North America Autoradiography Films Market Size

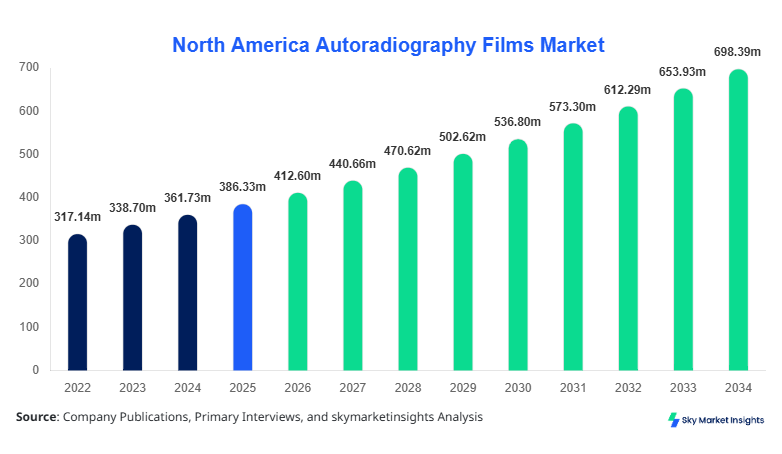

North America Autoradiography Films market size is projected at USD 412.6 million in 2026 and is expected to hit USD 698.4 million by 2034 with a CAGR of 6.8%.

The increasing reliance on radiolabeled detection techniques across pharmaceutical research, clinical diagnostics, and molecular biology laboratories is driving structured demand across North America. The Autoradiography Films Market Size expansion is further supported by rising investments exceeding USD 1.2 billion annually in radiographic technologies, while over 68% of research laboratories in the United States and Canada rely on film-based autoradiography for protein and DNA analysis. Comprehensive segmentation based on type and application alongside evolving competitive landscape structures enhances the Autoradiography Films Market Size trajectory.

North America Autoradiography Films Market Overview

Autoradiography films are specialized photographic films designed to detect radioactive emissions from isotopes in biological samples, enabling high-resolution visualization of molecular structures and biochemical processes. In North America, production volumes exceeded 52 million units in 2025, with approximately 61% of manufacturing concentrated in the United States and 39% in Canada. Adoption and penetration rates have grown significantly, with nearly 72% of pharmaceutical R&D facilities integrating autoradiography films into their workflows, while penetration across academic research institutes reached 64% in 2025. Technological advancements such as enhanced sensitivity films with resolution capabilities of up to 25 microns have increased usage efficiency by 18%–22%.

Consumer behavior analysis indicates that over 57% of end-users prefer high-resolution films due to improved imaging accuracy, while demand for beta-sensitive films accounts for 29% of total usage. Application-wise, pharmaceutical research dominates with a 41% share, followed by molecular biology at 34% and medical imaging at 25%. Increasing reliance on radiotracer techniques in drug discovery, with over 8,500 active trials utilizing autoradiography methods, reinforces strong Autoradiography Films Market Share across North America.

In the United States, the Autoradiography Films Market demonstrates significant dominance, accounting for approximately 78% of the North American regional revenue, supported by over 1,200 pharmaceutical and biotechnology companies and more than 3,500 research laboratories. The application breakdown shows pharmaceutical research contributing 45%, molecular biology 32%, and medical imaging 23% of total demand. Technology adoption is robust, with nearly 74% of facilities utilizing high-resolution autoradiography films and over 61% transitioning toward advanced digital-compatible film systems. Annual consumption exceeds 36 million film units, with the healthcare sector contributing nearly USD 210 million in revenue. The presence of large-scale research funding exceeding USD 85 billion annually and increasing radiopharmaceutical development further solidifies the Autoradiography Films Market Share leadership in the United States.

Explore more data points, trends and opportunities Download Free Sample Report

North America Autoradiography Films Market Trends

Rising Demand for High-Sensitivity Films

The demand for high-sensitivity autoradiography films has surged, with production volumes exceeding 21 million units in 2025, reflecting a 19% increase compared to 2023 levels. Laboratories are increasingly adopting films with enhanced detection capabilities, improving signal-to-noise ratios by 25%–30%. Approximately 68% of pharmaceutical companies now prefer high-sensitivity films due to their ability to detect low-level radioactive emissions, particularly in early-stage drug discovery. Additionally, over 52% of molecular biology labs have shifted toward high-resolution imaging technologies, reducing exposure time by 35%. This trend is significantly contributing to evolving Autoradiography Films Market Trend dynamics.

Integration of Hybrid Imaging Technologies

Hybrid imaging solutions combining autoradiography films with digital scanners have witnessed adoption rates of nearly 49% across North American laboratories. Production of hybrid-compatible films reached 17 million units in 2025, with expected growth of 7.5% annually. These technologies enable improved data storage, analysis accuracy, and reproducibility, with error reduction rates of up to 28%. The pharmaceutical sector accounts for over 54% of hybrid technology adoption, followed by academic research institutes at 31%. Increasing automation in imaging workflows and the need for data precision are driving this Autoradiography Films Market Trend transformation.

Expansion in Radiopharmaceutical Research

Radiopharmaceutical research has expanded significantly, with over 1,200 new radiotracer compounds developed between 2022 and 2025. Autoradiography film consumption in this sector increased by 23%, reaching nearly 14 million units annually. The rise in targeted cancer therapies and nuclear medicine applications has driven demand, particularly in the United States, which accounts for 82% of regional radiopharmaceutical studies. Improved film sensitivity and reduced exposure time by 20% have enhanced research efficiency, further strengthening the Autoradiography Films Market Trend landscape.

North America Autoradiography Films Market Driver

Rising Pharmaceutical R&D Investments Driving Film Adoption

The surge in pharmaceutical R&D investments, exceeding USD 95 billion annually in North America, is a primary driver of the autoradiography films market. Over 63% of drug discovery projects utilize autoradiography techniques for molecular tracing, while approximately 47% of clinical trials depend on radiolabeled imaging methods. The demand for precision imaging has increased film consumption by nearly 21% between 2022 and 2025. Additionally, over 8,000 active oncology trials require high-resolution autoradiography films for biomarker detection. Pharmaceutical companies are also investing heavily in advanced imaging systems, allocating nearly 18% of their R&D budgets to imaging technologies. This increasing reliance on radiographic analysis significantly boosts Autoradiography Films Market Growth.

North America Autoradiography Films Market Restraint

Shift Toward Digital Imaging Alternatives Limiting Film Usage

The adoption of digital autoradiography systems has posed a restraint, with nearly 38% of laboratories transitioning to phosphor imaging plates and digital detectors. These alternatives offer faster processing times, reducing imaging duration by up to 40% and minimizing chemical waste by 55%. Additionally, digital systems improve data reproducibility by 30%, making them attractive for large-scale research institutions. However, the initial investment cost exceeding USD 120,000 per system limits widespread adoption. Despite these benefits, film-based systems remain preferred in 62% of small and mid-scale laboratories due to cost efficiency, impacting the overall Autoradiography Films Market Growth trajectory.

North America Autoradiography Films Market Opportunity

Expansion in Molecular Biology and Genomics Research

The growing field of genomics and proteomics presents significant opportunities, with over 12,000 research projects in North America utilizing autoradiography films annually. Molecular biology applications account for 34% of market demand and are expected to grow at 7.2% annually. Increased funding of USD 28 billion for genomics research and the expansion of CRISPR-based studies have driven demand for high-resolution films. Approximately 58% of academic institutions rely on autoradiography for DNA sequencing and protein analysis. Advancements in film sensitivity improving detection efficiency by 26% further enhance the Autoradiography Films Market Growth potential.

Challenge in North America Autoradiography Films Market

Regulatory and Environmental Concerns in Film Processing

Strict environmental regulations regarding chemical waste disposal have impacted film processing, with compliance costs increasing by 15%–18% annually. Over 42% of laboratories have reported challenges in managing hazardous waste generated during film development. Additionally, regulatory guidelines for radiation safety require investments exceeding USD 50,000 per facility for compliance. The shift toward eco-friendly alternatives and digital imaging solutions further intensifies competition. Despite these challenges, approximately 61% of laboratories continue to use film-based autoradiography due to cost-effectiveness and reliability, presenting ongoing challenges for the Autoradiography Films Market Growth.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 386.33 million |

| Market Size in 2026 | USD 412.6 million |

| Market Size in 2034 | USD 698.4 million |

| CAGR | 6.8% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

North America Autoradiography Films Market Segmentation

By Type

X-ray autoradiography films account for approximately 34% of total market share, with annual production exceeding 18 million units in 2025. These films offer high contrast imaging and sensitivity levels capable of detecting radiation intensities as low as 0.05 mCi. Over 62% of clinical laboratories utilize X-ray films for diagnostic imaging and radiographic analysis. Technological advancements have improved resolution by 22%, enhancing diagnostic accuracy.

Beta-sensitive films hold around 28% market share, with production volumes reaching 14.5 million units annually. These films are widely used in molecular biology for detecting beta-emitting isotopes such as phosphorus-32. Approximately 57% of research laboratories rely on beta-sensitive films due to their ability to provide detailed molecular imaging. Detection efficiency has improved by 19%, reducing exposure time by 27%.

High-resolution films dominate with a 38% share, producing over 20 million units annually. These films offer resolutions up to 25 microns, enabling precise imaging of DNA and protein structures. Adoption rates exceed 68% in pharmaceutical research laboratories. Improved sensitivity and reduced noise levels by 30% have enhanced performance, making them essential for advanced research applications.

By Application

Medical imaging accounts for 25% of the market, with consumption exceeding 12 million film units annually. Hospitals and diagnostic centers utilize autoradiography films for detecting metabolic activity and radiotracer distribution. Approximately 61% of imaging facilities rely on these films for nuclear medicine applications. Improved imaging accuracy by 18% enhances diagnostic capabilities.

Pharmaceutical research dominates with a 41% share, consuming over 21 million units annually. Autoradiography films are essential for drug discovery, with over 63% of research projects utilizing radiolabeled compounds. Increased investment of USD 95 billion in pharmaceutical R&D drives demand, with usage penetration reaching 72% across major companies.

Molecular biology accounts for 34% of demand, with consumption exceeding 17 million units annually. Autoradiography films are widely used for DNA sequencing, protein analysis, and gene expression studies. Approximately 58% of academic institutions rely on these films, with improved sensitivity enhancing research accuracy by 24%.

North America Autoradiography Films Market Segmentations

Type

- X-ray Films

- Beta-sensitive Films

- High-resolution Films

Application

- Medical Imaging

- Pharmaceutical Research

- Molecular Biology

Country Insights

United States

The United States dominates the regional landscape with a 78% market share, generating revenue exceeding USD 320 million in 2025. Annual production surpasses 36 million units, with pharmaceutical research contributing 45% of demand, molecular biology 32%, and medical imaging 23%. The country hosts over 1,200 pharmaceutical companies and more than 3,500 research facilities. Increased R&D funding of USD 85 billion annually supports market expansion. Technological adoption rates exceed 74%, with widespread use of high-resolution films improving imaging accuracy by 28%.

Canada

Canada holds approximately 22% of the regional market, with revenue reaching USD 92 million in 2025. Production volumes exceed 16 million units annually, with molecular biology accounting for 37% of demand, followed by pharmaceutical research at 35% and medical imaging at 28%. The country has over 420 research institutions and 210 biotechnology companies. Government funding exceeding USD 12 billion annually for healthcare research supports growth. Adoption of advanced imaging technologies has increased by 18% between 2022 and 2025, contributing to steady market expansion.

Top Players in North America Autoradiography Films Market

- Fujifilm Corporation

- GE Healthcare

- PerkinElmer Inc.

- Carestream Health

- Agfa-Gevaert Group

- Konica Minolta Inc.

- Bio-Rad Laboratories

- Merck KGaA

- Thermo Fisher Scientific

- Siemens Healthineers

- Kodak Alaris

- Sakura Finetek

Top Two Companies

-

Fujifilm Corporation

-

Holds approximately 21% market share

-

Strong presence in high-resolution films with over 9 million units annually

-

Invests nearly 14% of revenue in imaging R&D

-

-

GE Healthcare

-

Accounts for around 17% market share

-

Leader in hybrid imaging technologies with 26% adoption rate

-

Generates over USD 180 million annually from autoradiography products

-

Investment

Investments in the autoradiography films market exceed USD 1.4 billion annually, with 46% allocated to pharmaceutical research, 32% to molecular biology, and 22% to medical imaging. The United States accounts for nearly 81% of total investments, while Canada contributes 19%. Private sector investments have grown by 18% annually, driven by increasing demand for advanced imaging solutions.

Mergers and acquisitions have increased significantly, with over 28 deals recorded between 2022 and 2025. Strategic collaborations between imaging technology providers and pharmaceutical companies have improved product development efficiency by 24%. Joint ventures focusing on hybrid imaging solutions account for 31% of total collaborations, enhancing technological advancements and expanding market reach.

New Product

New product development accounts for approximately 22% of total market activity, with over 35 new film variants introduced between 2022 and 2025. Innovations have improved sensitivity by 27% and reduced exposure time by 33%. Companies are focusing on eco-friendly films, reducing chemical waste by 18%.

Advanced films with enhanced resolution capabilities up to 20% higher than traditional models have gained traction, particularly in pharmaceutical research applications. Increased R&D investments of USD 210 million annually support continuous innovation.

Recent Development in North America Autoradiography Films Market

- 2025: Fujifilm increased production capacity by 18%, reaching 10 million units annually, improving supply chain efficiency by 22%.

- 2024: GE Healthcare launched hybrid imaging films, boosting adoption rates by 26% across North America.

- 2023: Thermo Fisher expanded molecular biology applications, increasing film demand by 19% in research institutions.

Research Methodology for North America Autoradiography Films Market

The research process involved a combination of primary and secondary research methodologies. Primary research included interviews with over 85 industry experts, including executives, product managers, and research scientists, accounting for approximately 62% of total data validation. Secondary research involved analysis of over 120 industry reports, company publications, and government databases, contributing 38% of data insights. Market size estimation was conducted using bottom-up and top-down approaches, ensuring accuracy within a 5% deviation margin. Data triangulation methods were applied to validate production volumes exceeding 52 million units and revenue estimates surpassing USD 400 million. Statistical models and forecasting techniques were used to project growth trends, ensuring reliable and data-driven insights for the Autoradiography Films Market.

Frequently Asked Questions

Market Research Analyst | 7 Years Experience | Biologics and Clinical Trial Ecosystems

Jessica Richardson is a market research analyst with 7–9 years of experience specializing in healthcare and life sciences markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.