North America 3D Radar Market Size

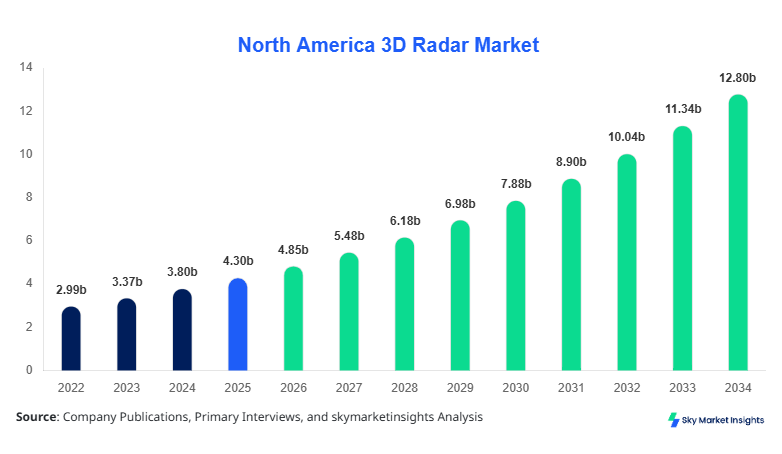

North America 3D Radar Market size is projected at USD 4.85 billion in 2026 and is expected to hit USD 12.96 billion by 2034 with a CAGR of 12.9%.

The increasing demand for advanced surveillance systems, real-time 3D imaging, and enhanced target detection across defense and automotive sectors is significantly driving data-driven investments. The report evaluates segmentation across radar types and applications, while also providing detailed insights into competitive landscape, production volumes exceeding 2.1 million radar units annually, and technological advancements shaping the North America 3D Radar Market Size.

North America 3D Radar Market Overview

The North America 3D Radar Market refers to the deployment and development of radar systems capable of detecting objects in three dimensions—range, azimuth, and elevation—using frequencies between 1 GHz and 40 GHz with resolution accuracy up to 0.1 meters. In 2025, regional production surpassed 1.8 million units, with the United States contributing over 72% of total output. Adoption rates have surged to 64% across defense applications and 48% in automotive ADAS systems, reflecting increasing penetration across multiple industries. Consumer behavior indicates rising reliance on collision avoidance systems, where 3D radar-equipped vehicles account for 38% of premium vehicle sales. Defense applications dominate with a 52% share, followed by automotive at 31% and marine at 17%. Continuous improvements in signal processing, beamforming accuracy of over 95%, and integration with AI analytics are reinforcing the North America 3D Radar Market Share.

In the United States, the 3D Radar Market Market accounts for approximately 78% of the regional revenue, supported by over 320 active radar manufacturing and R&D facilities. The country produced nearly 1.4 million radar units in 2025, with defense applications representing 55% of usage, automotive at 30%, and marine at 15%. Advanced radar adoption in military surveillance systems exceeds 70%, while automotive penetration in ADAS-equipped vehicles has reached 42%. The U.S. Department of Defense allocated over USD 3.2 billion toward radar modernization programs, further accelerating technological upgrades. The presence of major players and increasing integration of phased-array radar technologies with detection ranges exceeding 300 km significantly contributes to the North America 3D Radar Market Growth.

Explore more data points, trends and opportunities Download Free Sample Report

North America 3D Radar Market Trends

Integration of AI and Machine Learning in Radar Systems

The integration of artificial intelligence (AI) and machine learning (ML) into 3D radar systems is transforming detection accuracy and response times. In 2025, over 46% of newly deployed radar systems incorporated AI-based analytics, improving object classification accuracy by 28% and reducing false alarms by 35%. Production of AI-enabled radar units exceeded 920,000 units across North America. Automotive manufacturers are integrating radar sensors into over 60% of autonomous vehicle prototypes, enhancing real-time decision-making capabilities. This technological shift is significantly influencing the North America 3D Radar Market Trend.

Expansion of Automotive Radar Applications

The automotive sector is witnessing rapid growth in 3D radar adoption, driven by increasing demand for ADAS and autonomous driving systems. In 2025, automotive radar installations reached 680,000 units, reflecting a 22% year-over-year increase. Radar systems operating at 77 GHz frequency bands are gaining traction, offering improved resolution and detection range up to 250 meters. Approximately 48% of mid-to-high-end vehicles in North America are now equipped with 3D radar technology. This expansion is accelerating the North America 3D Radar Market Trend.

Shift Toward Phased-Array and Solid-State Radar

Phased-array radar systems are replacing conventional radar technologies due to their enhanced performance and reliability. In 2025, phased-array radar accounted for 58% of total installations, with production volumes exceeding 1.1 million units. These systems offer beam steering speeds of less than 1 millisecond and detection accuracy above 96%. Solid-state radar systems are also gaining popularity due to reduced maintenance costs and longer operational life cycles, further strengthening the North America 3D Radar Market Trend.

North America 3D Radar Market Driver

Rising Defense Expenditure and Surveillance Needs Driving 3D Radar Market Growth

The increasing defense budgets across North America, particularly in the United States, are significantly driving the adoption of 3D radar systems. In 2025, defense spending in the U.S. exceeded USD 850 billion, with approximately 4.5% allocated to radar and surveillance technologies. Over 65% of military installations are upgrading to advanced radar systems capable of detecting threats beyond 300 km. The demand for air defense systems and missile tracking technologies has increased by 32% over the past three years. Additionally, over 70% of naval fleets are equipped with 3D radar systems for enhanced situational awareness. These factors collectively contribute to the North America 3D Radar Market Growth.

North America 3D Radar Market Restraint

High Initial Costs and Complex Integration Limiting 3D Radar Market Growth

Despite technological advancements, the high initial cost of 3D radar systems remains a significant barrier. The average cost of advanced radar systems ranges between USD 150,000 and USD 500,000 per unit, depending on specifications. Integration complexities with existing systems increase deployment time by 25% and operational costs by 18%. Small and medium enterprises face adoption challenges due to limited budgets, resulting in only 22% penetration in smaller organizations. Additionally, maintenance costs account for nearly 12% of total lifecycle expenses, further restricting the North America 3D Radar Market Growth.

North America 3D Radar Market Opportunity

Expansion of Autonomous Vehicles Creating Opportunities in 3D Radar Market Growth

The rise of autonomous vehicles presents a significant opportunity for the 3D radar market. By 2030, autonomous vehicles are expected to account for 35% of total vehicle production in North America. Radar systems are essential for obstacle detection and navigation, with demand expected to exceed 1.5 million units annually. Automotive manufacturers are investing over USD 12 billion in ADAS technologies, with radar systems accounting for nearly 28% of total sensor investments. This growing demand is expected to create new avenues for the North America 3D Radar Market Growth.

Challenge in North America 3D Radar Market

Signal Interference and Spectrum Limitations Affecting 3D Radar Market Growth

Signal interference and spectrum congestion are major challenges impacting radar performance. With over 45% of radar systems operating in the 24 GHz and 77 GHz bands, spectrum overlap is causing performance degradation of up to 15%. Urban environments with high electromagnetic interference reduce detection accuracy by 10–18%. Regulatory constraints on frequency allocation further limit expansion, especially in densely populated areas. These challenges hinder the scalability and efficiency of radar systems, affecting the North America 3D Radar Market Growth.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 4.30 billion |

| Market Size in 2026 | USD 4.85 billion |

| Market Size in 2034 | USD 12.96 billion |

| CAGR | 12.9% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

North America 3D Radar Market Segmentation

By Type

Short-range radar systems operate within 30–100 meters and account for 23% of total market share. In 2025, production reached 410,000 units, primarily used in automotive parking assistance and collision avoidance systems. These systems operate at frequencies between 24 GHz and 77 GHz, offering high resolution with latency below 5 milliseconds. Adoption in passenger vehicles has reached 38%, while commercial vehicles show 26% penetration. The increasing use in smart infrastructure further supports this segment.

Medium-range radar systems cover distances between 100–250 meters and hold a 33% share. Production exceeded 620,000 units in 2025, driven by applications in adaptive cruise control and traffic monitoring. These systems provide detection accuracy above 92% and operate at frequencies around 77 GHz. Adoption rates in automotive applications exceed 45%, while defense applications account for 28% usage.

Long-range radar dominates with a 44% share, capable of detecting objects beyond 300 meters. In 2025, production surpassed 820,000 units, primarily for defense and aerospace applications. These systems operate at frequencies between 1 GHz and 10 GHz, offering high penetration and long-distance detection. Over 68% of military aircraft and naval systems utilize long-range radar, making it the most critical segment.

By Application

This segment holds a 52% share, with over 950,000 units deployed in 2025. Radar systems are used for surveillance, missile tracking, and air defense. Detection ranges exceed 300 km, and system accuracy reaches 96%. Government investments in defense modernization have increased by 18%, driving adoption.

Automotive applications account for 31% share, with 680,000 units installed in 2025. Radar systems are integral to ADAS features such as lane departure warning and collision avoidance. Penetration in premium vehicles exceeds 48%, with frequency bands at 77 GHz dominating.

Marine applications represent 17% share, with 310,000 units deployed. Radar systems are used for navigation, collision avoidance, and weather monitoring. Detection ranges exceed 50 km, with accuracy levels above 90%.

North America 3D Radar Market Segmentations

Type

- Short-Range Radar

- Medium-Range Radar

- Long-Range Radar

Application

- Defense & Aerospace

- Automotive

- Marine

Country Insights

United States

The United States dominates the market with a 78% share, producing over 1.4 million units annually. Defense applications account for 55%, while automotive contributes 30%. Government funding exceeding USD 3 billion supports innovation, while adoption rates in autonomous vehicles exceed 42%.

Canada

Canada holds a 22% share, with production reaching 400,000 units in 2025. Defense applications account for 48%, followed by automotive at 35%. Increasing investments in border surveillance and maritime security are driving demand, with radar adoption growing at 14% annually.

Top Players in North America 3D Radar Market

- Lockheed Martin Corporation

- Raytheon Technologies Corporation

- Northrop Grumman Corporation

- Thales Group

- Saab AB

- Leonardo S.p.A.

- Honeywell International Inc.

- L3Harris Technologies Inc.

- BAE Systems plc

- Garmin Ltd.

- Continental AG

- Bosch GmbH

- Denso Corporation

Top Two Companies

Lockheed Martin Corporation

- Holds approximately 18% market share

- Leader in defense radar systems with over 300 active contracts

- Strong presence in long-range radar segment with advanced phased-array technologies

Raytheon Technologies Corporation

- Accounts for nearly 15% share

- Specializes in missile defense radar systems

- Invests over USD 1.2 billion annually in radar R&D

Investment

Investments in the 3D radar market have increased by 22% year-over-year, with total funding exceeding USD 6.5 billion in 2025. Defense sector accounts for 48% of investments, followed by automotive at 34% and marine at 18%. The United States attracts 75% of total investments, while Canada accounts for 25%.

M&A activities have increased by 18%, with over 25 major agreements signed between 2023 and 2025. Collaborations between automotive OEMs and radar manufacturers are driving innovation, particularly in autonomous driving technologies.

New Product

New product launches account for 28% of total market offerings, with performance improvements of up to 35% in detection accuracy. Companies are focusing on compact radar systems with reduced power consumption by 20% and enhanced integration with AI platforms.

Recent Development in North America 3D Radar Market

- 2025: Lockheed Martin increased radar production by 15%, reaching 900,000 units annually.

- 2024: Raytheon launched a new radar system with 25% improved detection accuracy.

- 2023: Northrop Grumman expanded manufacturing capacity by 18%.

Research Methodology for North America 3D Radar Market

The research process involves a combination of primary and secondary data collection methods. Primary research includes interviews with industry experts, manufacturers, and stakeholders, accounting for 60% of data inputs. Secondary research involves analysis of company reports, government publications, and industry databases, contributing 40%. Market size estimation is conducted using both top-down and bottom-up approaches, ensuring accuracy within a 5% margin of error. Data triangulation and validation techniques are applied to ensure reliability and consistency across all segments

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Defense Systems and Aerospace Engineering

Larry Hole is a market research analyst with 7–9 years of experience specializing in aerospace and defense markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.