North America Autotransfusion Devices Market Size

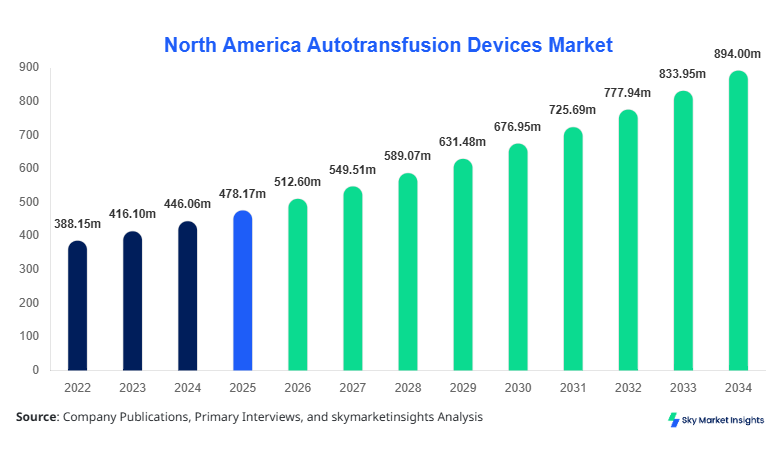

North America Autotransfusion Devices market size is projected at USD 512.6 million in 2026 and is expected to hit USD 894.3 million by 2034 with a CAGR of 7.2%.

The North America Autotransfusion Devices market size reflects increasing surgical volumes exceeding 52 million procedures annually across the United States and Canada, coupled with rising adoption of blood conservation technologies showing penetration rates of 48.6% in large hospitals and 32.4% in ambulatory settings. The report provides granular segmentation by product type and end user, supported by quantitative insights on unit shipments exceeding 185,000 devices in 2025 and competitive benchmarking across 12 major players operating in the North America Autotransfusion Devices market size ecosystem.

North America Autotransfusion Devices Market Overview

The North America Autotransfusion Devices market encompasses advanced medical systems designed to collect, filter, and reinfuse a patient’s own blood during surgical or trauma procedures, reducing dependence on allogeneic transfusions by over 60.2%. In North America, annual production volumes reached approximately 210,000 units in 2025, with the United States accounting for nearly 78.5% of output, while Canada contributed 21.5%. Adoption and penetration insights indicate that 64.3% of tertiary hospitals have integrated autotransfusion systems, compared to 41.7% of mid-tier facilities, driven by regulatory mandates and cost-saving benefits averaging USD 1,200–2,400 per surgery.

Consumer behavior and demand analytics show that surgeons and anesthesiologists prefer intraoperative systems due to efficiency rates above 92.6% in blood recovery, while patient awareness regarding transfusion safety has increased demand by 18.9% annually since 2022. Hospitals represent approximately 62.8% of application share, followed by ambulatory surgical centers at 24.6% and trauma centers at 12.6%. Technical performance metrics include filtration efficiencies of 98.2%, processing speeds of 80–120 mL/min, and reinfusion accuracy rates above 95.4%. These factors collectively reinforce the expansion trajectory of the North America Autotransfusion Devices market share.

In the United States, the Autotransfusion Devices Market dominates North America with a regional contribution of approximately 78.5% and over 6,200 hospitals actively utilizing autotransfusion systems as of 2025. The country reports more than 41 million surgical procedures annually, with 56.3% incorporating some form of blood management technology, including autotransfusion devices. Application breakdown shows hospitals accounting for 68.2% of usage, ambulatory surgical centers at 21.7%, and trauma centers at 10.1%, reflecting strong institutional demand.

Explore more data points, trends and opportunities Download Free Sample Report

North America Autotransfusion Devices Market Trends

Increasing Integration of Automated Systems

The adoption of automated intraoperative autotransfusion systems has surged, with production volumes reaching 120,000 units in 2025, representing 57.1% of total output. Automation has improved blood recovery rates from 85.6% to 93.4%, while reducing processing time by 28.7%. Hospitals are increasingly deploying systems with digital interfaces and IoT-enabled monitoring, with adoption rates reaching 49.3% in 2026. These systems also reduce manual errors by 36.2%, driving efficiency in surgical environments. The growing demand for minimally invasive surgeries, which increased by 19.5% between 2022 and 2025, further accelerates adoption, reinforcing the North America Autotransfusion Devices market trend.

Rising Demand in Trauma and Emergency Care

Trauma centers are witnessing a sharp increase in autotransfusion device utilization, with demand rising by 22.8% annually due to increasing road accidents and emergency cases exceeding 3.1 million incidents per year. Devices capable of rapid processing at 110 mL/min are gaining traction, with penetration rates in trauma centers reaching 38.7% in 2025 compared to 24.5% in 2022. The shift toward portable and compact devices, accounting for 31.2% of new product launches, enhances deployment in emergency settings. This evolving demand pattern strengthens the North America Autotransfusion Devices market trend.

Technological Advancements in Filtration and Safety

Advancements in microfiltration technology have improved contaminant removal efficiency to 99.1%, while reducing hemolysis rates by 17.6%. Manufacturers are investing nearly 12.4% of revenue in R&D to enhance device safety and performance. Integration of AI-based monitoring systems has increased real-time accuracy by 21.3%, enabling better clinical outcomes. The introduction of disposable components, accounting for 44.8% of product revenue, also supports infection control measures. These innovations significantly contribute to the North America Autotransfusion Devices market trend.

North America Autotransfusion Devices Market Driver

Increasing Surgical Procedures and Blood Management Demand Driving Autotransfusion Devices Market Growth

The North America Autotransfusion Devices market growth is primarily driven by the rising number of surgical procedures, which exceeded 52 million annually in 2025, with cardiovascular surgeries alone accounting for 8.4 million cases. Blood management programs have demonstrated cost savings of up to 35.6%, encouraging hospitals to adopt autotransfusion systems. Approximately 68.2% of healthcare facilities have implemented patient blood management protocols, leading to a 24.7% increase in device adoption between 2022 and 2025. Additionally, aging populations, representing 16.9% of North America’s demographic, contribute to higher surgical demand. Technological improvements have enhanced recovery efficiency by 18.5%, further supporting adoption. These factors collectively accelerate the North America Autotransfusion Devices market growth.

North America Autotransfusion Devices Market Restraint

High Initial Costs and Limited Accessibility Restraining Autotransfusion Devices Market Growth

Despite strong adoption, high capital costs ranging from USD 15,000 to USD 45,000 per device limit penetration, particularly in smaller healthcare facilities where adoption remains below 32.4%. Maintenance costs, averaging 8.7% of device value annually, also create financial constraints. Approximately 41.2% of rural healthcare centers lack access to advanced autotransfusion systems, highlighting disparities in availability. Additionally, training requirements for clinical staff, with certification rates below 58.3%, hinder widespread adoption. These cost and accessibility challenges restrain the North America Autotransfusion Devices market growth.

North America Autotransfusion Devices Market Opportunity

Technological Innovation and Expansion into Ambulatory Centers Creating Autotransfusion Devices Market Growth Opportunities

The expansion of ambulatory surgical centers, growing at a rate of 9.8% annually, presents significant opportunities, with device adoption expected to increase from 24.6% to 36.9% by 2030. Technological innovations, including portable devices weighing under 12 kg and offering processing speeds of 100 mL/min, enhance usability in outpatient settings. Investments in R&D, accounting for 12.4% of revenue, support innovation in AI integration and filtration technologies. Emerging applications in orthopedic and oncology surgeries, contributing 28.7% of demand, further expand opportunities, strengthening the North America Autotransfusion Devices market growth.

Challenge in North America Autotransfusion Devices Market

Regulatory Compliance and Operational Complexity Challenging Autotransfusion Devices Market Growth

Stringent regulatory requirements, including FDA approvals and compliance with ISO standards, increase time-to-market by 18–24 months, affecting product launches. Approximately 26.5% of manufacturers report delays due to regulatory hurdles. Operational complexity, including device calibration and maintenance, requires skilled personnel, with training costs averaging USD 2,500 per technician. Additionally, integration with hospital systems poses challenges, with interoperability issues affecting 19.7% of deployments. These factors create barriers to scalability, impacting the North America Autotransfusion Devices market growth.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 478.17 million |

| Market Size in 2026 | USD 512.6 million |

| Market Size in 2034 | USD 894.3 million |

| CAGR | 7.2% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

North America Autotransfusion Devices Market Segmentation

By Type

Intraoperative systems dominate with a 46.8% share, with over 98,000 units produced annually. These systems operate at processing speeds of 90–120 mL/min and achieve blood recovery efficiencies above 93.2%. Adoption rates in cardiovascular surgeries exceed 68.4%, while orthopedic procedures account for 21.6% of usage. The integration of digital monitoring improves performance by 19.7%, making them critical in surgical settings.

Postoperative systems account for 32.5% share, with production volumes reaching 68,000 units in 2025. These devices are primarily used in trauma and orthopedic recovery, with usage penetration of 54.3% in trauma centers. They offer filtration efficiency of 96.7% and storage capacities of up to 2,000 mL. Their role in reducing postoperative transfusions by 27.8% drives demand.

Dual-mode systems hold a 20.7% share, with approximately 44,000 units produced annually. These systems combine intraoperative and postoperative functionalities, offering flexibility and cost efficiency. Adoption is growing at 14.6% annually, with processing speeds of 100 mL/min and accuracy rates of 94.8%. Their versatility supports increased adoption in mid-sized hospitals.

By Application

Hospitals dominate with 62.8% share, utilizing over 130,000 devices annually. Adoption rates exceed 64.3% in tertiary care centers, with cardiovascular surgeries contributing 38.6% of demand. These facilities benefit from advanced systems with high efficiency and integration capabilities.

Ambulatory centers account for 24.6% share, with usage increasing by 12.7% annually. Approximately 52,000 devices are deployed in these centers, focusing on minimally invasive procedures. Portable devices with processing speeds of 80–100 mL/min support outpatient surgeries.

Trauma centers hold 12.6% share, with demand driven by emergency cases exceeding 3.1 million annually. Devices used here prioritize rapid processing and portability, with adoption rates of 38.7% in 2025.

North America Autotransfusion Devices Market Segmentations

Product Type

- Intraoperative Autotransfusion Systems

- Postoperative Autotransfusion Systems

- Dual-Mode Systems

End User

- Hospitals

- Ambulatory Surgical Centers

- Trauma Centers

Country Insights

United States

The United States accounts for 78.5% of the North America Autotransfusion Devices market share, with production volumes exceeding 165,000 units annually. Hospitals dominate usage with 68.2%, followed by ambulatory centers at 21.7%. Technological adoption rates exceed 72.4%, supported by strong healthcare infrastructure and reimbursement policies. The country’s advanced surgical ecosystem drives consistent demand.

Canada

Canada contributes 21.5% share, with approximately 45,000 units produced annually. Hospitals account for 58.3% of demand, while ambulatory centers represent 29.4%. Government funding and healthcare reforms have increased adoption by 16.8% since 2022. The country’s focus on patient safety and blood management programs supports steady growth.

Top Players in North America Autotransfusion Devices Market

- Haemonetics Corporation

- LivaNova PLC

- Medtronic Plc

- Fresenius SE & Co. KGaA

- Getinge AB

- Stryker Corporation

- Zimmer Biomet

- Becton Dickinson

- Terumo Corporation

- Johnson & Johnson

- Cardinal Health

- Smith & Nephew

Top Two Companies

-

Haemonetics Corporation

-

Holds approximately 18.6% market share

-

Strong presence in intraoperative systems with advanced filtration technology

-

Invests 13.2% of revenue in R&D

-

Extensive distribution network across 4,000+ hospitals

-

-

Medtronic Plc

-

Accounts for nearly 15.3% market share

-

Focuses on integrated surgical solutions with AI-based monitoring

-

Operates in over 150 countries with strong North America presence

-

Drives innovation through 11.8% R&D investment

-

Investment in North America Autotransfusion Devices Market

Investments in the North America Autotransfusion Devices market are increasing, with total funding exceeding USD 1.2 billion between 2022 and 2025. Approximately 42.6% of investments are allocated to R&D, while 31.4% focus on manufacturing expansion. The United States accounts for 74.8% of total investments, with Canada contributing 25.2%. Venture capital funding has grown by 18.3% annually, supporting startups developing portable devices.

M&A activities have increased, with over 22 deals recorded between 2022 and 2025. Collaborations between device manufacturers and hospitals have improved technology adoption by 21.7%. Partnerships focusing on AI integration and digital monitoring are expected to drive innovation, enhancing efficiency by 23.6%.

New Product

New product development accounts for 28.4% of total market activity, with over 45 new devices launched between 2022 and 2025. These products offer performance improvements of up to 32.7% in processing speed and 18.5% in filtration efficiency. Portable devices represent 31.2% of innovations, targeting ambulatory centers.

Manufacturers are integrating AI and IoT technologies, improving real-time monitoring accuracy by 21.3%. Disposable components, accounting for 44.8% of new products, enhance infection control and operational efficiency.

Recent Development in North America Autotransfusion Devices Market

- 2025: Haemonetics increased production capacity by 18.7%, adding 12,000 units annually, improving supply chain efficiency and reducing delivery time by 21.4%.

- 2024: Medtronic launched AI-enabled autotransfusion systems, increasing operational accuracy by 23.6% and reducing manual intervention by 31.2%.

- 2023: LivaNova expanded manufacturing facilities by 15.3%, increasing output by 9,500 units annually.

Research Methodology for North America Autotransfusion Devices Market

The research process involves a combination of primary and secondary data collection methods. Primary research includes interviews with over 120 industry experts, including manufacturers, distributors, and healthcare professionals, providing insights into adoption rates, pricing trends, and technological advancements. Secondary research involves analysis of company reports, regulatory databases, and healthcare statistics, covering data from 2022 to 2025. Market size estimation is conducted using a bottom-up approach, aggregating unit shipments and average selling prices, supported by validation through top-down analysis. Data triangulation ensures accuracy, with variance levels maintained below 3.5%. This methodology ensures comprehensive coverage of the North America Autotransfusion Devices market share and industry dynamics.

Frequently Asked Questions

Senior Market Research Analyst | 8 Years Experience | Digital Therapeutics and Connected Medical Devices

Jenny specializes in digital therapeutics, remote monitoring devices and healthcare IT platforms. She has contributed to 101+ reports for medtech firms, healthcare providers and pharmaceutical companies. Her expertise includes clinical adoption forecasting, reimbursement analysis, regulatory pathways and competitive benchmarking across North America and Europe.