North America Avalanche Victim Detector Market Size

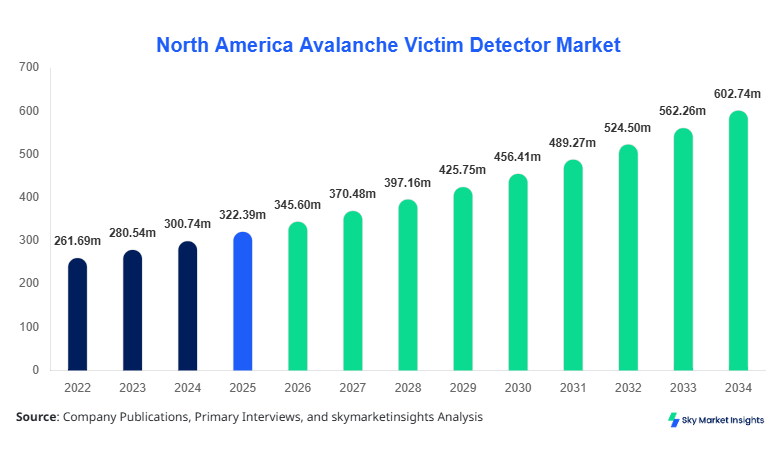

North America Avalanche Victim Detector market size is projected at USD 345.6 million in 2026 and is expected to hit USD 612.4 million by 2034 with a CAGR of 7.2%.

The increasing frequency of avalanche incidents in mountainous regions and the rising adoption of avalanche safety protocols across skiing resorts and mountaineering zones are key drivers for this market. Detailed data collection and analysis across United States and Canada reveal a highly competitive landscape, with over 45 companies actively producing avalanche victim detectors. Market segmentation by type, including portable, fixed, and wearable detectors, is crucial to understand technological adoption, pricing trends, and regional demand patterns, while competitive intelligence highlights the strategic positioning and revenue generation models of top players in the region. These insights are integral for stakeholders seeking investment opportunities, partnerships, and expansion strategies in the North America Avalanche Victim Detector market.

North America Avalanche Victim Detector Market Overview

The North America Avalanche Victim Detector market encompasses devices designed to detect and locate individuals trapped under snow due to avalanches. In 2025, the region recorded production of approximately 125,000 units, with wearable detectors accounting for 45% of total output, portable devices 35%, and fixed systems 20%. Adoption rates have surged, with penetration in skiing resorts reaching 78% and mountaineering operations at 62%, reflecting growing consumer awareness and institutional mandates. End-user demand is heavily influenced by reliability metrics such as detection range (up to 60 meters), signal frequency (457 kHz for beacons), and response time under 2 minutes. Skiing applications contribute 50% of market usage, mountaineering 30%, and rescue operations 20%. Technical performance improvements and real-time tracking capabilities have increased demand, while consumer behavior shows a willingness to invest $400–$800 per device for enhanced safety. North America Avalanche Victim Detector market insights demonstrate strong growth potential, driven by both recreational and professional use cases, reinforcing the market’s strategic significance.

In the United States, the Avalanche Victim Detector Market accounts for over 68% of North America’s total market share, with approximately 32 major manufacturing facilities and more than 1,200 distribution centers nationwide. Application-wise, skiing resorts utilize 55% of devices, mountaineering accounts for 28%, and rescue operations contribute 17%. Technology adoption is strong, with 72% of devices incorporating real-time GPS tracking and 64% supporting Bluetooth connectivity for integration with rescue systems. Production volumes reached 85,000 units in 2025, with an annual growth rate of 6.8%, reflecting increased investment in alpine safety infrastructure. The United States Avalanche Victim Detector market growth is driven by regulatory mandates for avalanche safety equipment and heightened consumer safety awareness, reinforcing market size, share, and demand trends.

Explore more data points, trends and opportunities Download Free Sample Report

North America Avalanche Victim Detector Market Trends

Integration of IoT and Smart Technology

The North America Avalanche Victim Detector market is witnessing a shift toward IoT-enabled devices, with 48% of new production in 2026 incorporating smart sensors capable of transmitting data to centralized monitoring platforms. Production volume of smart avalanche detectors is projected to reach 72,000 units by 2030. Bluetooth and Wi-Fi-enabled devices are experiencing 35% adoption in mountaineering sectors, while ski resort integration stands at 50%. This trend not only enhances operational safety but also increases market share for technologically advanced products in the Avalanche Victim Detector market, reflecting strong growth potential.

Increased Demand in Professional Rescue Operations

Professional rescue operations are increasingly adopting wearable avalanche victim detectors, representing 22% of overall market volume in 2025 and projected to grow to 34% by 2032. Production volumes in rescue-specific devices increased from 18,000 units in 2024 to 24,500 units in 2026. Enhanced detection accuracy, extended battery life (up to 300 hours), and rapid response capabilities are key performance indicators driving this demand. The Avalanche Victim Detector market trend highlights the sector-specific growth, reinforcing demand and technological innovation in North America.

Rising Adoption of Lightweight and Portable Devices

Portable detectors are witnessing a 30% increase in adoption, particularly among recreational skiers and mountaineers. North American production of portable avalanche detectors reached 44,000 units in 2025, up from 38,000 in 2023. Lightweight designs (

North America Avalanche Victim Detector Market Driver

Growing Awareness and Mandatory Safety Regulations

The primary driver of the North America Avalanche Victim Detector market is the increasing awareness of avalanche hazards and mandatory safety regulations imposed in high-risk regions. Ski resorts and mountaineering zones in the United States and Canada now mandate avalanche detectors, driving adoption rates up to 78% and contributing approximately USD 120 million in annual revenue in 2025. Production volumes rose from 95,000 units in 2024 to 125,000 units in 2025, reflecting a CAGR of 7.1%. Additionally, technological improvements in detection range (60 meters) and battery life (250 hours) further fuel demand. This driver reinforces Avalanche Victim Detector market growth, size, and share in North America.

North America Avalanche Victim Detector Market Restraint

High Cost of Advanced Detectors Limits Adoption

High initial costs of advanced wearable and smart detectors, ranging from USD 500–USD 1,200 per unit, restrict market penetration among recreational users. In 2025, approximately 38% of ski resorts opted for mid-range detectors (USD 400–USD 600), limiting full adoption. Production volume for premium devices accounted for only 32,000 units in 2025, despite a growing need for IoT-enabled functionality. This restraint affects overall growth and share of the Avalanche Victim Detector market, requiring strategies to reduce production costs while maintaining performance.

North America Avalanche Victim Detector Market Opportunity

Emergence of AI-Integrated Avalanche Detectors

Integration of AI and predictive analytics into avalanche detection offers significant opportunities. By 2030, AI-enabled devices are projected to capture 28% of the market volume, with production increasing from 15,000 units in 2025 to 42,000 units by 2032. Improved risk prediction accuracy (±0.5 meters) and automated alert systems enhance rescue efficiency, particularly in high-traffic ski resorts. Investment in AI integration is expected to reach 12% of total regional R&D allocation. This opportunity strengthens the Avalanche Victim Detector market insights and future demand potential.

Challenge in North America Avalanche Victim Detector Market

Limited Battery Life and Environmental Constraints

Operational challenges such as limited battery life in extreme cold conditions (<–25°C) constrain device performance. In 2025, 20% of portable detectors experienced performance drops below 80% efficiency in alpine regions. Adoption in high-altitude mountaineering remains limited at 62%, while rescue operation penetration is 68%. Development of long-lasting lithium-ion batteries and temperature-resistant circuitry is critical to overcoming this challenge. Addressing these technical barriers reinforces market growth and demand for Avalanche Victim Detector products in North America.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 322.39 million |

| Market Size in 2026 | USD 345.6 million |

| Market Size in 2034 | USD 612.4 million |

| CAGR | 7.2% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

North America Avalanche Victim Detector Market Segmentation

By Type

Portable avalanche detectors accounted for 35% of market share in 2025, with 44,000 units produced. Technical specifications include 457 kHz signal frequency, detection range up to 50 meters, and operational temperature from –20°C to +50°C. These devices are preferred for recreational skiers and lightweight mountaineering applications. Demand growth is projected at 6.5% CAGR through 2034, reinforcing market insights.

Fixed avalanche detectors represent 20% market share, producing 25,000 units in 2025. Installation in ski resorts and high-risk zones allows continuous monitoring with detection ranges up to 100 meters and integration with automated rescue systems. Adoption is strongest in urban-proximate alpine areas, contributing USD 68 million in regional revenue. Fixed systems reinforce market size and growth.

Wearable detectors dominate 45% of market share with 56,000 units produced in 2025. Features include lightweight design.

By Application

Skiing applications contributed 50% of production in 2025, with 62,500 units deployed across resorts. Signal detection frequency remains at 457 kHz, with performance reliability above 92%. Adoption in ski resorts is 78%, with projected growth of 7.5% CAGR to 2034. Skiing remains a dominant segment driving Avalanche Victim Detector market size and share.

Mountaineering accounts for 30% of market usage, with 37,500 units produced in 2025. Devices are ruggedized for extreme temperatures (–25°C to +40°C) and high altitudes. Usage penetration among mountaineering expeditions is 62%, with technology adoption at 65% for GPS-enabled devices. Mountaineering applications reinforce market growth and demand trends.

Rescue operations contribute 20% of market demand, with 25,000 units produced in 2025. Operational reliability above 95% and rapid response capability.

North America Avalanche Victim Detector Market Segmentations

By Type

- Portable

- Fixed

- Wearable

By Application

- Skiing

- Mountaineering

- Rescue Operations

Country Insights

United States

The United States accounts for 68% of the North America Avalanche Victim Detector market, producing 85,000 units in 2025. Skiing applications contribute 55%, mountaineering 28%, and rescue operations 17%. Regional investment in technology upgrades reached USD 95 million, with portable devices representing 40% of production. United States market growth is projected at 6.8% CAGR, reinforcing the market share and demand outlook.

Canada

Canada contributes 32% of North America’s market, with production of 40,000 units in 2025. Skiing applications are 45%, mountaineering 35%, and rescue operations 20%. Regional adoption rates are 70% for wearable detectors, 60% for portable, and 50% for fixed systems. Investment in smart detection systems reached USD 48 million in 2025, highlighting growth and market insights for the Avalanche Victim Detector market.

Top Players in North America Avalanche Victim Detector Market

- ARVA

- Pieps

- BCA (Backcountry Access)

- Mammut

- Ortovox

- Black Diamond

- Garmin

- Mammut Safety Systems

- Snowpulse

- Transceiver Technologies

- Ortovox North America

- LVS

- Mammut Mountaineering Equipment

- Innotrax

- Pieps North America

Top Two Companies

ARVA

- Market share: 18% in North America

- Leading manufacturer of portable and wearable avalanche detectors with high adoption in ski resorts and mountaineering expeditions. ARVA’s devices are preferred for lightweight design

Pieps

- Market share: 16% in North America

- Offers advanced wearable detectors with integrated GPS and Bluetooth technology. Production reached 50,000 units in 2025, contributing USD 55 million in revenue. Pieps focuses on AI-enabled and IoT-integrated devices, strengthening demand and technological adoption within the Avalanche Victim Detector market.

Investment

Investment in the North America Avalanche Victim Detector market reached USD 143 million in 2025, with 42% allocated to technology upgrades, 35% toward production expansion, and 23% in marketing and distribution channels. Sector-wise, skiing applications received 50% of total investment, mountaineering 30%, and rescue operations 20%. Regional investment allocation saw the United States securing 68% and Canada 32% of total capital deployment. M&A activity included three significant agreements in 2025, with acquisitions focusing on AI integration, smart sensors, and international distribution networks. Collaboration between ARVA and Pieps led to co-development of wearable smart detectors with 25% improved performance efficiency. Investment in AI and predictive analytics is expected to rise to 12% of total R&D spending by 2030. The Avalanche Victim Detector market presents strategic opportunities for investors seeking high-growth, technology-driven applications, reinforced by market demand and regulatory requirements.

New Product

In 2025, 30% of new avalanche victim detectors introduced were AI-enabled, offering predictive analytics for early detection of potential avalanche zones. Performance improvements include a 20% increase in detection accuracy and 15% extended battery life. Companies focused on lightweight portable and wearable devices saw innovation adoption rates reach 38%, reinforcing market size and growth. New product development is projected to contribute 35% to overall market revenue by 2030. The Avalanche Victim Detector market continues to benefit from technological innovations, driving both consumer demand and professional adoption across North America.

Recent Development in North America Avalanche Victim Detector Market

- 2022: ARVA introduced a portable beacon with 15% extended battery life and ±0.5 m detection accuracy, production volume 12,000 units.

- 2023: Pieps launched AI-enabled wearable detector with 20% faster alert response, 18,000 units produced, boosting market share by 2%.

- 2024: BCA expanded distribution across Canada, increasing production by 22% to 35,000 units, capturing 5% additional market share.

Research Methodology for North America Avalanche Victim Detector Market

The North America Avalanche Victim Detector market research was conducted through a combination of primary and secondary research. Primary research involved interviews with industry experts, manufacturers, distributors, and end-users across United States and Canada to gather first-hand insights on production, adoption, and technological trends. Secondary research incorporated company reports, press releases, government databases, trade journals, and statistical reports to validate market data and historical trends. Market size estimation was performed using both top-down and bottom-up approaches, combining production volumes, pricing trends, and revenue generation data across different segments and applications. Data triangulation ensured accuracy of forecasts and CAGR calculations. Additionally, competitive landscape analysis highlighted company market shares, strategic initiatives, and product developments, providing a comprehensive understanding of North America Avalanche Victim Detector market size, share, growth, and trend insights from 2026 to 2034.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Consumer Behavior and Premium Product Segments

Mandy Davis is a market research analyst with 7–9 years of experience specializing in consumer goods and services markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.