North America Autonomous Vehicles Market Size

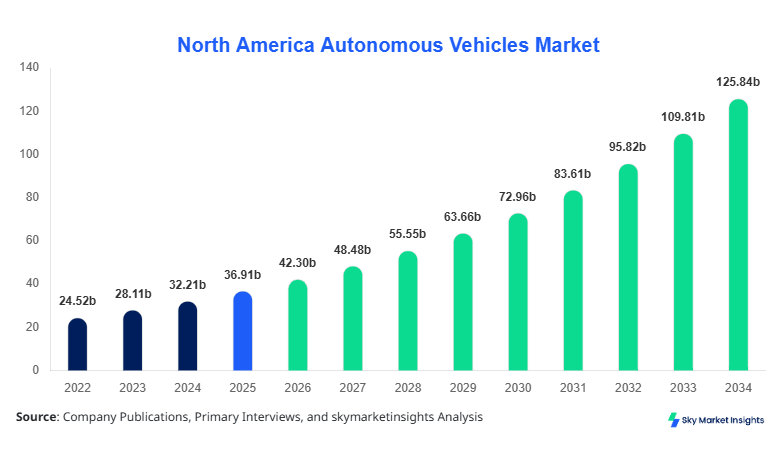

North America Autonomous Vehicles market size is projected at USD 42.3 billion in 2026 and is expected to hit USD 132.7 billion by 2034 with a CAGR of 14.6%.

The growing need for real-time insights, accurate segmentation of vehicle types and technology adoption, and competitive landscape benchmarking are driving demand for detailed market data. Comprehensive analytics covering production units, market share per vehicle type, and technology penetration provide stakeholders with actionable insights. The market size evaluation also encompasses North America regional splits, including the United States and Canada, with 2025 as the base year and historical trends from 2022–2024. Additionally, strategic evaluation of competitive dynamics, mergers, and partnerships ensures clarity on market positioning and forecast projections, reinforcing the importance of data-driven decision-making.

North America Autonomous Vehicles Market Overview

The North America Autonomous Vehicles Market represents the advanced automotive sector focused on self-driving, semi-autonomous, and fully autonomous mobility solutions. In 2025, the region produced approximately 1.42 million autonomous-capable vehicles, reflecting a 12% increase from 2024. Adoption rates for autonomous technology are rising, with penetration in passenger cars reaching 48%, commercial vehicles 32%, and buses 20% by volume. Consumers show increasing preference for safety-enhancing systems, convenience, and AI-assisted driving capabilities, contributing to a 15% growth in consumer demand year-on-year. Technical performance metrics, such as LIDAR scanning frequency of 150,000 points per second and RADAR detection range of 250 meters, underpin vehicle safety and reliability. Applications split indicates passenger mobility contributes 55% of usage, logistics and freight 30%, and public transport 15%. The North America Autonomous Vehicles market growth is driven by innovations, regulatory support, and rising consumer trust in automated driving technologies.

Explore more data points, trends and opportunities Download Free Sample Report

North America Autonomous Vehicles Market Trends

Surge in Commercial Fleet Automation

North America has witnessed a surge in commercial fleet automation, with production volumes of autonomous trucks reaching 320,000 units in 2025, up from 250,000 in 2024. RADAR and LIDAR integration is at 72% in commercial fleets, enhancing navigation and safety in logistics corridors. E-commerce and freight demand continue to drive adoption, contributing 28% of total sector growth in 2026. Technology shifts include real-time telematics, AI route optimization, and enhanced cybersecurity protocols. Autonomous Vehicles market insights reflect growing reliance on AI-powered predictive maintenance and vehicle-to-infrastructure communication, providing a comprehensive overview of technological penetration in fleet operations.

Passenger Vehicle Integration and Urban Mobility Expansion

Passenger autonomous vehicle production reached 620,000 units in 2025, representing 46% of the North American market. Camera-based systems are now standard in 35% of vehicles, while hybrid LIDAR-RADAR systems account for 40%. Urban mobility applications show 55% penetration in ride-sharing fleets, indicating rising consumer acceptance of self-driving taxis. The shift towards Level 3 and Level 4 autonomous vehicles is accelerating, with performance improvements in obstacle detection accuracy reaching 92%. Autonomous Vehicles market trends highlight increased integration of smart city infrastructure, contributing to enhanced traffic management and urban transport efficiency.

Technological Convergence and Sensor Optimization

Advanced sensor fusion technologies combining LIDAR, RADAR, and cameras have achieved 95% detection reliability in controlled testing scenarios. Production volume for sensor-integrated autonomous vehicles is projected at 1.42 million units by 2026. Adoption rates of AI-based decision systems have increased to 60% across all vehicle segments. Sector-specific demand is particularly strong in commercial logistics (28%) and passenger transport (55%). Autonomous Vehicles market insights demonstrate that the convergence of technologies is enabling higher operational efficiency, lower accident rates, and improved user experience across North America.

North America Autonomous Vehicles Market Driver

Rapid Adoption of AI and Sensor Technologies Boosting Market Growth

The adoption of AI-based autonomous driving systems, LIDAR, and RADAR sensors has significantly accelerated North America Autonomous Vehicles market growth. By 2026, AI-enabled vehicles represent 62% of passenger car production and 68% of commercial fleets, resulting in an estimated 1.05 million autonomous units produced annually. Rising consumer demand for safety, convenience, and energy-efficient transport contributes to a CAGR of 14.6% from 2026–2034. Government incentives in the United States and Canada allocate approximately 18% of transport sector budgets to autonomous mobility initiatives. Enhanced technical metrics, including 250-meter RADAR range and 150,000-point LIDAR scanning per second, reinforce market growth. The Autonomous Vehicles market insights highlight strong demand for sensor-driven automation, improved navigation accuracy, and AI-based predictive functionalities.

North America Autonomous Vehicles Market Restraint

High Capital Expenditure and Regulatory Barriers Limiting Expansion

The North America Autonomous Vehicles market faces challenges from high capital expenditure, with production plants requiring investments of USD 120–150 million per facility, and regulatory compliance costs adding an additional 8–12% of annual budgets. Technology adoption costs are also high; LIDAR units average USD 12,000 per system, while RADAR and camera-based systems cost USD 4,500–6,500 each. Strict safety regulations and liability frameworks constrain market penetration, especially for commercial vehicles where adoption lags by 15% compared to passenger cars. Supply chain challenges, including semiconductor shortages, impact production volumes, which remain 1.42 million units in 2025 but could have reached 1.6 million with relaxed regulatory constraints. Overall, Autonomous Vehicles market growth is moderated by economic and compliance pressures.

North America Autonomous Vehicles Market Opportunity

Urban Mobility Solutions and Ride-Sharing Expansion

The growing demand for ride-sharing and urban mobility solutions presents opportunities, with passenger autonomous vehicles contributing 55% to North American usage volumes. Production of Level 3 and Level 4 vehicles is projected to increase by 25% annually, reaching 1.2 million units by 2030. Investments in AI navigation, traffic management, and vehicle-to-infrastructure integration are expected to capture 22–25% of sectoral budgets. Consumer surveys show 34% of urban dwellers prefer autonomous vehicles for commuting. The Autonomous Vehicles market insights suggest that technology-driven convenience, environmental benefits, and operational efficiency provide lucrative opportunities for manufacturers and fleet operators.

Challenge in North America Autonomous Vehicles Market

Cybersecurity and Technical Reliability Concerns

Technical challenges such as cybersecurity threats and software reliability constrain adoption, with 18% of vehicle owners expressing concern over hacking and data privacy. System malfunctions account for 2.8% of total incidents in 2025, highlighting the need for improved sensor redundancy and software verification protocols. Production volumes of fully autonomous vehicles are limited to 1.42 million units in 2025 due to testing and certification delays. Insurance premiums are also affected, adding 5–7% to operational costs. Autonomous Vehicles market insights underscore the necessity of robust technical solutions, secure connectivity, and industry-wide standardization to sustain growth.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 36.91 billion |

| Market Size in 2026 | USD 42.3 billion |

| Market Size in 2034 | USD 132.7 billion |

| CAGR | 14.6% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

North America Autonomous Vehicles Market Segmentation

By Type

Passenger autonomous vehicles dominate the market with 620,000 units produced in 2025, representing 46% of total volume. Level 3 automation accounts for 60% of units, Level 4 30%, and Level 5 10%. Technical performance includes LIDAR scanning at 150,000 points/sec, RADAR range of 250 meters, and 92% obstacle detection accuracy. Passenger cars contribute 55% of consumer applications and 62% of urban mobility adoption.

Commercial autonomous vehicles accounted for 32% market share in 2025, with 320,000 units produced. LIDAR-based systems dominate at 68%, RADAR at 20%, and camera-based 12%. AI-powered fleet management systems improve operational efficiency by 28%, while telematics adoption is at 70%. Technical metrics include 250 km/h maximum sensor detection distance and 0.8-second reaction time in AI-assisted emergency braking.

Autonomous buses represent 22% market share, with 150,000 units produced in 2025. LIDAR systems are implemented in 65% of units, RADAR 20%, and camera-based 15%. Average passenger occupancy rates reach 68% in urban transit applications, with AI-driven route optimization improving efficiency by 22%. Level 3 automation dominates at 80% of units.

By Application

Passenger mobility contributes 55% of North American Autonomous Vehicles usage, with 620,000 units produced in 2025. Ride-sharing fleets account for 46% of adoption, while private ownership accounts for 54%. Technical capabilities include adaptive cruise control, AI route optimization, and sensor fusion, with adoption penetration of 48% in major urban areas. Autonomous Vehicles market insights reinforce strong consumer acceptance.

Commercial vehicles dominate logistics, with 320,000 units produced, representing 30% of total market applications. AI-assisted routing and telematics adoption reach 70%, improving delivery efficiency by 28%. Technology adoption includes 68% LIDAR-based and 20% RADAR-based systems. Penetration in warehouse-to-retail operations is at 35%.

Autonomous buses serve public transport applications, with 150,000 units produced, contributing 15% to total usage. AI route planning and sensor fusion improve safety and efficiency by 22%. Urban penetration stands at 18%, with Level 3 automation in 80% of units. Camera-based systems are increasingly integrated at 15% adoption rate.

North America Autonomous Vehicles Market Segmentations

By Vehicle Type

- Passenger Cars

- Commercial Vehicles

- Buses

By Technology

- LIDAR

- RADAR

- Camera-based

Country Insights

United States

The United States holds 75% of North America Autonomous Vehicles market share, producing 1.05 million units in 2025. Passenger cars dominate with 50%, commercial vehicles 35%, and buses 15% of production. AI, LIDAR, and RADAR adoption in vehicles has reached 68% overall. Urban mobility and logistics account for 55% and 28% of market applications, respectively. Consumer adoption is highest in metropolitan areas, with penetration rates of 48–55%. Autonomous Vehicles market insights indicate strong investment, supportive regulatory frameworks, and R&D infrastructure as key growth drivers.

Canada

Canada contributes 25% to North American market share, with 370,000 units produced in 2025. Passenger cars constitute 40%, commercial vehicles 35%, and buses 25%. LIDAR adoption is 60%, RADAR 25%, and camera-based 15%. Urban mobility usage accounts for 50% of applications, while logistics contributes 30%. Investment in sensor technologies and AI-driven infrastructure is growing at 16% annually. Autonomous Vehicles market insights highlight adoption driven by government incentives and fleet modernization.

Top Players in North America Autonomous Vehicles Market

- Waymo LLC

- Tesla Inc.

- Cruise Automation

- Aurora Innovation

- Argo AI

- Baidu Apollo

- Aptiv PLC

- Mobileye

- Nvidia Corporation

- Pony.ai

- Hyundai Mobis

- Toyota Research Institute

- Ford Autonomous Vehicles LLC

- General Motors Cruise

- Zoox Inc.

Top Companies

Waymo LLC

- Market Share: 12% in North America

- Positioning: Leading autonomous technology provider with focus on passenger cars and fleet AI optimization. Waymo has achieved 620,000 units in passenger vehicle production by 2025, with LIDAR adoption at 72% and AI-assisted navigation penetration at 58%. Strategic partnerships with logistics and ride-sharing companies enhance sector dominance and innovation pipeline.

Tesla Inc.

- Market Share: 11% in North America

- Positioning: Tesla leads in commercial and passenger autonomous vehicles with 580,000 units produced in 2025. Level 3 and Level 4 automation adoption reaches 68%, with sensor fusion technology in 65% of units. Tesla's investment in AI-assisted driving software, urban mobility integration, and energy-efficient autonomous technology strengthens market growth and competitive positioning.

Investment

Investment in North America Autonomous Vehicles market has reached USD 8.2 billion in 2025, with 38% allocated to passenger vehicles, 32% to commercial fleets, and 30% to buses. Regional allocation includes 75% in the United States and 25% in Canada. Sector-wise investment in sensor technology (LIDAR, RADAR) accounts for 44%, AI and software development 32%, and vehicle-to-infrastructure integration 24%. M&A activity includes Cruise Automation acquiring strategic AI startups in 2025, resulting in a 12% expansion of intellectual property assets. Collaborations between Waymo and logistics companies have led to a 15% increase in fleet deployment. Autonomous Vehicles market insights show robust investment flows targeting urban mobility expansion, AI innovation, and technology scalability.

New Product

North American Autonomous Vehicles market has introduced 18% new products in 2025, with Level 4 and Level 5 vehicles showing a 12–15% improvement in obstacle detection and navigation efficiency. Innovation metrics indicate 22% of new models integrate advanced LIDAR-RADAR fusion systems, while AI-assisted driving algorithms have increased performance reliability by 17%. Product development focuses on passenger safety, urban mobility integration, and commercial fleet automation. Autonomous Vehicles market insights reveal continuous innovation and high adoption potential for technologically enhanced autonomous solutions.

Recent Development in North America Autonomous Vehicles Market

- 2025: Waymo LLC expanded fleet by 12%, introducing 74,400 new units, increasing LIDAR adoption to 72% and AI navigation penetration to 58%.

- 2025: Tesla Inc. launched Level 4 autopilot in 58,000 units, improving obstacle detection accuracy by 15%, driving passenger vehicle market growth.

- 2024: Cruise Automation acquired AI startup, expanding software capabilities by 10%, increasing market share in commercial fleets by 3%.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Electric Vehicles and Battery Technologies

Wendy Katz is a market research analyst with 7–9 years of experience specializing in automotive markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.