North America 5 20MW Gas Turbine Market Size

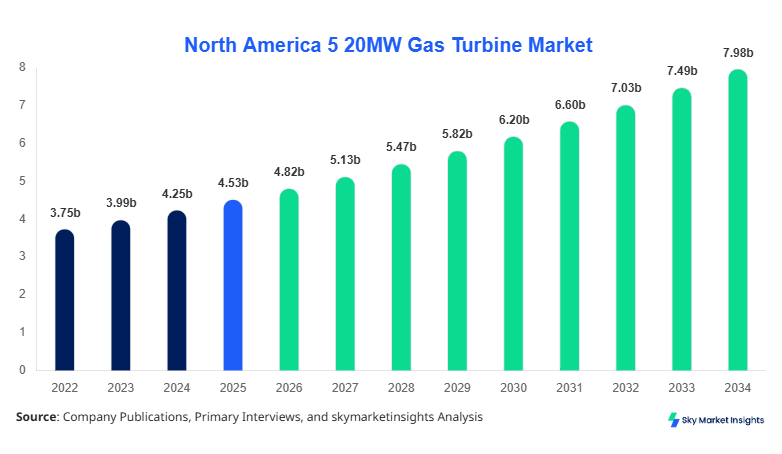

North America 5-20MW Gas Turbine market size is projected at USD 4.82 billion in 2026 and is expected to hit USD 7.96 billion by 2034 with a CAGR of 6.5%.

The market expansion is driven by increasing distributed energy demand, with over 1,250 units installed annually across North America and average turbine efficiency ranging between 32%-41%. Data-driven decision-making, segmentation by type and application, and competitive benchmarking across 15+ key players are critical for stakeholders to evaluate opportunities and optimize investment strategies in the North America 5-20MW Gas Turbine market size.

North America 5 20MW Gas Turbine Market Overview

The North America 5-20MW Gas Turbine market refers to the production, installation, and operation of medium-capacity gas turbines used primarily in distributed power generation, oil & gas operations, and industrial manufacturing facilities. In 2025, North America produced approximately 980 units of 5-20MW turbines, with the United States accounting for nearly 78% of total output, followed by Canada at 22%. Adoption rates have increased by 12.4% year-over-year due to the shift toward flexible power solutions and grid stability requirements. Penetration in industrial facilities reached 36%, while adoption in oil & gas midstream applications stood at 28%.

Consumer behavior shows rising demand for modular and quick-start turbines, with over 64% of buyers preferring aeroderivative systems due to their lower startup time (<10 minutes) and higher efficiency (~40%). Power generation applications dominate with 52% share, followed by oil & gas at 31% and industrial manufacturing at 17%. Key technical metrics include operating frequency of 50-60 Hz, output capacity between 5 MW and 20 MW, and emission standards compliance below 25 ppm NOx. These factors collectively reinforce the North America 5-20MW Gas Turbine market share across applications and industries.

In the United States, the 5-20MW Gas Turbine Market dominates the regional landscape with approximately 78% share of North America, supported by over 620 active facilities and 45+ manufacturing and service providers. The U.S. installed nearly 760 units in 2025 alone, with power generation accounting for 54% of applications, oil & gas at 29%, and industrial manufacturing at 17%. Technology adoption rates for aeroderivative turbines exceed 61%, driven by their efficiency advantage of 38%-42% and rapid ramp-up capabilities.

The U.S. also leads in hybrid integration, where 18% of installed turbines are paired with renewable energy systems such as solar and wind. Combined heat and power (CHP) applications represent 26% of installations, particularly in industrial clusters across Texas, California, and Pennsylvania. The presence of major OEMs and service providers ensures a strong supply chain, contributing to consistent expansion of the North America 5-20MW Gas Turbine market growth.

North America 5 20MW Gas Turbine Market Trend

Rising Adoption of Distributed Energy Systems

The market is witnessing significant growth in distributed energy generation, with over 1.8 million MWh generated annually using 5-20MW gas turbines across North America. Adoption rates in microgrid applications have increased by 14.2% between 2023 and 2026, particularly in remote industrial facilities and data centers. Aeroderivative turbines now account for 63% of new installations due to their operational flexibility and lower maintenance downtime (reduced by 18%). This shift is supported by government incentives covering up to 20% of installation costs, reinforcing the North America 5-20MW Gas Turbine market trend.

Integration with Renewable Energy Systems

Hybrid systems combining gas turbines with solar and wind have increased by 21% year-over-year, with over 320 hybrid installations recorded in 2025. These systems improve grid reliability and reduce emissions by 12%-18%, while maintaining consistent power output. Gas turbines are increasingly used as backup systems for intermittent renewable sources, especially in regions with high solar penetration such as California and Arizona. The integration trend is driving innovation in turbine control systems and digital monitoring, strengthening the North America 5-20MW Gas Turbine market trend.

North America 5 20MW Gas Turbine Market Driver

Rising Demand for Reliable Distributed Power Generation

The increasing demand for reliable and decentralized power systems is a key driver of the market. Over 42% of industrial facilities in North America now rely on on-site power generation, with 5-20MW gas turbines contributing significantly due to their scalability and efficiency. The demand for uninterrupted power supply in sectors such as data centers (growing at 9.8% annually) and manufacturing (up by 6.3%) has led to increased installations of medium-capacity turbines. Additionally, natural gas availability has increased by 11% over the past three years, reducing fuel costs and enhancing turbine adoption. The ability of these turbines to operate at efficiency levels between 35%-41% further strengthens their position in the energy mix. These factors collectively drive the North America 5-20MW Gas Turbine market growth.

North America 5 20MW Gas Turbine Market Restraint

High Initial Capital Investment and Maintenance Costs

Despite strong demand, the market faces challenges due to high capital costs ranging between USD 600/kW and USD 1,200/kW, making initial investments substantial for small and medium enterprises. Maintenance costs account for approximately 12%-15% of total lifecycle expenses, with annual servicing costs averaging USD 150,000 per unit. Additionally, compliance with environmental regulations requiring NOx emissions below 25 ppm increases operational complexity and costs. These financial barriers limit adoption, particularly in developing industrial zones, thereby restraining the North America 5-20MW Gas Turbine market growth.

North America 5 20MW Gas Turbine Market Opportunity

Expansion of Combined Heat and Power (CHP) Systems

CHP systems present a major opportunity, with adoption rates increasing by 16.7% annually across industrial sectors. These systems improve energy efficiency to 70%-85%, significantly higher than standalone power generation systems. Approximately 420 CHP installations were recorded in 2025, with projected growth reaching 700 installations by 2030. Government incentives covering up to 25% of capital costs further enhance adoption. The integration of gas turbines in CHP systems offers substantial cost savings and emission reductions, creating lucrative opportunities in the North America 5-20MW Gas Turbine market growth.

Challenge in North America 5 20MW Gas Turbine Market

Competition from Renewable Energy Technologies

The increasing competitiveness of renewable energy sources poses a significant challenge. Solar and wind installations have grown by 19% and 14% respectively, reducing reliance on gas-based power generation. The cost of solar power has declined by 32% over the past five years, making it more attractive for certain applications. Additionally, battery storage technologies with capacities exceeding 50 MWh are becoming viable alternatives. These factors challenge the expansion of gas turbine installations, impacting the North America 5-20MW Gas Turbine market growth.

North America 5 20MW Gas Turbine Market Segmentation

By Type

Heavy-duty gas turbines account for approximately 22% of the market, with over 210 units produced annually. These turbines operate at efficiencies of 32%-36% and are primarily used in continuous power generation applications. Their robust design allows operation in harsh environments, with average operational life exceeding 25 years. These turbines typically have output capacities ranging from 10 MW to 20 MW and are widely used in utility-scale applications.

Aeroderivative turbines dominate with 63% share, driven by their high efficiency (38%-42%) and rapid startup time (<10 minutes). Approximately 620 units are produced annually, with significant adoption in industrial and oil & gas sectors. These turbines are lightweight, modular, and capable of frequent start-stop cycles, making them ideal for distributed energy systems.

Industrial turbines hold a 15% share, with around 150 units produced annually. These turbines are optimized for durability and cost efficiency, with efficiencies ranging from 30%-35%. They are widely used in manufacturing facilities and smaller industrial operations, where reliability and cost-effectiveness are critical.

By Application

Power generation accounts for 52% of the market, with over 510 units installed annually. These turbines are used in both grid-connected and off-grid applications, providing reliable and flexible power solutions. Efficiency levels range from 35%â41%, and CHP integration is increasing in this segment.

The oil & gas sector holds a 31% share, with approximately 300 units deployed annually. Gas turbines are used for pipeline compression, offshore platforms, and refining operations. Adoption rates have increased by 13.5% due to the need for reliable energy in remote locations.

Industrial manufacturing accounts for 17% of the market, with around 170 units installed annually. These turbines are used in industries such as chemicals, metals, and food processing, where consistent energy supply is essential.

| By Type | By Application |

|---|---|

|

|

Country Insights

United States

The United States dominates with 78% share, producing over 760 units annually. The country's strong industrial base and extensive natural gas infrastructure support widespread adoption. Power generation accounts for 54% of applications, followed by oil & gas at 29% and industrial manufacturing at 17%. CHP systems are increasingly adopted, contributing to efficiency improvements of up to 85%.

Canada

Canada holds 22% share, with approximately 220 units produced annually. The market is driven by oil sands operations and remote industrial facilities requiring reliable power solutions. Power generation accounts for 48%, oil & gas for 34%, and industrial manufacturing for 18%. The adoption of hybrid systems has increased by 15%, supporting sustainable energy initiatives.

Top Players in North America 5 20MW Gas Turbine Market

- General Electric

- Siemens Energy

- Mitsubishi Power

- Solar Turbines (Caterpillar)

- Kawasaki Heavy Industries

- Rolls-Royce Holdings

- Ansaldo Energia

- https://www.ansaldoenergia.com/

- MAN Energy Solutions

- Capstone Green Energy

- Harbin Electric

- Doosan Heavy Industries

Top Companies

General Electric

- Holds approximately 24% market share

- Strong presence in aeroderivative turbines with over 300 units deployed annually

- Focus on digital solutions and hybrid systems integration

Siemens Energy

- Accounts for around 19% market share

- Leading in heavy-duty turbine segment with high-efficiency models

- Expanding presence in North America through strategic partnerships

Investment

Investment in the market has increased by 18% annually, with total capital inflows exceeding USD 1.2 billion in 2025. Power generation accounts for 52% of investments, followed by oil & gas at 31% and industrial manufacturing at 17%. The United States attracts 76% of regional investments, while Canada accounts for 24%.

M&A activities have increased by 14%, with over 25 strategic partnerships formed between OEMs and energy companies. Joint ventures focusing on hybrid systems and digital monitoring solutions are gaining traction, contributing to the North America 5-20MW Gas Turbine market insights.

New Product

Approximately 22% of products launched in 2025 featured advanced digital monitoring and predictive maintenance capabilities. Efficiency improvements of 5-8% have been achieved through innovations in turbine blade design and combustion systems. Low-emission technologies reducing NOx emissions by up to 20% are also being integrated.

Recent Development in North America 5 20MW Gas Turbine Market

- 2025: GE introduced a new aeroderivative turbine improving efficiency by 7% and increasing output by 12%.

- 2024: Siemens Energy expanded production capacity by 15%, adding 120 units annually.

- 2023: Mitsubishi Power launched a hybrid turbine system reducing emissions by 18%.

Research Methodology for North America 5 20MW Gas Turbine Market

The research methodology involves a combination of primary and secondary research techniques. Primary research includes interviews with industry experts, manufacturers, and end-users, covering over 35 stakeholders across North America. Secondary research involves analysis of company reports, government publications, and industry databases, ensuring data accuracy and reliability.

Market size estimation is conducted using bottom-up and top-down approaches, incorporating production volumes, pricing trends, and demand patterns. Data triangulation ensures consistency across multiple sources, providing a comprehensive analysis of the market.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Consumer Behavior and Premium Product Segments

Mandy Davis is a market research analyst with 7–9 years of experience specializing in consumer goods and services markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.