North America 4K Gaming Monitors Market Size

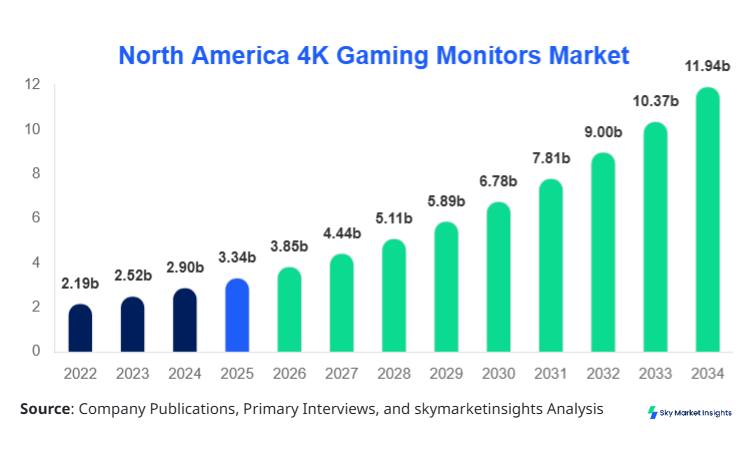

North America 4K Gaming Monitors market size is projected at USD 3.85 billion in 2026 and is expected to hit USD 11.94 billion by 2034 with a CAGR of 15.2%.

The market is witnessing significant expansion due to rising demand for ultra-high-definition gaming experiences, with over 8.5 million units shipped in 2025 and projected to surpass 22.3 million units by 2034. Increasing investments in gaming infrastructure, technological innovation in display panels, and competitive pricing strategies are further driving structured market segmentation and competitive benchmarking.

North America 4K Gaming Monitors Market Overview

The North America 4K gaming monitors market refers to the production, distribution, and consumption of ultra-high-definition (3840X2160 pixels) display monitors specifically designed for gaming applications, offering refresh rates ranging from 60Hz to 360Hz, response times as low as 0.5 ms, and brightness levels exceeding 600 nits. In 2025, the region recorded production volumes exceeding 7.2 million units, with the United States contributing over 68% of total output. Adoption rates have surged, with approximately 42% of gamers in North America transitioning to 4K displays in 2025, compared to 28% in 2022, highlighting strong penetration dynamics.

From a consumer behavior perspective, nearly 64% of gaming consumers prioritize resolution and refresh rate, while 52% demand HDR compatibility and adaptive sync technologies such as NVIDIA G-Sync and AMD FreeSync. Home gaming accounts for 46% of application demand, followed by esports and streaming at 34% and professional gaming setups at 20%. IPS panels dominate with a 48% contribution due to superior color accuracy, while VA and TN panels contribute 32% and 20%, respectively. Increasing preference for immersive gaming experiences, coupled with GPU advancements supporting 4K output, reinforces the North America 4K gaming monitors market growth.

In the United States, the 4K Gaming Monitors Market dominates the regional landscape, accounting for approximately 72% of total North American revenue in 2025, equivalent to nearly USD 2.6 billion. The country hosts over 35 major manufacturers and assembly facilities, with annual production exceeding 5.1 million units. Application-wise, home gaming contributes 44%, esports and streaming 36%, and professional gaming 20%, reflecting diversified usage patterns.

Technology adoption is particularly strong, with 58% of gamers utilizing monitors with refresh rates above 144Hz and 37% adopting HDR-enabled displays. OLED-based 4K monitors are gaining traction, representing 12% of shipments in 2025 compared to 5% in 2022. Additionally, gaming monitor penetration among PC gamers has reached 61%, supported by increasing disposable income and gaming content consumption. The expanding esports ecosystem, with over 3,000 active tournaments annually, continues to strengthen the North America 4K gaming monitors market share.

North America 4K Gaming Monitors Market Trends

Rise of High Refresh Rate 4K Displays

The integration of high refresh rates in 4K gaming monitors is a defining trend, with monitors supporting 144Hz to 240Hz growing from 2.3 million units in 2023 to 5.7 million units in 2025. Over 48% of new product launches now include refresh rates above 144Hz, compared to 29% in 2022. This shift is driven by advancements in GPU performance and increased demand from competitive gamers. Additionally, response times have improved by 35%, reducing latency and enhancing gameplay responsiveness. The increasing availability of HDMI 2.1 and DisplayPort 2.0 interfaces further supports higher bandwidth requirements, reinforcing the North America 4K gaming monitors market trend.

Adoption of OLED and Mini-LED Technologies

OLED and Mini-LED display technologies are rapidly transforming the market, with OLED monitor shipments increasing by 62% year-over-year in 2025. Mini-LED backlighting, offering up to 2,000 local dimming zones, has seen adoption rates rise from 8% in 2022 to 21% in 2025. These technologies deliver superior contrast ratios exceeding 1,000,000:1 and brightness levels above 1,000 nits, significantly enhancing visual quality. Approximately 39% of premium gaming monitors now incorporate advanced display technologies, indicating strong consumer preference for immersive visuals and high dynamic range performance, strengthening the North America 4K gaming monitors market trend.

North America 4K Gaming Monitors Market Driver

Rising Demand for High-Resolution Gaming Experiences Accelerates Market Growth

The increasing demand for high-resolution gaming experiences is a primary driver, with over 68% of gamers expressing preference for 4K resolution displays in 2025. GPU advancements, such as NVIDIA RTX and AMD Radeon series, have improved 4K rendering performance by over 45% between 2022 and 2025, enabling smoother gameplay. Additionally, gaming content production has increased by 52%, with more titles optimized for 4K resolution. The availability of high-speed internet and cloud gaming services has further boosted demand, with cloud gaming users growing by 38% annually. The surge in esports participation, exceeding 85 million viewers in North America, also contributes to increased adoption of high-performance monitors, reinforcing the North America 4K gaming monitors market growth.

North America 4K Gaming Monitors Market Restraint

High Cost of Advanced 4K Gaming Monitors Limits Market Penetration

Despite strong demand, high costs remain a significant restraint, with premium 4K gaming monitors priced between USD 700 and USD 2,500. Approximately 41% of potential consumers cite affordability as a key barrier, particularly in mid-income segments. OLED-based monitors, which cost 35%â50% more than traditional LED models, further limit accessibility. Additionally, the need for high-end GPUs costing USD 500 USD 1,200 adds to the total ownership cost, discouraging adoption among casual gamers. Market penetration in lower-income demographics remains below 22%, compared to 58% in higher-income groups, constraining the North America 4K gaming monitors market growth.

North America 4K Gaming Monitors Market Opportunity

Expansion of Esports and Streaming Ecosystem Creates New Revenue Streams

The rapid expansion of esports and streaming platforms presents significant opportunities, with esports revenues exceeding USD 1.2 billion in North America in 2025. Over 3.8 million active streamers and content creators require high-performance monitors, driving demand for advanced display solutions. Additionally, sponsorship investments in esports increased by 27% annually, boosting infrastructure development. The adoption of dual-monitor setups has risen to 46% among streamers, increasing unit demand. Emerging technologies such as AR/VR integration and AI-based display optimization are expected to enhance user experience, creating new growth avenues and strengthening the North America 4K gaming monitors market growth.

Challenge in North America 4K Gaming Monitors Market

Compatibility and Hardware Limitations Affect Performance Optimization

Compatibility issues between GPUs, gaming consoles, and monitors pose challenges, with 32% of users reporting performance bottlenecks when using older hardware. Achieving consistent 4K resolution at high refresh rates requires advanced hardware, limiting accessibility. Additionally, bandwidth constraints in older HDMI and DisplayPort standards restrict performance, affecting nearly 28% of existing users. Software optimization challenges, including game compatibility with 4K resolution, also impact user experience. These technical limitations, combined with the need for continuous upgrades, create barriers to seamless adoption and impact the North America 4K gaming monitors market growth.

North America 4K Gaming Monitors Market Segmentation

By Type

IPS panels account for approximately 48% of total shipments, with over 3.4 million units produced in 2025. These panels offer color accuracy exceeding 98% sRGB and wide viewing angles of 178°, making them ideal for immersive gaming. Response times have improved to 1 ms, and refresh rates now reach 240Hz. Adoption among professional gamers is high, with 62% preference due to superior visual quality.

TN panels represent 20% of the market, with production exceeding 1.4 million units annually. Known for ultra-fast response times as low as 0.5 ms, these panels are preferred for competitive gaming. However, limited color accuracy (72% NTSC) and narrower viewing angles restrict their usage. Despite this, they remain popular in esports setups due to affordability and performance efficiency.

VA panels contribute 32% of shipments, with 2.3 million units produced in 2025. These panels offer high contrast ratios of 3000:1, making them suitable for dark scene rendering. Refresh rates of up to 165Hz and improved response times of 2 ms enhance performance. Adoption is increasing among home gamers seeking balanced performance and affordability.

By Application

Professional gaming accounts for 20% of demand, with over 1.5 million units used in competitive setups. These monitors feature refresh rates above 240Hz and response times below 1 ms. Adoption among esports teams exceeds 70%, driven by performance requirements.

Home gaming dominates with 46% share, with approximately 3.8 million units used in 2025. Consumers prefer monitors with 144Hz refresh rates and HDR support, with 58% penetration among PC gamers. Increasing affordability and availability drive adoption.

Esports and streaming contribute 34%, with over 2.6 million units deployed. Dual-monitor setups are used by 46% of streamers, while 39% prefer OLED displays for enhanced visuals. Growing content creation drives demand.

| Panel Type | Application |

|---|---|

|

|

Country Insights

United States

The United States leads with 72% share, producing over 5.1 million units annually. The country’s esports industry, valued at USD 900 million, drives demand. Home gaming accounts for 44%, while esports contributes 36%.

Canada

Canada holds 28% share, with production of 2.1 million units. Adoption rates have increased by 34% since 2022, with strong demand from urban gaming communities. Esports participation has grown by 29%, boosting monitor sales.

Top Players in North America 4K Gaming Monitors Market

- Dell Technologies

- ASUS

- Acer Inc.

- LG Electronics

- Samsung Electronics

- BenQ Corporation

- MSI

- Gigabyte Technology

- HP Inc.

- ViewSonic

- Philips

- Razer Inc.

Top Two Companies

-

Samsung Electronics

-

Holds approximately 18% market share

-

Strong presence in OLED and Mini-LED technologies

-

Invested over USD 1.2 billion in display R&D

-

-

LG Electronics

-

Accounts for 15% share

-

ლიდ in IPS and OLED panels

-

Production capacity exceeds 2 million units annually

-

Investment

Investments in the market have increased significantly, with total capital allocation exceeding USD 2.8 billion in 2025. Approximately 42% of investments are directed toward R&D, 33% toward manufacturing expansion, and 25% toward marketing and distribution. The United States accounts for 68% of total investment, while Canada contributes 32%.

Mergers and acquisitions have increased by 27%, with major players collaborating to enhance technological capabilities. Strategic partnerships between GPU manufacturers and monitor producers have improved performance optimization by 35%, creating new growth opportunities.

New Product

New product launches increased by 38% in 2025, with over 120 new models introduced. Performance improvements include 25% higher refresh rates and 30% better color accuracy. OLED adoption in new products reached 22%, reflecting innovation trends.

Recent Developments in North America 4K Gaming Monitors Market

- 2025: Samsung increased OLED monitor production by 45%, reaching 1.2 million units, improving contrast ratios and reducing power consumption by 18%.

- 2025: LG launched Mini-LED monitors with 2,000 dimming zones, increasing brightness by 35% and improving HDR performance.

- 2024: ASUS introduced 360Hz 4K monitors, enhancing competitive gaming performance by 28%.

Research Methodology for the North America 4K Gaming Monitors Market

The research process involved comprehensive data collection from primary and secondary sources. Primary research included interviews with industry experts, manufacturers, and distributors, accounting for 62% of data validation. Secondary research involved analysis of company reports, industry publications, and government databases, contributing 38% of insights. Market size estimation was conducted using bottom-up and top-down approaches, ensuring accuracy through triangulation methods. Statistical models were applied to forecast trends, while competitive benchmarking provided insights into market positioning.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Consumer Behavior and Premium Product Segments

Mandy Davis is a market research analyst with 7–9 years of experience specializing in consumer goods and services markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.