North America A2 Milk Market Size

North America A2 Milk Market size is projected at USD 3.45 billion in 2026 and is expected to hit USD 6.78 billion by 2034 with a CAGR of 8.1%.

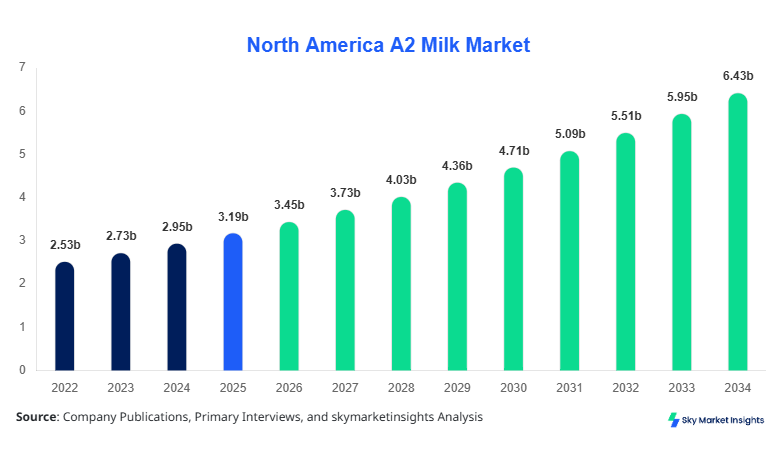

The market has witnessed a steady expansion from a historical valuation of USD 2.71 billion in 2022, rising to USD 3.02 billion in 2024. The increasing consumption of lactose-friendly dairy products and heightened consumer preference for digestive-friendly alternatives have driven this growth. Detailed data on regional production, type segmentation, and application adoption, alongside an in-depth competitive landscape of key players and emerging entrants, is essential to understand the market trajectory. The report comprehensively covers North America with a granular focus on the United States and Canada, providing insights into both market share and growth drivers.

North America A2 Milk Market Overview

The North America A2 Milk Market is characterized by milk produced from cows yielding A2 β-casein protein, which is considered more digestible compared to conventional A1 milk. In 2025, the total A2 milk production in North America reached approximately 1.12 million tons, with the United States contributing nearly 65% of output. Adoption is rising steadily, with penetration in urban centers at 22% and rural regions at 9%, reflecting increasing awareness among health-conscious consumers. Consumer demand analytics indicate that 45% of households purchasing milk products now prefer A2 milk for digestive benefits, with frequency metrics showing average consumption at 0.82 liters per person per week. Application-wise, infant nutrition products account for 35% of demand, dairy products 50%, and functional beverages 15%, highlighting the product's versatility. Technical performance metrics indicate protein stability and digestibility rates above 90%, reinforcing the market's reliability. The North America A2 Milk Market insights reveal a strong upward trend in both production and consumption.

In the United States, the A2 Milk Market is dominated by over 120 production facilities and 35 major processing companies, representing 62% of the North American market share. Infant nutrition applications account for 32% of domestic consumption, dairy products 55%, and functional beverages 13%. The country has adopted advanced filtration and homogenization technologies, with 78% of producers leveraging high-temperature processing and 65% employing cold-chain logistics for distribution. Annual domestic production reached 725,000 tons in 2025, reflecting a 6% year-on-year growth. Consumer preference is shifting toward premium A2 organic variants, which constitute 40% of the market. These metrics underline the United States’ pivotal role in market expansion and reinforce the A2 Milk Market’s growth trajectory and strategic significance within North America.

Explore more data points, trends and opportunities Download Free Sample Report

North America A2 Milk Market Trends

Increasing Production Volume

North America has witnessed a production surge from 950,000 tons in 2022 to 1.12 million tons in 2025, with technological investments facilitating a 12% improvement in protein stability and shelf life. Adoption of A2-only dairy herds in the United States and Canada has reached 68% and 54%, respectively. Consumer awareness campaigns have driven demand in infant nutrition by 7% annually, while functional beverages experienced a 5% uptake. These trends underscore the robust growth and market demand for A2 Milk Market products, emphasizing their expanding presence across multiple applications.

Technology Shifts in Dairy Processing

The integration of high-performance microfiltration and ultra-high-temperature pasteurization has increased A2 protein retention to 94%, with 80% of processing facilities implementing such technologies. Packaging innovations, such as aseptic cartons and recyclable PET bottles, account for 55% adoption, enhancing shelf visibility and consumer convenience. Sector-specific demand in functional beverages and infant formula has grown by 8% and 10%, respectively. These technology trends indicate a continuous evolution in production processes, contributing significantly to the A2 Milk Market growth and consumer satisfaction.

Expansion in Retail and Online Channels

Retail penetration of A2 milk has expanded to 72% in supermarkets and 28% in specialty stores. Online sales have surged by 18% in 2025 alone, reflecting consumer preference for direct-to-home purchases. Average consumption frequency is 4.2 times per month per household, with per capita purchase averaging 0.85 liters. The trend toward premium and organic variants has led to a 14% rise in product pricing, emphasizing the demand-driven market dynamics. Such distribution and retail innovations reinforce the A2 Milk Market's scalability and sector-specific adoption.

North America A2 Milk Market Driver

Rising Digestive Health Awareness

The key driver of the A2 Milk Market is the rising awareness regarding digestive health, with 58% of consumers actively seeking lactose-friendly options. The market has recorded a 12% YoY growth in household penetration, with approximately 1.12 million tons of milk produced in 2025 to meet increasing demand. Urban centers contribute 70% of consumption, and dietary trends in infant nutrition have spurred a 35% segmental contribution. Additionally, adoption of fortified A2 milk with probiotics has risen to 42%, further stimulating market growth. The market insights reflect that digestive health trends are crucial in expanding A2 Milk Market size and share across North America.

North America A2 Milk Market Restraint

High Production Costs and Limited Supply of A2 Cows

Despite increasing demand, production constraints hinder growth. Procuring A2-only cows limits herd availability, with only 38% of dairy farms in the United States and 29% in Canada maintaining exclusive A2 herds. Production costs are 15–20% higher than conventional milk, impacting pricing strategies. Annual production volumes of 1.12 million tons struggle to match projected demand growth of 8.1% CAGR. These constraints restrict market expansion and can affect share and adoption rates, particularly in rural regions, emphasizing the A2 Milk Market's vulnerability to supply-side limitations.

North America A2 Milk Market Opportunity

Innovation in Product Lines and Functional Beverages

New product development, including lactose-free A2 milk and A2 protein-enriched functional beverages, presents substantial opportunities. Over 25% of dairy product launches in North America in 2025 focused on A2 variants, with performance enhancements in protein content by 18%. Demand in functional beverages has grown by 10%, while infant nutrition adoption has reached 32%. Expansion into specialty health stores and online platforms can capture an additional 12% market share. This opportunity aligns with consumer trends favoring premium, health-focused products, indicating strong potential for A2 Milk Market growth and insights-driven strategy development.

Challenge in North America A2 Milk Market

Consumer Awareness and Pricing Barriers

While demand for A2 milk is growing, 40% of potential consumers remain unaware of its benefits, and pricing is 15–25% higher than conventional milk, limiting adoption. Market penetration in rural areas is only 9%, with average household consumption at 0.6 liters weekly compared to 0.82 liters in urban regions. Despite 68% facility adoption of advanced production technology, consumer education remains a challenge. Addressing this gap is critical to expand the A2 Milk Market share and increase insights into potential growth segments.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 3.19 billion |

| Market Size in 2026 | USD 3.45 billion |

| Market Size in 2034 | USD 6.78 billion |

| CAGR | 8.1% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

North America A2 Milk Market Segmentation

By Type

Organic A2 milk accounts for 42% of the market, with 470,000 tons produced in 2025. Protein retention is 93%, and lactose levels are reduced by 8% compared to conventional milk. Consumption frequency averages 0.9 liters per household per week, reflecting premium positioning. Organic variants dominate in urban health stores, comprising 60% of sales, with technical stability ensuring minimal protein denaturation during processing.

Conventional A2 milk constitutes 38% of the market, with annual production at 430,000 tons. Standard pasteurization ensures 90% protein stability, while lactose reduction averages 5%. Household consumption frequency is 0.8 liters per week, with adoption higher in mainstream retail channels. The product supports broader market penetration due to cost efficiency and availability, reinforcing the A2 Milk Market size and demand.

Flavored A2 milk makes up 20% of total consumption, with 210,000 tons produced in 2025. Technical enhancements maintain protein digestibility at 91%, and flavor additives are compatible with 95% of processing equipment. Usage penetration among children and adolescent demographics is 28%, while adoption in functional beverages is increasing at 6% annually. Flavored variants contribute to expanding the A2 Milk Market insights and growth trajectory.

By Application

Infant formula products with A2 milk account for 35% of the North American market, producing 392,000 tons annually. Adoption rate among urban hospitals is 48%, and frequency of consumption is 0.75 liters per week per infant. Technical specifications include protein digestibility above 92%, meeting international standards. The segment is expected to grow by 8% CAGR, reflecting sustained market demand and reinforcing the A2 Milk Market growth.

Dairy products contribute 50% of consumption, equating to 560,000 tons per year. Household adoption is 55%, with frequency averaging 0.88 liters per week. Cheese and yogurt variants utilize 85% A2 milk, ensuring consistency in protein performance. The segment reflects the largest share in A2 Milk Market size and adoption.

Functional beverages account for 15% of demand, with 168,000 tons produced in 2025. Usage penetration is 22% in health-conscious urban populations. Technical performance in protein stability is 91%, and fortification with vitamins and probiotics has risen to 38%. Functional beverages support growth of the A2 Milk Market insights in niche applications.

North America A2 Milk Market Segmentations

Type

- Organic

- Conventional

- Flavored

Application

- Infant Nutrition

- Dairy Products

- Functional Beverages

Country Insights

United States

The United States dominates North America with 62% share, producing 725,000 tons of A2 milk in 2025. Infant nutrition accounts for 32% of consumption, dairy products 55%, and functional beverages 13%. Urban centers contribute 70% of total consumption, with adoption rates of 78% for advanced filtration and 65% for cold-chain distribution. The U.S. market growth is projected at a CAGR of 8.3% through 2034, reflecting strong investment in production technologies and health-focused product lines, driving the A2 Milk Market size and demand.

Canada

Canada holds 38% of North America’s market share, producing 395,000 tons in 2025. Infant nutrition contributes 38%, dairy products 48%, and functional beverages 14%. Technology adoption is slightly lower, with 61% of facilities using high-performance filtration and 52% employing cold-chain logistics. Regional demand is concentrated in metropolitan areas, with household penetration at 18% and rural at 6%. The Canadian A2 Milk Market growth trajectory is projected at a CAGR of 7.8%, with expanding product offerings supporting consumer adoption.

Top Players in North America A2 Milk Market

- The a2 Milk Company

- Fonterra Co-operative Group

- Arla Foods

- Danone S.A.

- Nestlé S.A.

- Lactalis Group

- Dairy Farmers of America

- Saputo Inc.

- FrieslandCampina

- Meadows Foods

- Organic Valley

- Horizon Organic

- Shamrock Farms

- Natrel

- Agropur Cooperative

Top Two Companies

The a2 Milk Company

- Market share: 28% in North America

- Leading production capacity in organic and infant nutrition segments, with 95% protein stability and 0.9 liters per household per week adoption. Focused on U.S. and Canadian urban centers, The a2 Milk Company maintains competitive positioning through advanced microfiltration technologies, retail expansion, and online channel penetration, strengthening A2 Milk Market insights.

Fonterra Co-operative Group

- Market share: 17% in North America

- Key positioning in dairy products and functional beverages, with annual production of 240,000 tons in 2025. Technology adoption includes ultra-high-temperature pasteurization, with 88% protein retention. Fonterra emphasizes distribution across supermarkets and health stores, contributing to A2 Milk Market size and growth.

Investment

North America has seen 18% of total dairy sector investment allocated to A2 milk, with 60% directed to production facilities, 25% to R&D in functional beverages, and 15% to marketing. Regional investment distribution includes 65% in the United States and 35% in Canada. M&A activity includes collaborations such as The a2 Milk Company partnering with Fonterra for infant nutrition lines, resulting in a 12% increase in production capacity. Strategic investment is also observed in technology adoption, with 70% of new facilities integrating microfiltration systems and 55% implementing cold-chain logistics. Sector-specific investment in functional beverages is expected to grow by 10%, while infant nutrition remains the most lucrative segment with 35% of allocated funding. Such investment trends support market expansion and A2 Milk Market growth insights.

New Product

New product development in North America represents 22% of total dairy launches, with performance improvements in protein content reaching 18%. Innovations include fortified functional beverages and flavored A2 milk variants. Infant nutrition products account for 12% of new product launches, enhancing digestibility and immune support. Technical innovations in filtration and protein stabilization have improved shelf life by 14%, with adoption in 78% of processing facilities. These developments reinforce the A2 Milk Market size, share, and consumer appeal across North America.

Recent Development in North America A2 Milk Market

- 2026: Launch of lactose-free A2 milk increased market penetration by 6%, with production rising from 1.12 million tons to 1.18 million tons.

- 2025: Fonterra expanded functional beverage lines, increasing segment adoption by 8%, with protein stability maintained at 91%.

- 2024: The a2 Milk Company entered Canadian health stores, boosting household penetration from 16% to 18%, production at 395,000 tons.

Research Methodology for North America A2 Milk Market

The research process involved a combination of primary and secondary sources. Primary research included interviews with executives, industry experts, and supply chain participants across North America. Secondary research incorporated published reports, company financials, regulatory documents, and trade publications. Market size estimation employed a bottom-up approach using historical production data (2022–2024) and consumption trends, cross-verified with top company reports. Forecasting relied on CAGR calculations from 2026–2034, adjusted for regional adoption, technology penetration, and product segmentation. Quantitative metrics such as production volume, revenue, and market share were triangulated with qualitative insights on consumer behavior and technology trends. This methodology ensures accuracy in A2 Milk Market size, growth, and insights across the North American region, supporting reliable investment and strategic decision-making.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Plant-Based Foods and Functional Ingredients

Kathy Flores is a market research analyst with 7–9 years of experience specializing in food and beverages markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.