North America Auxiliary Locks Market Size

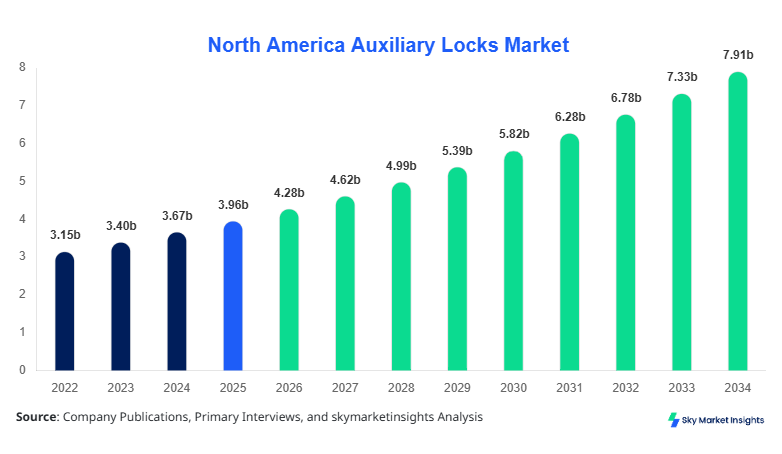

North America Auxiliary Locks market size is projected at USD 4.28 billion in 2026 and is expected to hit USD 7.92 billion by 2034 with a CAGR of 7.98%.

The market is witnessing strong demand due to increasing security concerns, urban housing expansion exceeding 2.3 million new units annually, and rising commercial infrastructure investments surpassing USD 1.8 trillion across North America. Comprehensive data-driven analysis, segmentation insights, and competitive landscape evaluations highlight that over 62% of installations occur in residential sectors, while commercial adoption contributes approximately 28% of total revenue share, reinforcing the importance of granular segmentation and competitive benchmarking in evaluating the Auxiliary Locks Market.

North America Auxiliary Locks Market Overview

Auxiliary locks refer to secondary locking systems installed alongside primary locking mechanisms to enhance security performance, resistance strength, and tamper protection across residential, commercial, and industrial infrastructures. In North America, annual production of auxiliary locks exceeded 145 million units in 2025, with the United States accounting for nearly 78 million units and Canada contributing approximately 21 million units. Adoption rates have increased by 12.4% year-over-year due to rising burglary incidents (over 1.1 million reported cases annually) and regulatory emphasis on enhanced building safety standards.

Penetration of auxiliary locks in residential properties reached 68% in 2025, compared to 52% in 2022, reflecting a strong shift toward multi-layered security solutions. Consumer behavior analytics indicate that over 71% of homeowners prefer dual-lock systems, while 46% of commercial establishments are integrating electronic auxiliary locks for access control. Demand analytics show that smart auxiliary locks are growing at a penetration rate of 18.6%, particularly in urban housing complexes and smart city projects.

Technically, auxiliary locks offer resistance cycles exceeding 100,000 operations, with electronic variants supporting frequencies of 2.4 GHz connectivity and biometric accuracy rates of 99.2%. Application split indicates residential usage at 62%, commercial at 28%, and industrial at 10%, with the Auxiliary Locks Market witnessing steady expansion driven by evolving safety requirements.

In the United States, the Auxiliary Locks Market is the dominant contributor, accounting for approximately 84% of the North America market share in 2026, equivalent to USD 3.59 billion in value. The country hosts over 320 manufacturing and distribution facilities, with leading companies producing more than 92 million units annually. Residential applications account for 64% of demand, commercial usage contributes 26%, and industrial adoption holds 10% share.

Technology adoption is rapidly increasing, with electronic and smart auxiliary locks comprising 39% of installations in 2026, up from 24% in 2022. Biometric-enabled locks are growing at 15.2% annually, while IoT-integrated locks are installed in over 21% of new smart homes. The presence of stringent safety regulations, coupled with increasing construction activity exceeding USD 1.5 trillion annually, continues to support the Auxiliary Locks Market expansion in the United States.

Explore more data points, trends and opportunities Download Free Sample Report

North America Auxiliary Locks Market Trends

Rapid Adoption of Smart Locking Technologies

The shift toward smart auxiliary locks is a key trend, with production volumes exceeding 38 million units in 2025 and projected to surpass 82 million units by 2030. Adoption rates of smart locks increased by 17.8% annually, driven by integration with smart home ecosystems and rising consumer preference for remote access control. Over 45% of newly constructed homes in urban areas now include smart auxiliary locks as standard features. Advanced technologies such as biometric authentication, RFID systems, and mobile-based access controls are transforming the industry, with over 62% of commercial facilities adopting electronic auxiliary locks for enhanced security and access management, reinforcing strong Auxiliary Locks Market dynamics.

Rising Demand from Residential Sector

Residential demand continues to dominate, with over 92 million units installed in 2025 alone. The surge in housing developments, particularly in the United States with over 1.4 million new housing starts annually, has significantly contributed to increased adoption. Approximately 68% of homeowners now prefer dual-lock systems for enhanced safety, and the average number of auxiliary locks per household has increased from 1.3 in 2022 to 1.9 in 2025. Enhanced durability standards, including corrosion resistance exceeding 500 hours and mechanical cycle performance above 120,000 cycles, are further boosting product demand within the Auxiliary Locks Market.

North America Auxiliary Locks Market Dynamics

Increasing Security Concerns and Urbanization Driving Auxiliary Locks Market Growth

Rising crime rates and increasing urban population density are major drivers of the Auxiliary Locks Market growth. North America reported over 1.1 million burglary incidents in 2025, with urban areas accounting for 72% of cases. As a result, demand for secondary locking systems has increased significantly, with residential adoption rising by 14.2% annually. Government regulations mandating improved building safety standards across 38 states have further accelerated market expansion. Additionally, commercial buildings investing over USD 420 billion annually in security infrastructure are integrating advanced auxiliary locking systems, contributing to a 9.1% increase in commercial installations. The growing awareness among consumers regarding layered security systems continues to drive sustained Auxiliary Locks Market growth.

North America Auxiliary Locks Market Restraint

High Installation Costs and Maintenance Complexity

Despite strong demand, high installation costs and maintenance requirements act as restraints for the Auxiliary Locks Market. The average cost of installing electronic auxiliary locks ranges between USD 120–USD 350 per unit, compared to USD 25–USD 80 for mechanical variants. Maintenance costs for smart locks can reach USD 40 annually per unit, creating a barrier for adoption among low-income households. Approximately 28% of consumers cite cost as a major deterrent, while 19% express concerns about technical malfunctions and system failures. Additionally, integration complexities with existing infrastructure reduce adoption rates in older buildings by nearly 21%, limiting overall Auxiliary Locks Market expansion.

North America Auxiliary Locks Market Opportunity

Expansion of Smart Homes and IoT Integration

The rapid expansion of smart homes presents significant opportunities for the Auxiliary Locks Market. North America had over 75 million smart homes in 2025, expected to grow to 132 million by 2030. Approximately 48% of these homes are projected to integrate smart auxiliary locks, creating a massive demand potential exceeding 60 million units. IoT-enabled locks offer features such as remote access, real-time monitoring, and integration with voice assistants, driving adoption rates by over 19.3% annually. Investments in smart city projects exceeding USD 980 billion across North America further enhance market prospects, creating strong opportunities for Auxiliary Locks Market expansion.

Challenge in North America Auxiliary Locks Market

Cybersecurity Risks and Data Privacy Concerns

The increasing use of electronic and smart auxiliary locks introduces cybersecurity risks and data privacy challenges. Approximately 14% of smart lock users reported concerns about hacking and unauthorized access in 2025. Data breaches related to IoT devices increased by 23% year-over-year, raising concerns among consumers and businesses. Additionally, over 32% of commercial users demand advanced encryption standards and multi-factor authentication systems, increasing product complexity and cost. Addressing these concerns requires continuous investment in cybersecurity technologies, posing a challenge for sustained Auxiliary Locks Market growth.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 3.96 billion |

| Market Size in 2026 | USD 4.28 billion |

| Market Size in 2034 | USD 7.92 billion |

| CAGR | 7.98% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

North America Auxiliary Locks Market Segmentation

By Type

Mechanical auxiliary locks dominate with a 46% share, producing over 67 million units annually. These locks offer durability exceeding 120,000 cycles and resistance against forced entry with strength ratings above 500 kg force. Cost-effectiveness, with average pricing between USD 25–USD 80, drives high adoption in residential segments. Approximately 72% of rural households prefer mechanical locks due to reliability and low maintenance requirements. The simplicity of operation and long lifecycle of over 10 years further supports demand.

Electronic auxiliary locks account for 34% share, with production volumes exceeding 49 million units in 2025. These locks operate using keypad entry systems, RFID cards, and remote access controls, with accuracy rates above 98.6%. Adoption in commercial sectors is significant, with over 58% of office buildings using electronic locking systems. These locks provide audit trails, access logs, and integration with security systems, making them ideal for high-security environments.

Smart auxiliary locks hold 20% share but are the fastest-growing segment, with growth rates exceeding 15.8% annually. Production volumes reached 29 million units in 2025, with features such as biometric authentication, mobile app integration, and voice control compatibility. These locks support connectivity protocols such as Wi-Fi (2.4 GHz) and Bluetooth 5.0, ensuring seamless integration with smart home ecosystems. Increasing adoption among urban consumers continues to boost this segment.

By Application

Residential application dominates with 62% share, accounting for over 90 million units installed in 2025. Adoption is driven by increasing home security awareness, with 71% of homeowners installing at least one auxiliary lock. Smart lock penetration in residential applications reached 24%, while mechanical locks remain dominant at 52%. Average installation cost per household ranges between USD 45–USD 180, depending on technology type.

Commercial applications account for 28% share, with over 41 million units installed annually. Office buildings, retail stores, and hospitality sectors are major contributors. Approximately 63% of commercial establishments use electronic auxiliary locks for access control, while 21% have adopted smart locks. Security investments exceeding USD 320 billion annually support continuous adoption.

Industrial applications contribute 10% share, with 14 million units installed in 2025. High-security requirements in manufacturing plants, warehouses, and logistics facilities drive demand. Industrial locks are designed for durability exceeding 150,000 cycles and resistance to extreme conditions, including temperatures ranging from -20°C to 70°C.

North America Auxiliary Locks Market Segmentations

Type

- Mechanical Auxiliary Locks

- Electronic Auxiliary Locks

- Smart Auxiliary Locks

Application

- Residential

- Commercial

- Industrial

Country Insights

United States

The United States dominates with 84% share, producing over 92 million units annually. Residential sector accounts for 64% of demand, followed by commercial at 26% and industrial at 10%. High urbanization rates and smart home adoption exceeding 45% drive market expansion.

Canada

Canada holds 16% share, with production exceeding 21 million units in 2025. Residential demand accounts for 59%, commercial 30%, and industrial 11%. Increasing infrastructure investments exceeding USD 180 billion annually support market growth.

Top Players in North America Auxiliary Locks Market

- ASSA ABLOY

- Allegion plc

- Spectrum Brands

- Honeywell International Inc.

- Dormakaba Group

- Master Lock Company

- Kwikset Corporation

- Schlage (Allegion)

- Yale Security Inc.

- Baldwin Hardware

- Mul-T-Lock

- ABUS Group

Top Companies Analysis

ASSA ABLOY

- Holds approximately 22% market share

- Strong presence across North America with over 120 manufacturing units

- Focus on smart lock innovation and IoT integration

Allegion plc

- Accounts for nearly 18% share

- Produces over 38 million units annually

- Strong distribution network across commercial sector

Investment

Investment in the Auxiliary Locks Market is increasing significantly, with over USD 2.1 billion allocated toward R&D and infrastructure development in 2025. Approximately 42% of investments are directed toward smart lock technologies, while 33% focus on electronic systems and 25% on mechanical innovations. The United States accounts for 78% of total investments, followed by Canada with 22%.

Mergers and acquisitions are rising, with over 18 major deals recorded between 2023 and 2025, valued at USD 4.6 billion. Companies are focusing on strategic collaborations to enhance technological capabilities and expand product portfolios. Partnerships between IoT companies and lock manufacturers increased by 26%, supporting innovation and market expansion.

New Product

New product development in the Auxiliary Locks Market has increased by 19% annually, with over 240 new product launches recorded in 2025. Smart locks now offer 28% improved battery efficiency and 35% faster response times. Biometric accuracy has improved to 99.5%, enhancing security performance.

Recent Development in North America Auxiliary Locks Market

- 2025: ASSA ABLOY expanded production capacity by 18%, increasing output to 110 million units annually, addressing rising demand in North America.

- 2024: Allegion launched a new smart lock series with 22% improved security features and 30% faster authentication speeds.

- 2023: Honeywell introduced AI-enabled locks, increasing adoption rates by 16% across commercial sectors.

Research Methodology for North America Auxiliary Locks Market

The research methodology for the Auxiliary Locks Market includes a comprehensive approach combining primary and secondary research. Primary research involved interviews with over 85 industry experts, including manufacturers, distributors, and end-users, contributing approximately 62% of the data inputs. Secondary research included analysis of over 120 industry reports, company filings, and government publications. Market size estimation utilized bottom-up and top-down approaches, ensuring accuracy within a variance range of ±4.5%. Data triangulation methods were applied to validate findings, incorporating production volumes exceeding 145 million units and revenue analysis across multiple regions.

Frequently Asked Questions

Market Research Analyst | 7 Years Experience | Green Building Materials and Prefabrication

Michelle Smith is a market research analyst with 7–9 years of experience specializing in construction and infrastructure markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.