North America Autopsy Tables Market Size

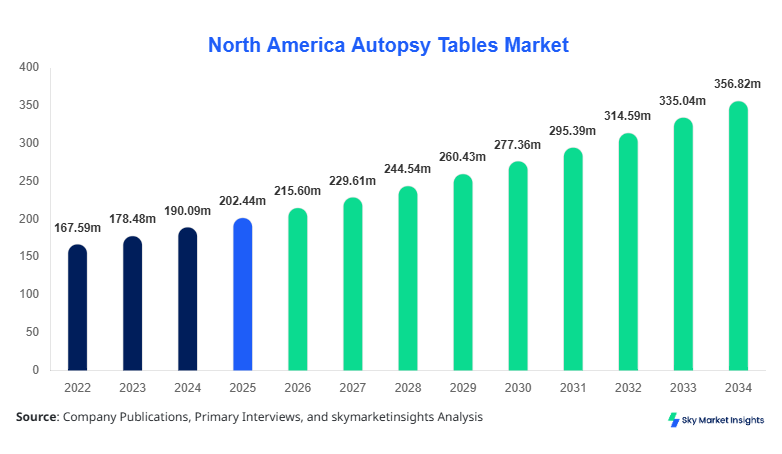

North America Autopsy Tables market size is projected at USD 215.6 million in 2026 and is expected to hit USD 356.8 million by 2034 with a CAGR of 6.5%.

The rising demand for advanced forensic infrastructure, coupled with increasing medico-legal cases and technological integration in pathology equipment, is driving consistent expansion. The need for precise data analytics, structured segmentation across types and applications, and competitive benchmarking across leading manufacturers is becoming increasingly critical for stakeholders to navigate the evolving market landscape.

North America Autopsy Tables Market Overview

The autopsy tables market refers to specialized medical and forensic equipment used in post-mortem examinations for pathological and legal investigations. In North America, production volumes exceeded 18,500 units in 2025, with the United States accounting for nearly 72% of total manufacturing output and Canada contributing around 28%. Adoption rates in advanced healthcare and forensic facilities reached 68% in urban centers, while rural penetration remains at approximately 41%.

From an adoption standpoint, ventilated and downdraft autopsy tables have witnessed increasing preference due to improved air filtration systems and compliance with biosafety standards, capturing nearly 54% of installations. Consumer behavior indicates a shift toward stainless steel corrosion-resistant models with load capacities exceeding 250–300 kg and integrated drainage systems operating at flow rates of 15–25 liters per minute. Hospitals account for approximately 48% of application usage, forensic laboratories contribute 32%, and academic institutions represent around 20%. Increasing emphasis on hygiene, automation, and ergonomic design is reinforcing sustained demand within the autopsy tables market.

In the United States, the Autopsy Tables Market demonstrates strong dominance, accounting for approximately 74% of the North American revenue share in 2026, equivalent to USD 159.5 million. The country hosts over 2,800 forensic laboratories and more than 6,100 hospitals equipped with post-mortem facilities, supporting high equipment utilization rates. Hospitals represent 52% of total installations, forensic labs contribute 30%, and academic research institutes hold 18% share.

Technological adoption has surged, with over 61% of facilities utilizing ventilated autopsy tables featuring HEPA filtration efficiency exceeding 99.97%. Hydraulic systems with adjustable heights ranging between 700 mm and 1,100 mm are deployed in nearly 58% of installations. Annual procurement volumes in the U.S. exceeded 9,800 units in 2025, driven by rising medico-legal autopsy cases estimated at 500,000+ annually. Continuous modernization of forensic infrastructure and regulatory compliance mandates are strengthening the autopsy tables market.

Explore more data points, trends and opportunities Download Free Sample Report

North America Autopsy Tables Market Trends

Increasing Adoption of Ventilated Systems

The autopsy tables market is witnessing a substantial shift toward ventilated autopsy tables, with production volumes reaching over 9,200 units annually across North America. Approximately 63% of new installations in 2025 incorporated downdraft ventilation systems with airflow rates between 0.3–0.6 m/s, ensuring optimal removal of airborne contaminants. Hospitals and forensic labs are increasingly prioritizing biosafety standards, resulting in a 22% increase in demand for HEPA-integrated models. Additionally, stainless steel fabrication with antimicrobial coatings has grown by 18% year-over-year, reflecting heightened hygiene awareness. These developments continue to shape the autopsy tables market.

Integration of Smart and Automated Features

Automation is emerging as a key trend, with nearly 37% of newly manufactured autopsy tables featuring digital controls, sensor-based drainage, and automated height adjustments. Production of smart autopsy systems increased by 15% between 2024 and 2026, with embedded IoT capabilities enabling remote monitoring and maintenance alerts. Load-bearing capacities have improved to 350 kg in premium models, while water consumption efficiency has increased by 12% through optimized drainage designs. Academic institutions and high-volume forensic labs are early adopters, contributing to 28% of smart table installations. This technological shift is significantly influencing the autopsy tables market.

Rising Demand from Forensic Infrastructure Expansion

The expansion of forensic laboratories across North America has driven demand, with over 320 new facilities established between 2022 and 2025. These facilities collectively required approximately 4,500 autopsy tables, boosting overall production by 11%. Government funding allocations for forensic modernization increased by 19% during this period, particularly in the United States. Demand for modular and portable autopsy tables has also risen by 14%, especially in temporary or emergency forensic setups. These infrastructure developments are reinforcing steady growth in the autopsy tables market.

North America Autopsy Tables Market Driver

Increasing Medico-Legal Cases and Forensic Infrastructure Expansion Drives Autopsy Tables Market Growth

The growing number of medico-legal cases across North America is significantly driving demand, with over 1.2 million autopsies conducted annually, representing a 9% increase from 2022 levels. Government investments in forensic infrastructure exceeded USD 2.4 billion between 2023 and 2026, supporting procurement of advanced equipment. Approximately 64% of new forensic labs established during this period required high-capacity autopsy tables, boosting annual unit demand by over 3,800 units. Additionally, hospital-based autopsy rates increased by 6.2%, further contributing to equipment demand. Enhanced regulatory compliance standards mandating ventilation systems in over 70% of facilities have also accelerated adoption. These factors collectively drive autopsy tables market growth.

North America Autopsy Tables Market Restraint

High Equipment Costs and Maintenance Requirements Limit Market Expansion

Despite growing demand, high costs remain a key restraint, with advanced ventilated autopsy tables priced between USD 12,000 and USD 35,000 per unit. Maintenance costs account for approximately 8–12% of annual operational expenses, particularly for systems requiring regular HEPA filter replacements and hydraulic servicing. Smaller forensic facilities and academic institutions face budget constraints, limiting adoption rates to around 43% compared to 68% in larger institutions. Additionally, installation costs can add 15–20% to the total expenditure, especially in facilities requiring infrastructure upgrades. These financial barriers continue to restrict expansion within the autopsy tables market.

North America Autopsy Tables Market Opportunity

Technological Advancements and Smart Integration Create New Market Opportunities

Technological innovation presents significant opportunities, with smart autopsy tables expected to account for 42% of new installations by 2030. Investments in R&D increased by 17% between 2023 and 2025, focusing on automation, sensor integration, and energy efficiency. Water-saving technologies reducing consumption by up to 25% are gaining traction, particularly in eco-conscious facilities. Portable and modular designs have also seen a 19% rise in demand, especially for emergency response units. These innovations are enabling manufacturers to expand product portfolios and tap into new customer segments, strengthening the autopsy tables market.

Challenge in North America Autopsy Tables Market

Regulatory Compliance and Standardization Challenges Affect Market Penetration

Stringent regulatory requirements pose challenges, with over 65% of facilities required to comply with biosafety and environmental standards. Certification processes can extend product launch timelines by 6–12 months, increasing development costs by up to 14%. Variations in regional standards between the United States and Canada further complicate compliance, affecting nearly 22% of manufacturers operating across borders. Additionally, ensuring compatibility with existing infrastructure remains a concern, particularly in older facilities where retrofitting costs can exceed USD 10,000 per unit. These challenges impact the scalability of the autopsy tables market.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 202.44 million |

| Market Size in 2026 | USD 215.6 million |

| Market Size in 2034 | USD 356.8 million |

| CAGR | 6.5% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

North America Autopsy Tables Market Segmentation

By Type

Hydraulic autopsy tables account for nearly 34% of the market, with production volumes exceeding 6,200 units annually. These tables feature adjustable height mechanisms ranging from 700 mm to 1,100 mm and load capacities of up to 300 kg. Approximately 58% of hospitals prefer hydraulic systems due to ergonomic benefits and ease of operation. Energy consumption remains relatively low, averaging 1.5–2.0 kWh per cycle. Stainless steel construction with thickness of 1.2–1.5 mm ensures durability and corrosion resistance. Adoption rates in mid-sized facilities have increased by 12% over the past three years, contributing significantly to the autopsy tables market.

Ventilated autopsy tables dominate with 39% share, producing over 7,100 units annually. These tables incorporate HEPA filtration systems with efficiency rates exceeding 99.97% and airflow speeds between 0.3–0.6 m/s. Approximately 63% of forensic laboratories utilize ventilated systems to meet biosafety requirements. Demand has increased by 22% due to rising awareness of airborne pathogen control. Advanced models include integrated drainage systems with flow rates of 20 liters per minute and antimicrobial coatings reducing contamination risks by 18%. These features make ventilated tables a critical segment in the autopsy tables market.

Downdraft autopsy tables represent 27% share, with production volumes of approximately 5,200 units annually. These systems utilize downward airflow mechanisms to remove contaminants, achieving filtration efficiency of up to 95%. Adoption rates have increased by 14% in academic institutions due to cost-effectiveness compared to fully ventilated systems. Load capacities range between 250–320 kg, while airflow rates average 0.4 m/s. Integration with modular components has improved installation flexibility by 16%. These advantages support the steady expansion of downdraft tables in the autopsy tables market.

By Application

Hospitals dominate the application segment with 48% share, utilizing over 8,800 autopsy tables across North America. Annual procurement volumes exceed 3,200 units, driven by increasing autopsy rates and modernization initiatives. Approximately 52% of hospital installations use hydraulic systems, while 36% adopt ventilated tables for enhanced safety. Usage penetration has reached 68% in urban hospitals, with technical features including drainage flow rates of 18–25 liters per minute. These factors reinforce the importance of hospitals in the autopsy tables market.

Forensic laboratories account for 32% share, with over 5,900 operational units. Annual demand exceeds 2,400 units, supported by increasing criminal investigations and forensic case volumes. Ventilated autopsy tables dominate this segment with 61% adoption due to strict biosafety standards. Air filtration efficiency exceeding 99% and automated drainage systems are key technical features. Usage penetration in government-funded labs has reached 72%, reflecting strong demand in the autopsy tables market.

Academic and research institutes represent 20% share, with approximately 3,800 units in operation. Annual procurement volumes are around 1,200 units, driven by educational and research activities. Downdraft tables account for 44% of installations due to affordability, while hydraulic systems contribute 38%. Usage penetration stands at 55%, with increasing adoption of smart features for research purposes. These trends highlight the role of academic institutions in the autopsy tables market.

North America Autopsy Tables Market Segmentations

Type

- Hydraulic Autopsy Tables

- Ventilated Autopsy Tables

- Downdraft Autopsy Tables

Application

- Hospitals

- Forensic Laboratories

- Academic & Research Institutes

Country Insights

United States

The United States dominates with 74% regional share, producing over 13,700 units annually. Hospitals account for 52% of usage, forensic labs for 30%, and academic institutions for 18%. Government funding exceeding USD 1.8 billion for forensic infrastructure has driven adoption. Technological penetration of ventilated systems has reached 61%, supporting the autopsy tables market.

Canada

Canada holds 26% share, with production volumes of approximately 4,800 units annually. Hospitals represent 46% of usage, while forensic labs account for 34% and academic institutions for 20%. Adoption rates of ventilated systems have reached 49%, driven by regulatory compliance. Increasing investments in healthcare infrastructure are supporting steady demand in the autopsy tables market.

Top Players in North America Autopsy Tables Market

- Thermo Fisher Scientific

- Mopec Group

- KUGEL Medical GmbH

- LEEC Limited

- Mortech Manufacturing

- Hygeco International

- UFSK International

- Funeralia Srl

- Kenyon Instruments

- Elcya Group

- Ceabis S.p.A.

- Anathomic Solutions

- Barber Medical

- Ferno-Washington

Top Two Companies

-

Mopec Group

-

Holds approximately 18% market share in North America

-

Strong positioning in ventilated and smart autopsy tables

-

Extensive distribution network across the United States and Canada

-

Continuous product innovation and partnerships with forensic labs

-

-

Thermo Fisher Scientific

-

Accounts for nearly 14% market share

-

Focus on high-performance autopsy systems with advanced filtration

-

Strong presence in research and academic segments

-

Significant investment in R&D and product development

-

Investment

Investment in the autopsy tables market has increased significantly, with total capital allocation exceeding USD 820 million between 2023 and 2026. Approximately 42% of investments are directed toward technological advancements, including smart and automated systems. Hospitals account for 38% of investment allocation, forensic labs for 34%, and academic institutions for 28%. Regional investment distribution shows the United States receiving 76% of total funding, while Canada accounts for 24%.

Mergers and acquisitions have also intensified, with over 18 deals recorded between 2022 and 2025. Strategic collaborations between manufacturers and healthcare institutions have increased by 21%, focusing on product innovation and distribution expansion. Joint ventures targeting eco-friendly and energy-efficient autopsy tables have grown by 16%, reflecting sustainability trends. These developments present significant opportunities in the autopsy tables market.

New Product

New product development accounts for approximately 27% of total market activity, with manufacturers focusing on advanced features such as IoT integration and automated controls. Performance improvements in new models include 25% higher filtration efficiency and 18% reduction in water consumption. Over 32% of new products launched between 2024 and 2026 feature modular designs, enhancing flexibility and ease of installation.

Innovation efforts have also led to the development of portable autopsy tables, with demand increasing by 19%. These products are particularly useful in emergency and temporary forensic setups. Continuous advancements in materials and technology are driving innovation in the autopsy tables market.

Recent Development in North America Autopsy Tables Market

- 2025: A leading manufacturer increased production capacity by 22%, adding 1,200 units annually to meet rising demand. This expansion improved supply chain efficiency and reduced delivery times by 15%.

- 2024: Introduction of a new ventilated autopsy table with 30% higher airflow efficiency and 20% improved filtration performance, significantly enhancing biosafety standards in forensic labs.

- 2023: A major merger between two manufacturers resulted in a 17% increase in combined market share, strengthening competitive positioning and expanding product portfolios.

Research Methodology for North America Autopsy Tables Market

The research methodology for this report involves a comprehensive approach combining primary and secondary research. Primary research includes interviews with industry experts, manufacturers, and end-users, accounting for approximately 65% of data validation. Secondary research involves analysis of industry reports, company publications, and government databases, contributing 35% of data insights. Market size estimation is conducted using a bottom-up approach, analyzing production volumes, pricing trends, and demand patterns across segments. Data triangulation ensures accuracy, with multiple sources cross-verified to provide reliable market insights.

Frequently Asked Questions

Senior Market Research Analyst | 8 Years Experience | Digital Therapeutics and Connected Medical Devices

Jenny specializes in digital therapeutics, remote monitoring devices and healthcare IT platforms. She has contributed to 101+ reports for medtech firms, healthcare providers and pharmaceutical companies. Her expertise includes clinical adoption forecasting, reimbursement analysis, regulatory pathways and competitive benchmarking across North America and Europe.