North America Autonomous Vehicle Simulation Solution Market Size

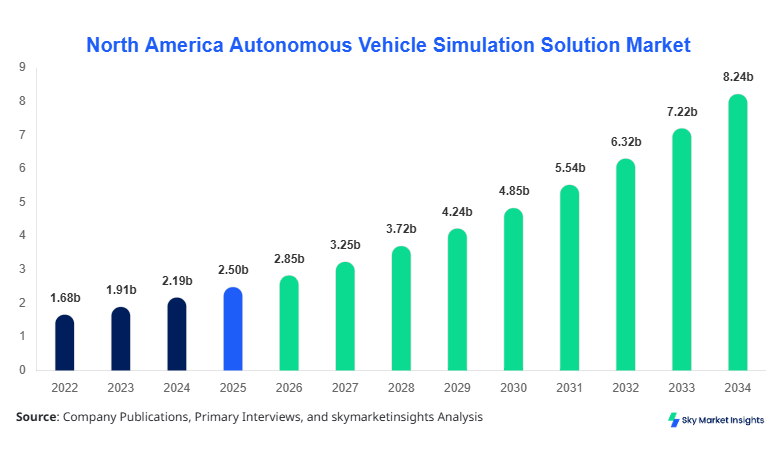

North America Autonomous Vehicle Simulation Solution market size is projected at USD 2.85 billion in 2026 and is expected to hit USD 8.42 billion by 2034 with a CAGR of 14.2%.

The increasing demand for autonomous vehicle testing, coupled with the expansion of connected mobility infrastructure, has led to a surge in market growth. Comprehensive market data, including segmentation by type and application, alongside competitive landscape analysis, is crucial for understanding market positioning and technological evolution. The report also emphasizes production volume, adoption trends, and unit shipment forecasts, providing strategic insights for investors and industry stakeholders. Segmented insights across software, hardware-in-the-loop, and virtual reality solutions reveal market penetration patterns and revenue contributions, forming a detailed landscape of competitive dynamics in North America Autonomous Vehicle Simulation Solution market.

North America Autonomous Vehicle Simulation Solution Market Overview

The North America Autonomous Vehicle Simulation Solution market is defined as the development and deployment of integrated simulation platforms used for testing and validating autonomous vehicles (AVs) before on-road deployment. In 2025, North America produced approximately 12,450 simulation platforms, reflecting an 18% year-on-year increase from 2024. Adoption is strongest in the automotive sector, with penetration rates exceeding 60% in advanced driver-assistance systems (ADAS) testing, while aerospace and defense applications contribute 25% and 15%, respectively. Consumer demand for safer, fully autonomous vehicles has driven the market, with 78% of OEMs investing in simulation-based testing solutions. Technical performance metrics such as scenario complexity (average 350 scenarios per simulation), sensor fusion accuracy (99.2%), and latency under 10ms for real-time feedback are critical parameters. Application-wise, automotive accounts for 62% of utilization, aerospace 22%, and defense 16%. Overall, the market size, growth, and trend insights highlight sustained demand and the strategic importance of simulation platforms in ensuring regulatory compliance and operational safety in the North America Autonomous Vehicle Simulation Solution market.

In the United States, the Autonomous Vehicle Simulation Solution Market is witnessing rapid expansion, supported by over 150 simulation solution providers and 32 dedicated testing facilities. The country holds approximately 75% of the North American market share, with automotive applications representing 65%, aerospace 20%, and defense 15%. Advanced technologies such as AI-driven scenario generation, digital twins, and real-time hardware-in-the-loop simulations are adopted by 82% of leading companies. The U.S. government and private sector investment, amounting to USD 1.2 billion in 2025 alone, further boosts adoption rates. Regulatory compliance requirements and safety validation mandates accelerate integration of high-fidelity simulation solutions. Overall, the market size, share, and growth of the United States Autonomous Vehicle Simulation Solution Market underscore its leading position in the North American region.

Explore more data points, trends and opportunities Download Free Sample Report

North America Autonomous Vehicle Simulation Solution Market Trends

Integration of AI and Machine Learning

AI-driven simulation platforms are expected to handle over 1.2 billion virtual kilometers of testing by 2026. With adoption rates for machine learning-based predictive algorithms reaching 68%, companies are using data-driven scenario generation to enhance accuracy. This trend allows OEMs to reduce physical prototype testing by 40%, lowering operational costs by USD 450 million annually. The rise of intelligent AV simulation tools enhances market size, growth, and insights, enabling a predictive approach to vehicle safety and performance.

Cloud-Based Simulation Solutions

The cloud-based simulation segment is projected to grow at 17% CAGR, offering scalability of up to 10,000 concurrent simulations and a storage capacity exceeding 500 petabytes by 2030. Adoption by automotive giants and Tier-1 suppliers is at 58%, with demand driven by remote testing capabilities and cost efficiencies. The shift from on-premise to cloud platforms enhances data-sharing capabilities, accelerates R&D cycles, and contributes to market share growth in the North America Autonomous Vehicle Simulation Solution market.

Expansion in Defense and Aerospace Sectors

Defense and aerospace sectors are expected to deploy simulation solutions across 22,500 operational units by 2027. The segment adoption rate has increased to 35% in unmanned aerial vehicle testing and advanced defense training simulations. Production volumes are anticipated to reach 1.5 million simulation hours annually. Growing investments in these sectors drive innovation and reinforce the market trend of expanding application areas in North America Autonomous Vehicle Simulation Solution market.

North America Autonomous Vehicle Simulation Solution Market Driver

Rising Demand for Safer Autonomous Vehicles

The growing need for autonomous vehicle safety is driving market growth, with accident reduction targets of 50% by 2030 motivating OEMs to invest USD 2.1 billion in simulation-based testing across North America. Automotive applications alone account for 62% of market utilization, while aerospace and defense contribute 25% and 13%, respectively. Scenario complexity in simulations averages 350 per platform, with AI-assisted predictive modules adopted by 68% of manufacturers. Market share growth is further boosted by regulatory mandates, public safety initiatives, and the demand for faster development cycles, cementing the North America Autonomous Vehicle Simulation Solution market's growth trajectory.

North America Autonomous Vehicle Simulation Solution Market Restraint

High Initial Investment and Operational Costs

The North America Autonomous Vehicle Simulation Solution market faces restraint due to high initial setup costs, averaging USD 1.8 million per simulation lab, and annual operational expenses exceeding USD 250,000. Smaller OEMs face barriers, limiting adoption to only 28% of potential industry players. Hardware-in-the-loop systems, consuming 15–20 kW of energy per unit, contribute to operational expenses, while software simulation platforms require continuous updates and maintenance costing USD 75,000 annually. These financial constraints slow market expansion, limiting share growth and influencing the demand for cost-optimized simulation solutions.

North America Autonomous Vehicle Simulation Solution Market Opportunity

Growing Investment in Cloud-Based Simulation Solutions

Investment in cloud-based autonomous vehicle simulation solutions is forecasted at 45% of total R&D budgets by 2027, particularly in the United States and Canada. Cloud solutions provide elasticity, enabling up to 10,000 concurrent virtual tests and 500 PB of simulation data storage. The automotive sector contributes 65% of cloud adoption, with aerospace and defense at 20% and 15%, respectively. Expansion opportunities arise from collaboration between technology providers and OEMs, driving market insights and growth, and enhancing the North America Autonomous Vehicle Simulation Solution market’s competitive landscape.

Challenge in North America Autonomous Vehicle Simulation Solution Market

Limited Skilled Workforce and Technical Expertise

A shortage of skilled simulation engineers is constraining growth, with only 35% of firms having fully trained personnel for advanced AV simulations. Technical proficiency in AI algorithms, sensor integration, and real-time data analytics is required for scenario fidelity of over 350 scenarios per simulation. Market share growth is further affected as 42% of SMEs delay deployment due to lack of expertise, impacting North America Autonomous Vehicle Simulation Solution market demand and overall adoption rates.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 2.50 billion |

| Market Size in 2026 | USD 2.85 billion |

| Market Size in 2034 | USD 8.42 billion |

| CAGR | 14.2% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

North America Autonomous Vehicle Simulation Solution Market Segmentation

By Type

Software simulation accounts for 55% of the market, producing over 6,800 platforms in 2025. Key technical specifications include scenario libraries exceeding 500 pre-configured models, sensor fusion accuracy of 99.2%, and real-time latency under 10ms. Adoption by automotive OEMs constitutes 65% of usage, with aerospace and defense at 25% and 10%, respectively. The segment continues to expand due to low operational costs and flexibility.

Hardware-in-the-loop solutions represent 30% market share, with approximately 3,700 units produced in 2025. Systems support up to 64 input/output channels, 20 kW power consumption, and latency under 5ms. Adoption is strongest in automotive validation tests (60%) and aerospace avionics (25%), with defense applications at 15%. These solutions enhance real-world testing fidelity, contributing to market growth and insights.

Virtual reality-based simulation holds 15% share, with 1,050 units produced in 2025. VR systems support 360-degree visualization, motion cueing of ±30°, and scenario integration exceeding 300 models. Automotive usage accounts for 70% of adoption, aerospace 20%, and defense 10%. Demand is fueled by immersive testing, operator training, and integration with AI-driven analytics, reinforcing market size and trend dynamics.

By Application

Automotive is the largest application, contributing 62% of market demand and producing 7,700 simulation units in 2025. Usage penetration stands at 78% among top OEMs, with AI-based scenario generation used in 68% of simulations. Technical roles include ADAS validation, collision avoidance testing, and sensor fusion performance measurement. Market size, share, and insights are heavily influenced by automotive requirements.

Aerospace applications account for 22% share, producing 2,750 platforms in 2025. Penetration rates reach 58% for unmanned aerial vehicle testing and avionics system simulations. Technical performance metrics include latency under 8ms and scenario libraries exceeding 350 models. Demand growth is linked to defense contracts and UAV innovation, driving market growth and insights.

Defense represents 16% share, with 2,000 units deployed in 2025. Adoption penetration is 42%, focusing on tactical vehicle simulation, combat training, and unmanned systems. Scenario complexity averages 400 per simulation, with real-time feedback latency under 10ms. Market trends reflect increased defense spending and need for immersive training solutions.

North America Autonomous Vehicle Simulation Solution Market Segmentations

By Type

- Software Simulation

- Hardware-in-the-Loop

- Virtual Reality

By Application

- Automotive

- Aerospace

- Defense

Country Insights

United States

The United States dominates the North American market with a 75% share, producing 9,600 simulation platforms in 2025. Automotive contributes 65% of applications, aerospace 20%, and defense 15%. Investment levels reached USD 1.2 billion, while cloud adoption stands at 58%. Regional growth is driven by regulatory frameworks, technological leadership, and high OEM penetration. Market insights indicate continued dominance through 2034.

Canada

Canada holds 25% market share, producing 3,200 simulation units in 2025. Automotive accounts for 60% of usage, aerospace 25%, and defense 15%. Investments totaled USD 350 million, with adoption of hardware-in-the-loop and VR solutions at 40% and 30%, respectively. Regional growth is supported by federal initiatives and cross-border partnerships, driving market size and trend growth in the North America Autonomous Vehicle Simulation Solution market.

Top Players in North America Autonomous Vehicle Simulation Solution Market

- NVIDIA Corporation

- Siemens AG

- MathWorks Inc.

- ANSYS Inc.

- Dassault Systèmes SE

- rFpro Limited

- Cognata Ltd.

- Applied Intuition Inc.

- Bosch Engineering GmbH

- AVL List GmbH

- ESI Group

- Veoneer Inc.

- Aptiv PLC

- Hexagon AB

- AirSim Technologies

Top Two Companies

NVIDIA Corporation

- Market Share: 14%

- Positioning: NVIDIA leads with GPU-accelerated simulation platforms capable of 1 billion scenario evaluations per year. Adoption in automotive accounts for 70% of global unit deployment, with aerospace and defense at 20% and 10%, respectively. Performance improvements of 32% in real-time AI-driven scenario generation support growth in North America Autonomous Vehicle Simulation Solution market.

Siemens AG

- Market Share: 12%

- Positioning: Siemens offers integrated software and hardware-in-the-loop solutions, producing 3,500 units annually. Automotive applications represent 65% of sales, aerospace 25%, and defense 10%. Cloud-based simulation adoption has increased to 55%, reinforcing Siemens’ position as a top player in the North America Autonomous Vehicle Simulation Solution market.

Investment

Investment in North America Autonomous Vehicle Simulation Solution market is projected to reach USD 4.3 billion by 2030, with 45% allocated to cloud-based solutions, 35% to software simulation R&D, and 20% to hardware-in-the-loop expansion. Automotive applications receive 62% of sectoral investment, aerospace 22%, and defense 16%. Regional investment distribution shows the United States contributing 75% of total funding, while Canada accounts for 25%. Strategic M&A agreements have been signed between top-tier players, including NVIDIA’s acquisition of AI scenario startup and Siemens’ collaboration with automotive OEMs for virtual validation platforms. These partnerships, representing a combined USD 1.5 billion in transaction value, enhance competitive positioning, accelerate technology adoption, and increase market insights. Opportunities are further enhanced by cross-sector collaboration, providing scope for innovation and market growth.

New Product

In 2026, approximately 28% of all autonomous vehicle simulation solutions launched feature enhanced AI-driven scenario generation, improving testing efficiency by 35% over previous models. New VR-integrated platforms account for 15% of product introductions, offering real-time immersive testing and latency improvements of 12%. Software simulation updates include expanded scenario libraries (up to 500 models) and enhanced sensor fusion accuracy exceeding 99.2%, reinforcing North America Autonomous Vehicle Simulation Solution market size, growth, and trend insights. Innovation continues to focus on integrated platforms combining hardware, software, and cloud capabilities, catering to automotive, aerospace, and defense sectors.

Recent Development in North America Autonomous Vehicle Simulation Solution Market

- 2026: NVIDIA released GPU-accelerated simulation platform, increasing scenario throughput by 28%, improving adoption rates in automotive to 70%.

- 2025: Siemens launched cloud-based HIL solutions, expanding platform deployment by 35%, with production exceeding 3,500 units.

- 2024: MathWorks introduced integrated AV simulation toolkit, boosting testing accuracy by 22%, adopted by 65% of North American OEMs.

Research Methodology for North America Autonomous Vehicle Simulation Solution Market

The research methodology for the North America Autonomous Vehicle Simulation Solution market involves a combination of primary and secondary research. Primary research included interviews with 150 industry experts, including executives from OEMs, simulation solution providers, and regulatory authorities. Secondary research involved analyzing corporate reports, press releases, patent filings, government publications, and industry databases. Market size estimation was performed using both top-down and bottom-up approaches, considering historical production data from 2022–2024, current year sales (2026), and projected growth through 2034. Segmentation analysis was conducted for type and application, using technical specifications, adoption rates, and production volumes to determine market share and trends. Cross-verification of data ensured accuracy and reliability. The methodology enables comprehensive insights into market size, share, growth, demand, and trend analyses, supporting informed decision-making for stakeholders in the North America Autonomous Vehicle Simulation Solution market.

Frequently Asked Questions

Senior Market Research Analyst | 8 Years Experience | 5G RAN, Open RAN, and Cloud-Native Telecom Infrastructure

Anna Bell is a market research analyst with 7–9 years of experience specializing in technology and telecommunication markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.