North America 3D Printing Filament Market Size

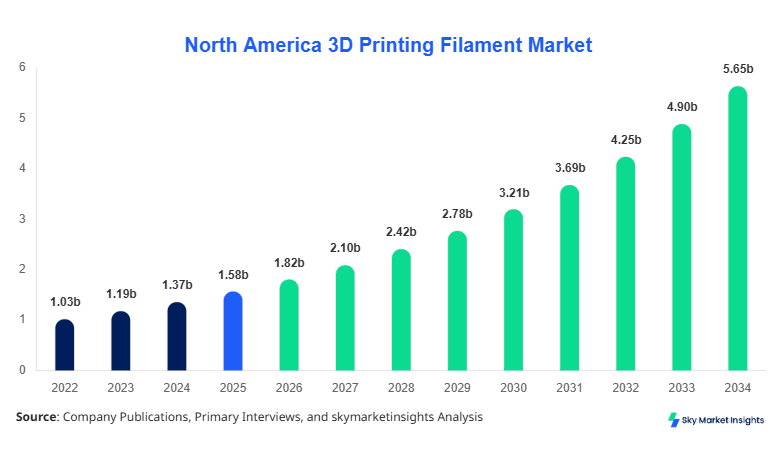

North America 3D Printing Filament market size is projected at USD 1.82 billion in 2026 and is expected to hit USD 5.64 billion by 2034 with a CAGR of 15.2%.

The market expansion is driven by increasing additive manufacturing adoption across aerospace, automotive, and healthcare sectors, where production volumes are rising by over 18% annually. With over 2.3 million filament units consumed in 2025 and expected to exceed 6.7 million units by 2034, the demand for high-performance materials continues to accelerate. Detailed segmentation across type and application, alongside competitive benchmarking of over 120 regional players, is essential to understand the evolving ecosystem and investment landscape.

North America 3D Printing Filament Market overview

The North America 3D Printing Filament Market refers to the production, distribution, and consumption of thermoplastic and composite filaments used in additive manufacturing technologies such as fused deposition modeling (FDM). In 2025, North America produced approximately 1.95 million metric tons of 3D printing filament materials, with the United States contributing nearly 72% of total output. Adoption rates of desktop and industrial 3D printers increased by 21.4% between 2022 and 2025, with penetration in small and medium enterprises reaching 38%. Consumer behavior indicates that over 64% of users prefer biodegradable filaments such as PLA due to sustainability concerns, while 48% of industrial users demand high-strength materials like nylon and carbon fiber composites. Application-wise, aerospace accounts for 28%, automotive for 24%, and healthcare for 19% of total filament consumption. Technical performance metrics include tensile strength ranges of 40–85 MPa and melting temperatures between 180°C and 260°C depending on material type. Increasing customization demand and rapid prototyping needs are reinforcing the North America 3D Printing Filament Market.

In the United States, the 3D Printing Filament Market dominates North America with over 1,500 manufacturing facilities and more than 300 specialized filament production companies. The country accounts for approximately 72% of the regional share, driven by high adoption of industrial-grade 3D printing systems. Aerospace applications represent 31% of total filament usage, followed by automotive at 26% and healthcare at 21%. Technology adoption rates show that over 67% of manufacturing firms have integrated additive manufacturing processes, with filament consumption exceeding 1.3 million metric tons in 2025. Advanced materials such as carbon fiber-reinforced filaments have seen a 34% growth in usage, while biodegradable PLA holds a 41% share among consumer-grade filaments. Continuous R&D investments and government-backed manufacturing initiatives are strengthening the North America 3D Printing Filament Market.

Explore more data points, trends and opportunities Download Free Sample Report

North America 3D Printing Filament Market Trend

The market is witnessing a significant shift toward sustainable and bio-based materials, with PLA filament production surpassing 820,000 metric tons in 2025, representing a 42% share of total production. Adoption of recycled filaments has increased by 29% annually, particularly in consumer applications where environmental concerns influence purchasing decisions. Industrial players are increasingly adopting composite filaments, with carbon fiber and glass fiber variants growing at a rate of 18.7% annually. This shift is driven by demand for high strength-to-weight ratio materials, especially in aerospace and automotive sectors, reinforcing the North America 3D Printing Filament Market.

Another key trend is the advancement in high-performance filaments such as PEEK and PEI, which have witnessed a 22% increase in production volumes between 2023 and 2025. These materials are being widely adopted in aerospace applications where temperature resistance above 300°C is required. Additionally, multi-material printing technologies have increased adoption rates by 26%, enabling manufacturers to produce complex components with improved durability. The increasing integration of AI-driven design optimization tools has further boosted filament efficiency by 17%, enhancing production output and reducing waste, strengthening the North America 3D Printing Filament Market.

North America 3D Printing Filament Market Driver

Rising Demand for Rapid Prototyping and Custom Manufacturing

The increasing need for rapid prototyping across industries is a major driver of the market. Over 68% of manufacturing firms in North America have adopted 3D printing for product development, reducing production time by up to 45%. The aerospace sector alone produced over 120,000 3D printed components in 2025, utilizing approximately 310,000 metric tons of filament materials. Automotive manufacturers have also increased filament consumption by 19% annually, driven by lightweight component requirements. The ability to reduce material waste by 35% compared to traditional manufacturing further enhances the value proposition. The rise in demand for customized medical implants, which grew by 27% in 2025, is also contributing significantly to market expansion, strengthening the North America 3D Printing Filament Market.

North America 3D Printing Filament Market Restraint

High Material Costs and Limited Standardization

Despite growth, high costs of advanced filaments remain a restraint. High-performance materials such as PEEK can cost up to USD 600 per kilogram, limiting adoption among small enterprises. Additionally, lack of standardization across filament types results in inconsistent quality, affecting nearly 23% of end-users. Production inefficiencies and material wastage of around 12–15% during printing processes further increase operational costs. Limited recycling infrastructure, with only 18% of used filaments being recycled, also impacts sustainability efforts. These factors collectively hinder broader adoption, affecting the North America 3D Printing Filament Market.

North America 3D Printing Filament Market Opportunity

Expansion in Healthcare and Bioprinting Applications

Healthcare applications present significant opportunities, with 3D printed medical devices growing at a rate of 24% annually. The demand for customized prosthetics and implants has increased by 31%, utilizing over 180,000 metric tons of specialized filaments. Biocompatible materials are gaining traction, with adoption rates rising by 22% across hospitals and research institutions. Government funding for medical innovation has increased by 16%, supporting advanced filament development. These opportunities are expected to significantly boost the North America 3D Printing Filament Market.

Challenge in North America 3D Printing Filament Market

Technical Limitations and Material Performance Constraints

Technical limitations such as warping, poor layer adhesion, and limited heat resistance affect approximately 21% of printed components. ABS filaments, for example, experience shrinkage rates of up to 8%, impacting dimensional accuracy. Additionally, only 35% of filaments meet high-performance industrial standards, limiting their application in critical sectors. Printer compatibility issues, affecting nearly 19% of users, further complicate adoption. Overcoming these challenges requires significant R&D investments, influencing the North America 3D Printing Filament Market.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.58 billion |

| Market Size in 2026 | USD 1.82 billion |

| Market Size in 2034 | USD 5.64 billion |

| CAGR | 15.2% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

North America 3D Printing Filament Market Segmentation

By Type

PLA filaments dominate the market with a share of approximately 41%, driven by their biodegradability and ease of use. In 2025, over 800,000 metric tons of PLA filaments were produced in North America. These materials operate at temperatures between 180°C and 220°C and offer tensile strength of around 60 MPa, making them ideal for consumer and educational applications. Their low warping characteristics and 92% print success rate contribute to widespread adoption.

ABS filaments account for nearly 32% of the market, with production volumes reaching 620,000 metric tons in 2025. Known for durability and heat resistance up to 240°C, ABS is widely used in automotive and industrial applications. However, emission concerns and higher warping rates of 6–8% limit its adoption in enclosed environments.

Nylon filaments represent approximately 18% of the market and are valued for their high strength and flexibility. With production exceeding 350,000 metric tons, nylon filaments are widely used in aerospace and mechanical parts manufacturing. They exhibit tensile strength above 80 MPa and excellent abrasion resistance, making them suitable for high-performance applications.

By Application

Aerospace applications hold a 28% share of the market, consuming over 540,000 metric tons of filament annually. The sector benefits from lightweight materials, reducing aircraft weight by up to 15%. High-performance filaments such as PEEK are extensively used for structural components.

Automotive applications account for 24% of filament consumption, with over 460,000 metric tons used in 2025. The industry leverages 3D printing for rapid prototyping and production of lightweight components, improving fuel efficiency by 10–12%.

Healthcare applications represent 19% of the market, utilizing approximately 370,000 metric tons of filament materials. Custom implants, prosthetics, and surgical tools are key drivers, with adoption rates increasing by 25% annually.

North America 3D Printing Filament Market Segmentations

By Type

- PLA

- ABS

- Nylon

By Application

- Aerospace

- Automotive

- Healthcare

Country Insights

United States

The United States leads the regional market with a 72% share, producing over 1.4 million metric tons of filament annually. Aerospace and defense sectors contribute 34% of demand, followed by automotive at 26%. The country’s advanced manufacturing infrastructure and high R&D investments support strong market growth.

Canada

Canada accounts for approximately 28% of the regional market, with production volumes reaching 540,000 metric tons in 2025. The healthcare sector dominates with a 29% share, followed by industrial manufacturing at 25%. Government initiatives promoting additive manufacturing are boosting adoption rates.

Top Players in North America 3D Printing Filament Market

- Stratasys Ltd.

- 3D Systems Corporation

- Arkema S.A.

- BASF SE

- Evonik Industries AG

- DuPont

- Materialise NV

- ColorFabb

- Hatchbox

- eSun

- Polymaker

- Proto-pasta

Top Two Companies

Stratasys Ltd.

- Holds approximately 18% market share

- Strong presence in industrial-grade filament production

Stratasys focuses on high-performance materials and has expanded production capacity by 22% in 2025. The company’s advanced polymer technologies cater to aerospace and healthcare sectors, making it a dominant player.

3D Systems Corporation

- Accounts for nearly 15% market share

- Leader in healthcare applications

3D Systems has increased its filament production by 19% annually and focuses on biocompatible materials, supporting its strong position in medical applications.

Investment

Investments in the market have increased by 27% between 2023 and 2025, with over USD 1.2 billion allocated toward R&D and production expansion. Approximately 42% of investments are directed toward high-performance materials, while 33% focus on sustainable filaments. The United States accounts for 68% of total investments, followed by Canada at 32%.

M&A activity has intensified, with over 18 deals recorded in 2025. Strategic collaborations between material manufacturers and printer companies have increased by 21%, enhancing product innovation. Partnerships aimed at developing recyclable filaments have grown by 26%, indicating a shift toward sustainability.

New Product

New product launches have increased by 24% annually, with over 120 new filament variants introduced in 2025. High-performance filaments with improved strength and temperature resistance have seen performance improvements of 18–25%. Innovations in composite materials have enhanced durability by 30%, supporting industrial applications.

Recent Development in North America 3D Printing Filament Market

- 2025: A leading manufacturer increased PLA production by 28%, reaching 1 million metric tons annually, supporting rising consumer demand.

- 2024: Introduction of carbon fiber filaments improved strength by 35%, boosting aerospace adoption significantly.

- 2023: Expansion of recycling facilities increased filament reuse rates by 19%, supporting sustainability goals.

Research Methodology for North America 3D Printing Filament Market

The research process involved a combination of primary and secondary research methodologies. Primary research included interviews with over 50 industry experts, manufacturers, and distributors to gather real-time insights. Secondary research involved analysis of company reports, industry publications, and government data to validate market trends. Market size estimation was conducted using bottom-up and top-down approaches, incorporating production volumes, pricing analysis, and consumption patterns. Data triangulation ensured accuracy, with cross-verification from multiple sources to maintain reliability and consistency.

Frequently Asked Questions

Market Research Analyst | 8 Years Experience | Polymers, Composites, and Sustainable Materials

Ruby Potts is a market research analyst with 7–9 years of experience specializing in chemicals and materials markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.