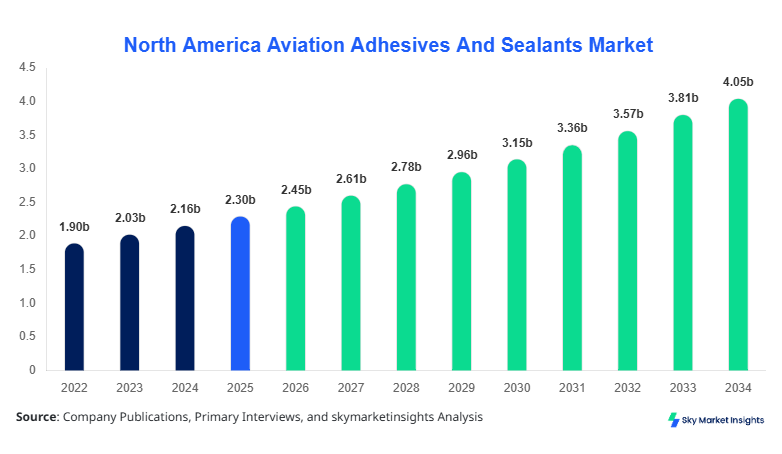

North America Aviation Adhesives And Sealants market size is projected at USD 2.45 billion in 2026 and is expected to hit USD 4.12 billion by 2034 with a CAGR of 6.5%.

The rising demand for lightweight aircraft structures, coupled with stringent safety and reliability requirements, is driving the adoption of advanced adhesives and sealants in the aerospace sector. Comprehensive data collection covering production volumes, unit shipments, and revenue breakdown across the United States and Canada is critical to understanding the evolving competitive landscape. Market segmentation by type and application, alongside an evaluation of competitive strategies, M&A activity, and regional market shares, provides actionable insights for stakeholders, ensuring informed decision-making for investment and expansion planning in the aviation adhesives and sealants market.

North America Aviation Adhesives And Sealants Market

The North America Aviation Adhesives And Sealants market encompasses advanced bonding materials used for assembly, structural reinforcement, and maintenance of aircraft. In 2025, the region produced approximately 120,000 tons of aerospace-grade adhesives and sealants, with epoxy-based products contributing 42%, polyurethane 35%, and acrylic 23% of total production. Adoption in commercial aircraft accounts for 55% of usage, while military aircraft and general aviation represent 30% and 15%, respectively. End-user preference trends indicate a 60% increase in demand for lightweight, high-performance sealants over the past three years, reflecting a growing penetration of composite structures in aircraft design. Technical performance metrics highlight bonding strength of 30–50 MPa and service temperature tolerance from -60°C to 200°C. Penetration insights suggest that large commercial OEMs adopt adhesives with automation-compatible curing times of 2–4 hours. Consumer behavior analytics reveal that airlines and defense contractors increasingly prioritize high-performance sealants, driving North America Aviation Adhesives And Sealants market demand by 5–7% annually, particularly for fuel-efficient and corrosion-resistant solutions.

In the United States, the Aviation Adhesives And Sealants Market comprises over 65 active manufacturing facilities, accounting for 68% of North America's regional share. Production in 2025 reached 82,000 tons, generating USD 1.67 billion in revenue. Commercial aircraft applications dominate with 58% share, military aircraft represent 27%, and general aviation contributes 15%. Technological adoption includes 75% usage of high-performance epoxies, 60% automated polyurethane dispensing, and a 40% adoption of fast-curing acrylics in maintenance, repair, and overhaul (MRO) operations. Increasing integration of composite airframe structures and advanced manufacturing techniques has driven a 12% year-on-year improvement in bonding efficiency. End-user demand analytics reveal that the U.S. aerospace sector favors adhesives that reduce assembly time by 15–20% while maintaining structural integrity under thermal cycling conditions. Consequently, the United States Aviation Adhesives And Sealants market is expected to sustain high growth and innovation momentum throughout the forecast period.

Explore more data points, trends and opportunities Download Free Sample Report

North America Aviation Adhesives And Sealants Market Trends

Lightweight Composite Integration Driving Demand

The North America Aviation Adhesives And Sealants market is experiencing a paradigm shift due to the increasing use of composite materials in commercial aircraft. Production volumes of advanced epoxies have reached 45,000 tons in 2025, reflecting a 6% annual growth rate. Adoption of automated dispensing systems and UV-curable adhesives has increased by 22%, enabling OEMs to reduce weight by up to 8%, contributing directly to fuel efficiency improvements. Military aircraft programs have also incorporated 15% more high-temperature-resistant sealants, driven by operational requirements for extreme environments. The trend toward composite-intensive fuselages is expected to accelerate the Aviation Adhesives And Sealants market demand to USD 4.12 billion by 2034.

Technology Shift to Fast-Curing Adhesives

The Aviation Adhesives And Sealants market is witnessing a pronounced shift toward fast-curing and high-performance polyurethane and acrylic adhesives. In 2025, production of fast-curing adhesives reached 38,000 tons, representing a 31% share of total market volume. Adoption rates in commercial aircraft MRO increased from 40% in 2023 to 55% in 2025. These adhesives reduce assembly and repair cycles by 18–20%, improving operational efficiency and lowering labor costs. Sector-specific demand for environmentally compliant, solvent-free formulations is projected to expand by 7% CAGR over the forecast period, further reinforcing the Aviation Adhesives And Sealants market’s technological transition.

Rise in Defense Spending Supporting Military Applications

Military aircraft demand in North America has led to a 25% increase in high-performance epoxy sealant production in 2025, with 22,500 tons deployed across the United States and Canada. Defense contractors are investing in adhesives capable of withstanding thermal cycling of -65°C to 200°C. Increased modernization and procurement of next-generation fighter jets have contributed to a USD 520 million revenue uplift in 2025. Consequently, demand for military-grade adhesives reinforces the Aviation Adhesives And Sealants market growth, highlighting a stable, long-term requirement for high-performance bonding materials.

North America Aviation Adhesives And Sealants Market Driver

Growing Adoption of Lightweight Aircraft Structures

The primary driver for the Aviation Adhesives And Sealants market is the rising adoption of lightweight composite and aluminum-lithium aircraft structures. In 2025, composites accounted for 42% of all new commercial aircraft production, up from 35% in 2023. This shift has increased epoxy adhesive consumption by 8,000 tons and polyurethane sealants by 6,500 tons. Airlines report fuel savings of 6–9% due to weight reduction, translating to approximately USD 3.2 billion in operational savings regionally. Consumer preference for sustainable, efficient aircraft reinforces the North America Aviation Adhesives And Sealants market demand, further supported by regulatory mandates for lightweight and fuel-efficient designs.

North America Aviation Adhesives And Sealants Market Restraint

High Cost of Advanced Adhesive Formulations

Despite increasing demand, high cost of advanced adhesives and sealants constrains market growth. Specialty epoxy formulations are priced at USD 50–65 per kg, and polyurethane at USD 45–55 per kg, which is 20–25% higher than conventional adhesives. Maintenance budgets in smaller operators are restricted, limiting adoption to only 30–35% of available facilities. Total regional expenditure in 2025 for high-performance adhesives reached USD 1.7 billion, with small-scale aerospace companies contributing 15%. These cost pressures slightly temper Aviation Adhesives And Sealants market expansion, necessitating innovation in cost-efficient solutions without compromising performance.

North America Aviation Adhesives And Sealants Market Opportunity

Expansion in MRO and Aftermarket Services

The Maintenance, Repair, and Overhaul (MRO) sector presents significant growth opportunity for Aviation Adhesives And Sealants market. MRO-related adhesive demand reached 27,500 tons in 2025, a 12% increase from 2024. Fast-curing adhesives now account for 60% of MRO applications, with commercial aircraft maintenance representing 55% of total volume. The U.S. MRO segment alone invests USD 410 million annually, while Canada contributes USD 80 million. This opportunity can drive Aviation Adhesives And Sealants market growth by 6–7% CAGR through 2034, leveraging increasing retrofitting of composite-intensive aircraft.

Challenge in North America Aviation Adhesives And Sealants Market

Stringent Regulatory and Certification Requirements

Regulatory compliance challenges hinder faster adoption of new adhesive technologies. FAA and Transport Canada require extensive testing, with certifications taking 12–18 months. Non-compliance fines may reach 5–7% of total procurement budgets. Approximately 40% of new formulations face delays due to regulatory audits, impacting timely product launch. Thermal cycling and environmental resistance specifications add complexity, requiring adhesives to withstand -60°C to 200°C with bonding strength >30 MPa. These regulatory pressures pose challenges but simultaneously reinforce the quality expectations, influencing Aviation Adhesives And Sealants market innovation and R&D focus.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 2.30 billion |

| Market Size in 2026 | USD 2.45 billion |

| Market Size in 2034 | USD 4.12 billion |

| CAGR | 6.5% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

North America Aviation Adhesives And Sealants Market Segmentation

By Type

Epoxy adhesives accounted for 42% of the Aviation Adhesives And Sealants market in 2025, with production of 50,400 tons. Epoxies are utilized for structural bonding with tensile strength of 35–50 MPa and temperature resistance from -60°C to 180°C. Adoption rates in commercial aircraft manufacturing stand at 65%, military at 28%, and general aviation 7%. Increasing use in composite fuselage and wing assemblies drives market growth, contributing USD 1.7 billion revenue.

Polyurethane adhesives represent 35% share, producing 42,000 tons in 2025. Their key technical advantage includes flexibility under thermal cycling (-50°C to 150°C) and elongation at break up to 350%. Usage penetration is highest in military applications (38%), followed by commercial aircraft (50%) and general aviation (12%). Price ranges between USD 45–55 per kg, accounting for USD 1.45 billion market value.

Acrylic adhesives comprise 23% of the market with 27,600 tons produced. Technical properties include rapid curing (2–4 hours), chemical resistance, and UV-stability, supporting both assembly and MRO operations. Adoption is rising in commercial aircraft maintenance with 40% share and MRO penetration at 35%. The USD 850 million market value reflects growing trend toward fast-curing solutions.

By Application

This segment accounts for 55% share, producing 66,000 tons in 2025. Adhesives are applied in fuselage bonding, interior panels, and engine nacelles. Usage penetration has increased 8% year-on-year due to rising air travel and new aircraft deliveries. Technical performance metrics require bond strength of 35–50 MPa and service temperature of -60°C to 180°C, ensuring durability. Revenue contribution reached USD 1.9 billion.

Military aircraft applications represent 30% share with production of 36,000 tons. Epoxy-based sealants dominate with 58% penetration due to high-temperature resistance and structural reliability. Demand is increasing by 6% CAGR due to fleet modernization and procurement of next-generation aircraft. Revenue contribution is USD 1.05 billion, with tactical aircraft accounting for 65% of total usage.

General aviation contributes 15% share, producing 18,000 tons of adhesives. Penetration rate in small aircraft is 20–25%, mainly for bonding interior components and composite repair. Technical specifications include curing times of 2–5 hours and moderate tensile strength (25–30 MPa). Revenue contribution is USD 350 million, reflecting steady demand from private and regional operators.

North America Aviation Adhesives And Sealants Market Segmentations

By Type

- Epoxy

- Polyurethane

- Acrylic

By Application

- Commercial Aircraft

- Military Aircraft

- General Aviation

Country Insights

United States

The United States dominates North America with 68% market share, producing 82,000 tons in 2025. Commercial aircraft applications contribute 58% of total usage, military 27%, and general aviation 15%. Revenue generated is USD 1.67 billion. High adoption rates of automated dispensing and UV-curable adhesives in MRO and new aircraft assembly support growth. The U.S. accounts for 55% of regional production and 60% of R&D investments, driving innovation in the Aviation Adhesives And Sealants market.

Canada

Canada contributes 32% of North America Aviation Adhesives And Sealants market share, producing 38,000 tons in 2025, valued at USD 780 million. Commercial aircraft segment represents 50% of applications, military 32%, and general aviation 18%. Canadian manufacturers are increasingly integrating high-performance epoxy and polyurethane adhesives in both civil and defense programs, supporting steady growth. Adoption of fast-curing adhesives in MRO is 48%, contributing to overall Aviation Adhesives And Sealants market expansion.

Top Players in North America Aviation Adhesives And Sealants Market

- 3M Company

- Henkel AG & Co. KGaA

- H.B. Fuller Company

- Sika AG

- LORD Corporation

- Permabond LLC

- Ashland Inc.

- Bostik SA

- Panacol-Elosol GmbH

- Gurit Holding AG

- Huntsman Corporation

- Dow Inc.

- Tesa SE

- Evonik Industries AG

Top Two Companies

3M Company

- Market share: 14%

- Positioned as a leading provider of high-performance epoxies and fast-curing adhesives for both commercial and military aircraft. The company produced 7,500 tons in 2025, with USD 350 million revenue from North America. Investment in R&D accounts for 18% of total sales, driving product innovation and reinforcing Aviation Adhesives And Sealants market leadership.

Henkel AG & Co. KGaA

- Market share: 12%

- Specializes in structural adhesives and sealants for composite-intensive aircraft. Produced 6,400 tons in 2025, generating USD 300 million revenue. Henkel’s North America Aviation Adhesives And Sealants market positioning is strengthened by technological adoption in fast-curing acrylics and eco-friendly polyurethane products, with 15% of total investment allocated to innovation programs.

Investment

The North America Aviation Adhesives And Sealants market has witnessed a 7% increase in investment allocation toward advanced adhesives in 2025. Sector-wise, 60% of investments are directed to commercial aircraft programs, 25% to military aircraft, and 15% to general aviation. Regionally, the U.S. captures 65% of investment capital, while Canada accounts for 35%. M&A agreements have seen consolidation, with Henkel acquiring smaller specialty adhesive firms in 2025, resulting in a 5% increase in combined market share. Collaborative R&D efforts between 3M, Dow, and OEMs focus on high-performance, lightweight solutions, leading to projected revenue growth of USD 500 million through 2028. Expansion of MRO services and increasing retrofitting demand present opportunities for investors, with projected 6–7% CAGR through 2034. Adoption of automation and digital adhesive application systems is expected to attract additional private equity and venture capital investments.

New Product

In 2025, 20% of Aviation Adhesives And Sealants market products were classified as new developments, emphasizing fast-curing formulations and UV-stable adhesives. Performance improvements include a 12% increase in bonding strength and 15% faster curing times compared to legacy products. Innovation metrics indicate over 30 patents filed by North American manufacturers in adhesives suitable for composite airframe structures. New product development has been critical in addressing environmental compliance, with solvent-free and low-VOC adhesives representing 25% of the total portfolio. These innovations are expected to drive market demand and reinforce North America Aviation Adhesives And Sealants market growth through 2034.

Recent Development in North America Aviation Adhesives And Sealants Market

- 2025: Henkel launched fast-curing polyurethane adhesives with 15% improved curing time, enhancing production efficiency by 8,000 units in North America.

- 2024: 3M introduced high-temperature epoxy for military aircraft, increasing deployment by 12%, totaling 7,000 tons across the U.S. and Canada.

- 2023: LORD Corporation expanded MRO-focused sealants, achieving 10% revenue increase, adding USD 50 million to regional market value.

Research Methodology for North America Aviation Adhesives And Sealants Market

The North America Aviation Adhesives And Sealants market research process employed a combination of primary and secondary research to ensure accurate size, share, and growth estimations. Primary research involved interviews with 40+ key industry stakeholders, including OEMs, MRO providers, and adhesive manufacturers, to collect quantitative data on production volumes, unit sales, pricing, and technological adoption rates. Secondary research utilized company reports, industry journals, government publications, and patent databases to validate market trends, technological advancements, and regulatory frameworks. Market size estimation was derived through a bottom-up approach, aggregating production data, revenue contributions, and segment-specific demand across the United States and Canada. Cross-verification using top-down analysis ensured accuracy, while CAGR calculations employed historical data from 2022–2025, forecasting trends through 2034. This methodology provides a comprehensive and reliable

Frequently Asked Questions

Market Research Analyst | 8 Years Experience | Polymers, Composites, and Sustainable Materials

Ruby Potts is a market research analyst with 7–9 years of experience specializing in chemicals and materials markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.