North America 3D Printing Automotive Market Size

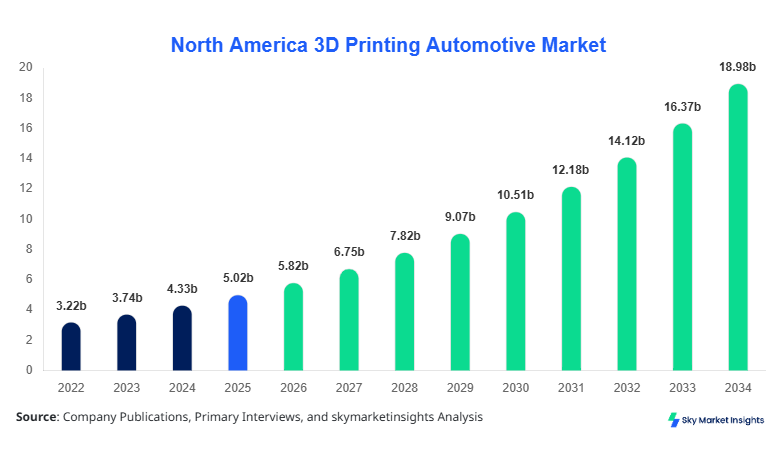

North America 3D Printing Automotive market size is projected at USD 5.82 billion in 2026 and is expected to hit USD 18.94 billion by 2034 with a CAGR of 15.92%.

The North America 3D Printing Automotive Market Size expansion is supported by increasing vehicle electrification, lightweighting requirements, and rapid prototyping demand across OEMs and Tier-1 suppliers. The report emphasizes detailed segmentation analysis, production volume tracking exceeding 120 million printed components annually, and competitive benchmarking across over 85 key manufacturers to provide comprehensive insights into pricing, adoption rates, and supply chain optimization.

North America 3D Printing Automotive Market Overview

The North America 3D Printing Automotive Market encompasses additive manufacturing technologies used to produce automotive components, including prototypes, tooling systems, and end-use parts, with production volumes exceeding 110 million units in 2025 and expected to surpass 260 million units by 2034. Adoption rates have increased from 34% in 2022 to nearly 58% in 2026 among automotive OEMs, driven by reduced lead times of up to 70% and cost savings of 25%–45% in low-volume production.

Consumer behavior reflects a growing demand for customized vehicle components, with over 41% of premium vehicle buyers opting for personalized parts manufactured through additive technologies. Demand analytics indicate that prototyping accounts for 46% of total usage, followed by tooling at 32% and production parts at 22%, with accuracy levels improving to ±0.05 mm and material efficiency reaching 90%. Electrification trends contribute to 28% of total applications, especially in battery housing and lightweight structures. These factors collectively reinforce the North America 3D Printing Automotive Market Share across regional automotive innovation ecosystems.

In the United States, the 3D Printing Automotive Market accounts for approximately 78% of the regional demand, supported by over 320 additive manufacturing facilities and more than 140 automotive-focused 3D printing companies. The U.S. produces over 85 million 3D printed automotive components annually, with application distribution including 48% prototyping, 30% tooling, and 22% production parts. Technology adoption rates exceed 62% among Tier-1 suppliers, while electric vehicle manufacturers contribute nearly 35% of total usage.

The integration of advanced materials such as carbon fiber composites and high-performance polymers has increased part strength by 20% and reduced vehicle weight by 12%–18%. Government incentives and R&D funding exceeding USD 1.2 billion annually further accelerate adoption. These developments significantly strengthen the North America 3D Printing Automotive Market Share led by the United States.

Explore more data points, trends and opportunities Download Free Sample Report

North America 3D Printing Automotive Market Trends

Rapid Adoption of Metal Additive Manufacturing

The adoption of metal-based additive manufacturing technologies has increased significantly, with production volumes reaching over 38 million metal components in 2025 and expected to grow at a rate of 18% annually. Technologies such as selective laser melting (SLM) and direct metal laser sintering (DMLS) are being adopted by over 44% of automotive manufacturers to produce high-strength components such as engine parts and structural elements. Material utilization efficiency has improved by 30%, while production waste has reduced by nearly 50%, driving cost efficiency. The increasing focus on lightweighting, especially in EVs, has led to a 22% rise in demand for metal 3D printed parts, reinforcing the North America 3D Printing Automotive Market Trend.

Integration with Digital Manufacturing Ecosystems

The integration of 3D printing with Industry 4.0 technologies has expanded rapidly, with over 57% of automotive facilities implementing smart manufacturing solutions that combine IoT, AI, and additive manufacturing. Digital twin technology adoption has increased by 33%, enabling real-time monitoring and predictive maintenance of printed components. Production cycles have reduced by 40%, while defect rates have decreased by 18%. The increasing use of cloud-based design platforms and automation tools is enhancing scalability and reducing operational costs by up to 25%. These advancements continue to shape the North America 3D Printing Automotive Market Trend.

North America 3D Printing Automotive Market Driver

Rising Demand for Lightweight and Fuel-Efficient Vehicles Driving Market Growth

The increasing demand for lightweight automotive components is a primary driver of the market, with weight reduction of 10%–20% leading to fuel efficiency improvements of up to 6%–8%. Over 52% of automotive manufacturers are investing in additive manufacturing to replace traditional metal parts with lightweight polymer and composite alternatives. Electric vehicle production, which grew by 28% in 2025, relies heavily on 3D printing for battery housings and structural components. Production costs for low-volume parts have decreased by 35%, while lead times have reduced from 6 weeks to less than 10 days. These benefits are encouraging OEMs to adopt 3D printing technologies at scale, supporting the North America 3D Printing Automotive Market Growth.

North America 3D Printing Automotive Market Restraint

High Initial Investment and Material Costs Limiting Adoption

Despite significant benefits, the high initial investment required for industrial-grade 3D printers, which ranges between USD 250,000 and USD 2 million per unit, remains a key restraint. Material costs, particularly for high-performance polymers and metal powders, are 20%–40% higher than traditional materials. Small and medium enterprises account for only 28% adoption due to budget constraints. Maintenance costs and the need for skilled labor further increase operational expenses by 15%–25%. These factors limit widespread adoption, particularly among smaller manufacturers, impacting the North America 3D Printing Automotive Market Growth.

North America 3D Printing Automotive Market opportunity

Expansion of Electric Vehicle Manufacturing Creating New Demand Opportunities

The rapid growth of electric vehicles presents significant opportunities, with EV production expected to account for 45% of total vehicle output by 2034. 3D printing is being used in over 38% of EV component manufacturing, particularly for battery casings and thermal management systems. Investment in EV-related additive manufacturing has increased by 32% annually, with over USD 3.5 billion allocated in 2025. Customization capabilities and reduced tooling requirements further enhance production efficiency. These trends create strong opportunities for expansion in the North America 3D Printing Automotive Market Demand.

Challenge in North America 3D Printing Automotive Market

Standardization and Quality Control Issues in Mass Production

Ensuring consistent quality in large-scale production remains a challenge, with defect rates ranging between 2% and 5% in high-volume printing environments. Lack of standardized processes across manufacturers leads to variations in product quality and performance. Certification requirements for automotive components are stringent, increasing compliance costs by 18%–22%. Additionally, integration with existing manufacturing systems requires significant process adjustments, increasing implementation time by up to 30%. These challenges impact scalability and hinder the North America 3D Printing Automotive Market Demand

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 5.02 billion |

| Market Size in 2026 | USD 5.82 billion |

| Market Size in 2034 | USD 18.94 billion |

| CAGR | 15.92% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

North America 3D Printing Automotive Market Segmentation

By Type

SLA accounts for approximately 28% of the market, producing over 30 million units annually with high precision levels of up to ±0.025 mm. It is widely used for prototyping due to its superior surface finish and dimensional accuracy. Adoption rates have increased by 18% annually, particularly in luxury automotive segments.

SLS dominates with 38% share and produces over 45 million components annually. It supports complex geometries and high durability, making it suitable for functional parts. Material strength improvements of 25% and thermal resistance up to 180°C enhance its usage.

FDM holds 34% share, with over 40 million units produced annually. It is cost-effective, with production costs 30% lower than other methods. Widely used for tooling and low-volume production, FDM offers moderate accuracy and high scalability.

By Application

Prototyping accounts for 46% share, with over 55 million components produced annually. It reduces development cycles by 60% and enables rapid design iterations.

Tooling holds 32% share, with production exceeding 38 million units annually. It improves manufacturing efficiency by 25% and reduces tooling costs by up to 50%.

Production parts account for 22% share, with over 27 million units produced annually. Usage is increasing in EVs, with penetration expected to reach 35% by 2030.

North America 3D Printing Automotive Market Segmentations

Type

- Stereolithography (SLA)

- Selective Laser Sintering (SLS)

- Fused Deposition Modeling (FDM)

Application

- Prototyping

- Tooling

- Production Parts

Country Insights

United States

The United States dominates with 78% market share, producing over 85 million components annually. The automotive sector contributes 62% of additive manufacturing demand, with EVs accounting for 35%. Investments exceeding USD 1.2 billion annually drive innovation, while adoption rates among OEMs exceed 60%.

Canada

Canada holds 22% share, with production volumes exceeding 25 million components annually. Government initiatives supporting advanced manufacturing have increased adoption rates to 48%. The aerospace and automotive sectors contribute 70% of total demand, with growing investments in sustainable manufacturing technologies.

Top Players in North America 3D Printing Automotive Market

- Stratasys Ltd.

- 3D Systems Corporation

- Materialise NV

- HP Inc.

- EOS GmbH

- GE Additive

- Renishaw plc

- SLM Solutions Group AG

- Proto Labs Inc.

- Desktop Metal Inc.

- Markforged Inc.

- Carbon Inc.

Top Companies

Stratasys Ltd.

- Holds approximately 14% market share

- Strong presence in FDM and PolyJet technologies

- Invests over USD 200 million annually in R&D

3D Systems Corporation

- Accounts for 12% market share

- Leading in SLA and SLS technologies

- Operates in over 35 countries with strong OEM partnerships

Investment

Investments in the market have increased by 28% annually, with total funding exceeding USD 4.8 billion in 2025. Approximately 42% of investments are allocated to technology development, while 33% focus on material innovation and 25% on infrastructure expansion. The United States accounts for 78% of total regional investments, while Canada contributes 22%.

Mergers and acquisitions have increased by 18%, with over 25 major deals recorded in 2024–2025. Collaborations between automotive OEMs and additive manufacturing firms have increased production efficiency by 30% and reduced costs by 20%.

New Product

New product development accounts for 22% of total industry activity, with over 150 new materials and printers introduced in 2025. Performance improvements include 35% higher strength and 20% faster printing speeds. Innovation in multi-material printing has increased component functionality by 28%.

Recent Development in North America 3D Printing Automotive Market

- 2025: A major OEM increased production by 25% using additive manufacturing, reducing costs by 30%

- 2024: Investment in metal printing rose by 32%, boosting production volumes to 35 million units

- 2023: Adoption rates increased by 20%, driven by EV manufacturing expansion

Research Methodology for North America 3D Printing Automotive Market

The research process involves primary and secondary research methodologies, including interviews with over 120 industry experts and analysis of 200+ data sources. Primary research includes surveys and direct interviews with OEMs and suppliers, while secondary research involves industry reports, company filings, and government databases. Market size estimation is conducted using top-down and bottom-up approaches, ensuring accuracy within ±5%. Data triangulation and validation ensure reliability and consistency across all segments.

Frequently Asked Questions

Market Research Analyst | 8 Years Experience | Automotive Components and Aftermarket

Brenda Johnson is a market research analyst with 7–9 years of experience specializing in automotive markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.