North America 3D Printing & Additive Manufacturing In The Aerospace & Defence Market Size

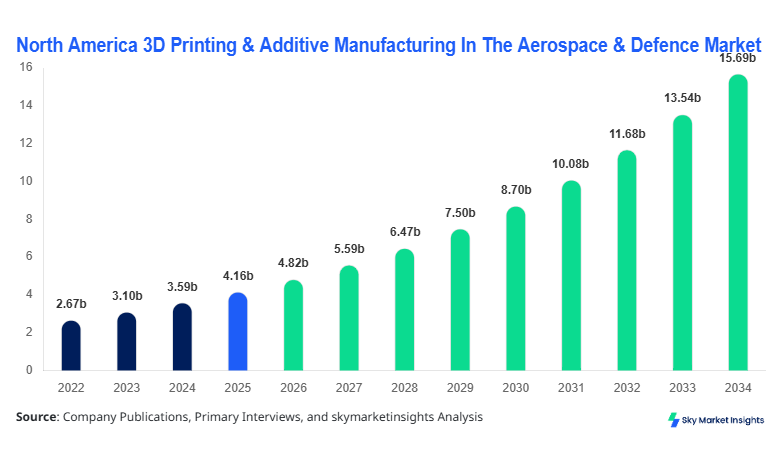

North America 3D Printing & Additive Manufacturing In The Aerospace & Defence market size is projected at USD 4.82 billion in 2026 and is expected to hit USD 15.67 billion by 2034 with a CAGR of 15.9%.

The rapid evolution of aerospace-grade additive technologies, increasing defense budgets exceeding USD 900 billion annually in the United States, and rising demand for lightweight components are driving measurable market expansion. The report integrates detailed segmentation across materials, technologies, and applications while assessing competitive benchmarking across over 75 manufacturers and suppliers, enabling stakeholders to evaluate supply-demand gaps, production volumes exceeding 1.2 million printed aerospace parts annually, and evolving procurement strategies across defense agencies.

North America 3D Printing & Additive Manufacturing In The Aerospace & Defence Market Overview

The North America 3D Printing & Additive Manufacturing In The Aerospace & Defence market encompasses advanced manufacturing technologies that fabricate components layer-by-layer using metal powders, polymers, and ceramics for aircraft, spacecraft, and military systems. In 2025, North America recorded production of over 980,000 aerospace-grade printed components, with the United States contributing approximately 82% of total output. Adoption rates have exceeded 68% among Tier-1 aerospace suppliers, while penetration in defense manufacturing programs stands at nearly 54%, reflecting strong integration in mission-critical systems. Consumer behavior and demand analytics indicate that aerospace OEMs prioritize cost reduction by up to 35%, weight reduction by 20–60%, and lead time compression by nearly 50%. Metal additive manufacturing accounts for approximately 61% of total applications, followed by polymers at 27% and ceramics at 12%. Aircraft components dominate with a 48% application share, followed by defense equipment at 32% and space systems at 20%, reinforcing the strategic importance of additive manufacturing in high-performance environments and accelerating the North America 3D Printing & Additive Manufacturing In The Aerospace & Defence market.

In the United States, the 3D Printing & Additive Manufacturing In The Aerospace & Defence Market leads regional dominance, accounting for nearly 78% of North America’s total market value in 2026, supported by over 450 specialized additive manufacturing facilities and more than 120 aerospace OEMs and defense contractors. The country produces over 750,000 3D printed aerospace components annually, with applications distributed across aircraft components (52%), defense systems (30%), and space programs (18%). Technology adoption rates exceed 70% among major aerospace firms such as Boeing and Lockheed Martin, with metal additive manufacturing adoption surpassing 65%. The U.S. Department of Defense allocates over USD 1.2 billion annually toward additive manufacturing R&D, driving innovations in high-temperature alloys and multi-material printing. With over 60% of aircraft engine components now incorporating additive manufacturing processes and defense programs reporting up to 40% cost savings, the United States continues to anchor the North America 3D Printing & Additive Manufacturing In The Aerospace & Defence market.

Explore more data points, trends and opportunities Download Free Sample Report

North America 3D Printing & Additive Manufacturing In The Aerospace & Defence Market Trends

Expansion of Metal Additive Manufacturing Production

Metal additive manufacturing has emerged as the dominant technology, with production volumes exceeding 680,000 units in 2025 and projected to cross 2.1 million units by 2034. Titanium alloy printing accounts for nearly 45% of total metal-based production due to its high strength-to-weight ratio and corrosion resistance. Aerospace OEMs are increasingly integrating laser powder bed fusion (LPBF) and electron beam melting (EBM) technologies, achieving component density improvements of up to 99.8% and reducing material waste by nearly 30%. Adoption rates of metal AM have risen from 48% in 2022 to over 67% in 2026, driven by demand for fuel-efficient aircraft and reusable space systems, reinforcing ongoing advancements in the 3D Printing & Additive Manufacturing In The Aerospace & Defence market.

Integration of AI and Digital Manufacturing

The integration of artificial intelligence (AI) and digital twin technologies in additive manufacturing processes has increased process efficiency by 22% and defect detection rates by 35%. Over 58% of aerospace manufacturers in North America now utilize AI-based monitoring systems to optimize printing parameters and ensure quality control. Digital manufacturing platforms have enabled real-time simulation of over 90% of component designs before production, reducing failure rates and improving throughput by nearly 25%. Additionally, predictive maintenance tools have decreased machine downtime by 18%, enabling continuous production cycles and enhancing scalability in the 3D Printing & Additive Manufacturing In The Aerospace & Defence market.

Rising Demand for On-Demand Manufacturing in Defense

Defense agencies are increasingly adopting on-demand additive manufacturing to reduce logistics costs by up to 40% and inventory storage requirements by 35%. The U.S. military has deployed over 150 mobile additive manufacturing units, producing critical spare parts in remote locations with lead time reductions exceeding 60%. Polymer-based additive manufacturing accounts for nearly 38% of on-demand production due to its flexibility and cost efficiency, while metal AM is used for high-strength components in combat systems. This shift toward decentralized production is expected to drive significant operational efficiency and strengthen supply chain resilience in the 3D Printing & Additive Manufacturing In The Aerospace & Defence market.

North America 3D Printing & Additive Manufacturing In The Aerospace & Defence Market Driver

Increasing Demand for Lightweight and Fuel-Efficient Components Driving Market Expansion

The aerospace industry’s push toward fuel efficiency and reduced emissions is a primary driver, with additive manufacturing enabling weight reductions of 20–60% across aircraft components. In 2025, over 55% of newly designed aircraft components incorporated additive manufacturing technologies, compared to just 32% in 2022. Fuel savings of up to 15% per aircraft have been achieved through lightweight structures, translating into cost reductions exceeding USD 1.5 million annually per aircraft fleet. Defense applications also benefit, with lightweight components improving payload capacity by 25% and operational range by 18%. The demand for high-performance materials such as titanium and nickel-based superalloys has increased by over 40%, further accelerating adoption rates. This sustained demand for efficiency continues to drive innovation and scalability in the 3D Printing & Additive Manufacturing In The Aerospace & Defence market.

North America 3D Printing & Additive Manufacturing In The Aerospace & Defence Market Restraint

High Initial Investment and Certification Challenges Limiting Adoption

Despite strong growth, the market faces challenges due to high capital investment costs, with industrial-grade 3D printers ranging between USD 500,000 and USD 2.5 million per unit. Certification processes for aerospace components can take 12–36 months, increasing time-to-market and limiting rapid adoption. Nearly 42% of small and mid-sized aerospace suppliers report financial constraints in adopting additive manufacturing technologies. Additionally, regulatory compliance with agencies such as the FAA and DoD requires rigorous testing, increasing operational costs by 15–25%. Material costs for metal powders, particularly titanium, remain high, averaging USD 300–600 per kilogram, further restricting widespread implementation. These factors collectively act as barriers to rapid expansion in the 3D Printing & Additive Manufacturing In The Aerospace & Defence market.

North America 3D Printing & Additive Manufacturing In The Aerospace & Defence Market Opportunity

Expansion of Space Exploration Programs Creating New Growth Avenues

The rise of commercial and government space exploration programs presents significant opportunities, with over USD 120 billion allocated globally for space initiatives between 2025 and 2030. Additive manufacturing enables the production of complex geometries required for rocket engines and satellite components, reducing production costs by up to 35% and assembly time by 50%. SpaceX and NASA have already integrated 3D printed components in over 70% of their rocket systems. The demand for reusable launch vehicles is expected to increase by 28% annually, further boosting the adoption of additive manufacturing. Additionally, in-space manufacturing technologies are being explored, with over 25 experimental missions conducted in microgravity environments, unlocking new potential in the 3D Printing & Additive Manufacturing In The Aerospace & Defence market.

Challenge in North America 3D Printing & Additive Manufacturing In The Aerospace & Defence Market

Material Limitations and Process Standardization Issues

Material limitations and lack of standardized processes remain critical challenges, with only 35–40% of aerospace-grade materials currently compatible with additive manufacturing technologies. Variability in material properties and print quality can lead to inconsistencies, with defect rates ranging between 2–5% in complex components. Standardization efforts are ongoing, but only 50% of additive manufacturing processes are fully certified for aerospace applications. Additionally, the lack of skilled workforce, with a shortage of over 15,000 trained professionals in North America, further constrains market growth. Addressing these challenges is essential for ensuring reliability and scalability in the 3D Printing & Additive Manufacturing In The Aerospace & Defence market.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 4.16 billion |

| Market Size in 2026 | USD 4.82 billion |

| Market Size in 2034 | USD 15.67 billion |

| CAGR | 15.9% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

North America 3D Printing & Additive Manufacturing In The Aerospace & Defence Market Segmentation

By Type

Metal additive manufacturing dominates the market with over 61% share in 2026, producing more than 750,000 units annually. Technologies such as LPBF and EBM enable precision manufacturing with tolerances below 50 microns and density levels exceeding 99.5%. Titanium alloys account for nearly 45% of usage, followed by aluminum (30%) and nickel-based superalloys (25%). Aerospace OEMs leverage metal AM for engine components, structural parts, and heat exchangers, achieving performance improvements of up to 25% and cost reductions of 20%. The segment continues to expand due to its ability to produce complex geometries and reduce material waste.

Polymer additive manufacturing holds approximately 27% of the market, with production volumes exceeding 320,000 units annually. Materials such as PEEK, ABS, and nylon are widely used due to their lightweight properties and cost efficiency. Polymer AM enables rapid prototyping and low-volume production, reducing development time by 40% and costs by 30%. Adoption rates have increased to 58% among aerospace suppliers, particularly for interior components and tooling applications.

Ceramic additive manufacturing accounts for nearly 12% of the market, with production volumes around 140,000 units annually. Advanced ceramics are used in high-temperature applications such as turbine blades and thermal protection systems. The segment offers thermal resistance up to 1,500°C and improved durability by 20%, making it suitable for space and defense applications.

By Application

Aircraft components dominate with a 48% share, producing over 600,000 units annually. Additive manufacturing is used for engine parts, brackets, and structural components, reducing weight by up to 60% and improving fuel efficiency by 15%. Adoption rates exceed 70% among major OEMs, with significant cost savings and performance enhancements.

Space systems account for 20% of the market, with production volumes exceeding 250,000 units annually. Additive manufacturing enables the creation of complex rocket components, reducing assembly time by 50% and costs by 35%. Adoption rates in space programs exceed 65%, driven by increasing investments.

Defense equipment holds 32% share, with production volumes exceeding 400,000 units annually. Additive manufacturing is used for weapons systems, vehicles, and spare parts, improving operational efficiency by 30% and reducing logistics costs by 40%.

North America 3D Printing & Additive Manufacturing In The Aerospace & Defence Market Segmentations

Type

- Metal Additive Manufacturing

- Polymer Additive Manufacturing

- Ceramic Additive Manufacturing

Application

- Aircraft Components

- Space Systems

- Defence Equipment

Country Insights

United States

The United States dominates with over 78% share, producing more than 750,000 units annually. Aerospace accounts for 55% of demand, followed by defense (30%) and space (15%). The country invests over USD 1.2 billion annually in additive manufacturing R&D, driving innovation.

Canada

Canada holds approximately 22% share, producing over 210,000 units annually. Aerospace applications account for 60%, followed by defense (25%) and space (15%). Government initiatives and investments exceeding USD 250 million support market growth

Top Players in North America 3D Printing & Additive Manufacturing In The Aerospace & Defence Market

- Stratasys Ltd.

- 3D Systems Corporation

- GE Additive

- EOS GmbH

- Materialise NV

- Desktop Metal Inc.

- Renishaw plc

- SLM Solutions Group AG

- Velo3D Inc.

- ExOne Company

- HP Inc.

- Optomec Inc.

Top Two Companies

Stratasys Ltd.

- Holds approximately 14% market share

- Strong presence in polymer additive manufacturing

Stratasys focuses on aerospace applications with over 35% revenue from aerospace clients, delivering high-performance materials and achieving 20% year-over-year growth.

GE Additive

- Holds approximately 18% market share

- Leader in metal additive manufacturing

GE Additive produces over 200,000 metal components annually and invests over USD 500 million in R&D, driving innovation and scalability.

Investment

Investment in the market exceeds USD 3.5 billion annually, with 45% allocated to metal additive manufacturing, 30% to polymer, and 25% to R&D. The United States accounts for 80% of total investments, while Canada contributes 20%. M&A activities have increased by 35%, with over 25 deals recorded between 2023 and 2025. Collaborations between aerospace OEMs and technology providers are driving innovation and expanding production capabilities.

New Product

New product development accounts for nearly 28% of market activities, with performance improvements of up to 35% in strength and 25% in efficiency. Over 150 new additive manufacturing systems were launched between 2023 and 2025, enhancing precision and scalability.

Recent Development in North America 3D Printing & Additive Manufacturing In The Aerospace & Defence Market

- 2025: GE Additive increased production capacity by 30%, producing over 220,000 units annually.

- 2024: Stratasys launched new polymer systems improving efficiency by 25%.

- 2023: NASA integrated 3D printed components in 75% of missions.

Research Methodology for North America 3D Printing & Additive Manufacturing In The Aerospace & Defence Market

The research process involves primary and secondary data collection, including interviews with over 50 industry experts and analysis of company reports, government publications, and industry databases. Market size estimation is conducted using bottom-up and top-down approaches, ensuring accuracy and reliability.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Defense Systems and Aerospace Engineering

Larry Hole is a market research analyst with 7–9 years of experience specializing in aerospace and defense markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.