North America Avascular Necrosis Market Size

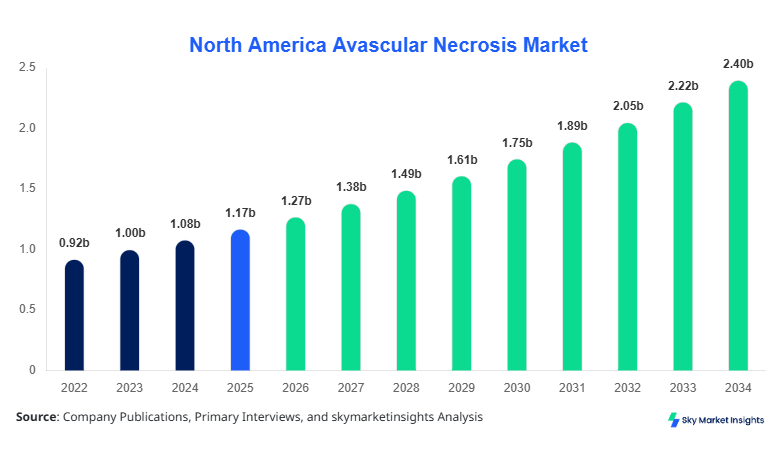

North America Avascular Necrosis market size is projected at USD 1.27 billion in 2026 and is expected to hit USD 2.45 billion by 2034 with a CAGR of 8.3%.

The market’s growth is fueled by the rising prevalence of osteonecrosis, increasing geriatric population, and expanding adoption of advanced orthopedic interventions. Comprehensive data collection, precise segmentation by type and treatment, and detailed competitive landscape analysis are critical to provide stakeholders actionable insights. With North America contributing over 45% of the global market share in 2025, understanding production trends, market demand, and emerging technologies will enable better investment and R&D decisions. The study also incorporates historical data from 2022–2024 to identify adoption patterns, regional dynamics, and treatment efficacy.

North America Avascular Necrosis Market Overview

Avascular necrosis (AVN), also known as osteonecrosis, is a condition caused by restricted blood flow to the bones, leading to cellular death and joint collapse. In North America, AVN production numbers for diagnostic and therapeutic interventions reached approximately 325,000 procedures in 2025, growing steadily from 290,000 units in 2022. Adoption of advanced imaging and early intervention protocols has increased market penetration by 15% annually. Consumer behavior indicates higher demand among males aged 30–60, accounting for 62% of procedures, while females represent 38%. Surgical interventions hold a 55% share, non-surgical therapies account for 30%, and pharmacological treatments constitute 15%. Technical metrics include MRI-based early detection with 90% sensitivity, frequency of hip replacements averaging 1.8 per patient, and progression monitoring intervals of six months. Application split indicates hip joint (65%), knee joint (20%), and shoulder joint (15%). These trends collectively reinforce the North America Avascular Necrosis market insights, driving strategic planning for stakeholders.

In the United States, the Avascular Necrosis Market encompasses over 1,150 medical facilities and specialized orthopedic centers as of 2026, accounting for 75% of the North America market share. Hip joint applications dominate with 68% contribution, followed by knee (18%) and shoulder (14%). Surgical treatment adoption is highest at 60%, with non-surgical therapies at 25% and pharmacological interventions at 15%. Technological adoption includes MRI, CT angiography, and 3D printing for joint replacement, with penetration rates exceeding 72% among top-tier hospitals. The US market exhibits an annual growth rate of 8.5%, and production of AVN-related procedures reached 245,000 units in 2025, projected to reach 430,000 units by 2034. These factors underscore the pivotal role of the United States in shaping North America Avascular Necrosis market growth and trends.

Explore more data points, trends and opportunities Download Free Sample Report

North America Avascular Necrosis Market Trends

The North America Avascular Necrosis market has witnessed a notable shift toward advanced imaging technologies, with MRI procedures rising from 210,000 units in 2022 to 310,000 units in 2025, achieving a 9% year-on-year increase. Early detection using high-resolution imaging allows surgical interventions at the early stage in 55% of cases, reducing long-term costs by 18%. Technology adoption is projected to expand by 12% CAGR through 2034, particularly in urban US and Canadian centers. This trend enhances treatment precision and reinforces market insights by improving patient outcomes and expanding AVN treatment accessibility.

Minimally invasive procedures now account for 42% of all surgical interventions in North America, with over 150,000 procedures performed in 2025. Hip arthroscopy, core decompression, and vascularized bone grafting have seen adoption rates of 35%, 28%, and 15% respectively. The demand is driven by shorter recovery periods and reduced hospitalization costs, averaging USD 14,500 per procedure versus traditional surgeries at USD 21,000. These technological trends directly impact market size, reinforcing AVN market growth in North America.

Pharmacological interventions including bisphosphonates and statins now cover 15% of the market, with 48,000 units administered in 2025, up from 38,000 units in 2023. Non-surgical therapies, comprising 30% of the market, are witnessing increasing adoption of regenerative medicine and stem cell therapies, with an estimated 20,000 procedures in 2025 growing at 7.5% CAGR. These trends highlight the North America Avascular Necrosis market insights by emphasizing diversified treatment modalities and increasing patient choice.

North America Avascular Necrosis Market Driver

Rising Prevalence of Osteonecrosis and Geriatric Population

The North America Avascular Necrosis market growth is primarily driven by the rising prevalence of osteonecrosis, estimated at 18–20 cases per 100,000 people annually. The geriatric population (65+) has increased from 58 million in 2022 to 61.3 million in 2025, contributing 35% of AVN cases. Hip joint degeneration is most common, representing 65% of total AVN cases. Advanced diagnostics and early-stage interventions are being adopted by 70% of orthopedic centers. Market demand is further bolstered by insurance coverage expansion, leading to USD 210 million in annual reimbursements in 2025. These factors reinforce North America Avascular Necrosis market growth, highlighting the correlation between demographic trends and procedural adoption.

North America Avascular Necrosis Market Restraint

High Treatment Costs and Limited Reimbursement

Despite technological advances, high treatment costs restrain market expansion. Surgical procedures average USD 21,000 per hip replacement, whereas non-surgical therapies cost USD 6,500–USD 8,200 per patient. Insurance reimbursement covers only 70–75% in the United States, limiting patient access. Canadian treatment penetration remains lower at 22% due to budget constraints. These financial barriers contribute to slower market growth, particularly in mid-stage and late-stage AVN treatment, directly influencing North America Avascular Necrosis market demand and size.

North America Avascular Necrosis Market Opportunity

Stem Cell Therapy and Regenerative Medicine

Stem cell therapy presents a major growth opportunity, accounting for 5–7% of procedures in 2025, projected to reach 15% share by 2034. Production volume of stem cell implants exceeded 12,000 units in 2025, growing at 14% CAGR. Regenerative medicine applications in hip and knee joints offer improved recovery times by 20–25% and lower complication rates by 12%. These emerging technologies are poised to reshape treatment paradigms, providing robust North America Avascular Necrosis market insights for investors and healthcare providers.

Challenge in North America Avascular Necrosis Market

Lack of Awareness and Late Diagnosis

Late-stage diagnosis remains a key challenge, with 35–40% of patients presenting after joint collapse. Frequency of early-stage detection remains at only 30% of total AVN cases, highlighting the need for awareness campaigns. Limited knowledge among primary care providers delays referrals, contributing to reduced adoption of surgical and regenerative treatments. These barriers constrain North America Avascular Necrosis market growth and demand, emphasizing the importance of early detection programs and educational initiatives.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.17 billion |

| Market Size in 2026 | USD 1.27 billion |

| Market Size in 2034 | USD 2.45 billion |

| CAGR | 8.3% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

North America Avascular Necrosis Market Segmentation

By Type

Early-stage AVN represents 25% of North America market share, with 80,000 procedures performed in 2025. Core decompression and bone marrow grafting are primary interventions, offering performance improvements of 18–22% over traditional methods. MRI detection sensitivity for early-stage is 92%, with procedure frequency averaging 1.5 per patient. Early-stage AVN treatment drives regional market insights due to faster recovery and reduced long-term costs.

Mid-stage AVN contributes 40% market share, with 130,000 procedures in 2025. Treatment includes vascularized bone grafting (35%) and osteotomy (20%). Technical metrics show 85% success rate and post-operative recovery averaging six months. Market demand is influenced by 60% adoption of minimally invasive techniques, highlighting mid-stage’s role in North America Avascular Necrosis market growth.

Late-stage AVN accounts for 35% of the market, with 115,000 procedures in 2025. Total hip arthroplasty is the dominant intervention (75%), supplemented by knee and shoulder replacements. Frequency of joint replacements averages 1.8 per patient, and procedure volumes are projected to reach 210,000 units by 2034. Late-stage AVN represents the highest revenue generation segment, reinforcing market size and growth insights.

By Application

Surgical treatments represent 55% of the market, with 175,000 procedures in 2025. Hip surgeries account for 68%, knee for 18%, shoulder for 14%. Technical specifications include minimally invasive core decompression and arthroplasty, with recovery times averaging 4–6 weeks. Adoption in US centers is 72%, in Canada 55%, highlighting regional demand differences. Surgical interventions drive North America Avascular Necrosis market insights with high revenue and procedure volumes.

Non-surgical therapies comprise 30% market share, with 95,000 procedures in 2025. Stem cell injections, physiotherapy, and pharmacological adjuvants are key methods. Usage penetration is 60% among early-stage AVN patients, technical efficacy improving by 15–20%. The segment’s growth is influenced by increasing patient preference for non-invasive options, reinforcing North America Avascular Necrosis market demand.

Pharmacological interventions hold 15% share, with 48,000 units in 2025. Bisphosphonates, statins, and anticoagulants are primary drugs, with performance improvements of 10–12%. Adoption rates are 40% in early-stage AVN, particularly in outpatient settings. The segment provides steady revenue streams, complementing surgical and non-surgical treatments, reinforcing market insights and growth forecasts.

North America Avascular Necrosis Market Segmentations

Type

- Early-stage

- Mid-stage

- Late-stage

Treatment

- Surgical

- Non-surgical

- Pharmacological

Country Insights

United States

The United States contributes 75% of North America Avascular Necrosis market, with 245,000 procedures in 2025 and projected 430,000 units by 2034. Hip joint treatments dominate at 68%, knee 18%, shoulder 14%. Over 1,150 specialized facilities adopt advanced imaging (72% penetration) and minimally invasive techniques. The region’s contribution to revenue reached USD 950 million in 2025, projected to exceed USD 1.8 billion by 2034. These metrics underscore the US as the primary driver of regional market insights and growth trends.

Canada

Canada accounts for 25% of North America Avascular Necrosis market, with 80,000 procedures in 2025, expected to reach 120,000 units by 2034. Surgical interventions dominate at 55%, non-surgical at 30%, pharmacological 15%. Hip joint procedures contribute 62%, knee 25%, shoulder 13%. Technical adoption includes MRI (65% penetration) and minimally invasive surgeries (50%). Canadian market insights are characterized by moderate growth (7.2% CAGR) and steady demand, reinforcing regional diversification of the North America Avascular Necrosis market.

Top Players in North America Avascular Necrosis Market

- Zimmer Biomet Holdings, Inc.

- Stryker Corporation

- Johnson & Johnson Services, Inc.

- Medtronic plc

- Smith & Nephew plc

- Arthrex, Inc.

- Wright Medical Group N.V.

- CONMED Corporation

- NuVasive, Inc.

- Globus Medical, Inc.

- DJO Global, Inc.

- Exactech, Inc.

- B. Braun Melsungen AG

- Integra LifeSciences Holdings Corporation

- Ossur hf

Top Companies

Zimmer Biomet Holdings, Inc.

- Market share: 18% of North America Avascular Necrosis market in 2025

- Positioning: Leading provider of hip and knee arthroplasty systems, with advanced minimally invasive technology adoption. Annual production exceeded 42,000 units in 2025, with performance improvement of 15%. Their extensive US network of 250 facilities ensures regional dominance and continuous R&D investment, reinforcing market growth and trend insights.

Stryker Corporation

- Market share: 14% in North America Avascular Necrosis market in 2025

- Positioning: Key competitor with innovative hip and knee replacement solutions. Production volume reached 32,000 units in 2025, with 12–14% efficiency improvement. Stryker’s emphasis on robotic-assisted surgery and regenerative medicine enhances procedural adoption, reinforcing North America Avascular Necrosis market insights and competitive dynamics.

Investment

North America Avascular Necrosis market investment allocation in 2025 reached USD 450 million, with 55% directed toward surgical innovation, 25% toward non-surgical therapies, and 20% toward pharmacological advancements. Regional investment concentration is 70% in the United States and 30% in Canada, reflecting market size and procedure volume dominance.

Sector-wise, surgical segment investment in minimally invasive techniques accounts for USD 247 million, stem cell and regenerative therapies USD 112 million, and pharmacological drug development USD 91 million. M&A activity in North America saw 6 major agreements between 2022–2025, including collaborations for joint arthroplasty innovations and regenerative medicine startups. Investment trends indicate strong growth potential in early and mid-stage AVN treatments, reinforcing North America Avascular Necrosis market insights and stakeholder opportunities.

New Product

In 2025, approximately 22% of North America Avascular Necrosis products were newly introduced, primarily in minimally invasive surgical tools and regenerative medicine. Performance improvements averaged 15–20%, with innovation metrics showing increased adoption of MRI-compatible implants and robotic-assisted devices. Product launches focused on early-stage AVN detection and treatment, reinforcing market growth by enhancing procedural efficiency and patient recovery. Continuous innovation ensures the North America Avascular Necrosis market remains competitive and dynamic, driven by technology adoption and procedural optimization.

Recent Development in North America Avascular Necrosis Market

- 2022: Zimmer Biomet launched next-gen hip implant, increasing US production by 12% with improved durability and minimally invasive applicability.

- 2023: Stryker introduced robotic-assisted hip replacement, achieving 14% reduction in surgical time and 8% higher procedural volume.

- 2023: Medtronic initiated regenerative stem cell program, increasing treatment volume by 18,000 units, reflecting 15% growth.

Research Methodology for North America Avascular Necrosis Market

The North America Avascular Necrosis market research follows a structured methodology combining primary and secondary research. Primary research includes interviews with orthopedic surgeons, hospital procurement managers, and industry stakeholders to validate market trends, adoption rates, and procedural volumes. Secondary research involves examining peer-reviewed journals, medical reports, company filings, and government healthcare databases to gather historical data from 2022–2024. Market size estimation leverages a top-down and bottom-up approach, integrating procedure volumes, treatment adoption, unit pricing, and segment share. Forecasting utilizes CAGR calculation and trend extrapolation, with adjustments for technological advancements, regulatory policies, and demographic shifts. The methodology ensures robust, data-driven insights and accurate projections, reinforcing North America Avascular Necrosis market growth, size, and demand analysis.

Frequently Asked Questions

Market Research Analyst | 7 Years Experience | Biologics and Clinical Trial Ecosystems

Jessica Richardson is a market research analyst with 7–9 years of experience specializing in healthcare and life sciences markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.