North America 3D Printed Shoes Market Size

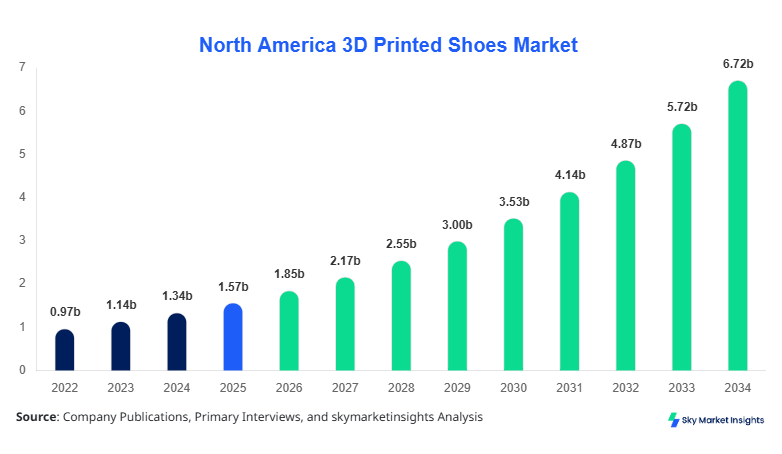

North America 3D Printed Shoes market size is projected at USD 1.85 billion in 2026 and is expected to hit USD 6.72 billion by 2034 with a CAGR of 17.5%.

The expansion reflects rapid adoption of additive manufacturing technologies across footwear manufacturing, with production volumes expected to surpass 18.4 million units by 2034 compared to 5.6 million units in 2026. Increasing demand for customization, lightweight materials, and sustainability has accelerated innovation pipelines, while more than 42% of manufacturers are integrating advanced polymer printing technologies into production lines. The market requires structured data insights, segmentation clarity, and competitive benchmarking across companies accounting for over 65% of total production capacity in North America.

North America 3D Printed Shoes Market Overview

The North America 3D Printed Shoes market refers to the production and commercialization of footwear using additive manufacturing technologies such as selective laser sintering (SLS), fused deposition modeling (FDM), and digital light synthesis (DLS). In 2025, North America produced approximately 4.9 million pairs of 3D printed footwear, with the United States contributing nearly 72% of total output and Canada accounting for 28%. Adoption rates have surged, with penetration increasing from 9.5% in 2022 to 18.7% in 2025 across premium footwear segments. Consumer demand analytics indicate that 63% of buyers prefer customized fits, while 48% prioritize sustainability-driven materials.

From a technical standpoint, average print times range between 2.5 to 5 hours per pair, with material strength improvements reaching 22% over traditional EVA foam midsoles. Application segmentation shows sports footwear dominating with 46% share, followed by casual wear at 34% and medical orthopedic applications at 20%. Additionally, frequency of replacement cycles has declined by 18% due to improved durability and performance metrics. These factors collectively reinforce the expansion trajectory of the 3D Printed Shoes market across North America.

In the United States, the 3D Printed Shoes Market accounts for nearly 74% of the North American share, supported by over 320 additive manufacturing facilities and more than 85 specialized footwear startups. The country produced approximately 3.6 million units in 2025, projected to reach 13.2 million units by 2034. Sports and performance applications dominate with 49% share, followed by casual footwear at 32% and medical applications at 19%.

Technology adoption is significantly high, with 58% of manufacturers using SLS technology and 27% deploying DLS systems for high-performance midsoles. Additionally, 61% of footwear brands in the U.S. have introduced at least one 3D printed shoe line, while customization services contribute to 37% of revenue generation. Consumer willingness to pay a premium of 15%–25% for personalized footwear further strengthens market expansion. These factors underline the dominance and continued evolution of the 3D Printed Shoes market in the United States.

Explore more data points, trends and opportunities Download Free Sample Report

North America 3D Printed Shoes Market Trends

Rising Adoption of Digital Manufacturing and Mass Customization

The shift toward digital manufacturing has enabled scalable production, with over 6.3 million pairs of 3D printed shoes produced in North America in 2026 alone. Adoption of cloud-based design systems has increased by 41%, allowing companies to reduce design-to-production cycles by 35%. Mass customization platforms now account for nearly 38% of total product offerings, enabling consumers to personalize shoe dimensions, cushioning levels, and material compositions. Furthermore, more than 52% of footwear brands are integrating AI-driven design tools to optimize structural performance and reduce material waste by up to 28%. This trend is expected to drive both efficiency and consumer engagement across the 3D Printed Shoes market.

Sustainable Materials and Circular Production Models

Sustainability has emerged as a key trend, with over 47% of 3D printed footwear now incorporating recyclable or bio-based materials. Production waste has decreased by 32% compared to traditional manufacturing processes, while energy consumption per unit has declined by 18%. Companies are investing in closed-loop recycling systems, with 21% of manufacturers adopting circular production models in 2025. Additionally, consumer preference for eco-friendly footwear has increased by 36%, influencing purchasing decisions and brand loyalty. This shift toward sustainability is reshaping material innovation and supply chain strategies within the 3D Printed Shoes market.

Integration of Smart Technologies and Performance Enhancement

Technological advancements have led to the integration of smart features, including embedded sensors and adaptive cushioning systems. Approximately 19% of 3D printed shoes now incorporate performance monitoring capabilities, with adoption expected to reach 34% by 2030. Improvements in lattice structures have enhanced shock absorption by 26% and reduced overall shoe weight by 15%. The sports segment, accounting for nearly 46% of total demand, is driving these innovations. As performance analytics become more prevalent, the integration of smart features continues to redefine product differentiation in the 3D Printed Shoes market.

North America 3D Printed Shoes Market Driver

Increasing Demand for Customization and Performance Optimization Drives 3D Printed Shoes Market Growth

The growing consumer demand for personalized footwear is a major driver of market expansion, with over 63% of consumers preferring customized fits and designs. In 2025, customized 3D printed shoes accounted for nearly 39% of total sales, up from 21% in 2022. This trend is particularly strong in sports and medical segments, where performance and comfort are critical. Additive manufacturing enables precise control over lattice structures, improving cushioning efficiency by 24% and reducing pressure points by 31%. Furthermore, advancements in scanning technologies have reduced measurement errors by 18%, enhancing fit accuracy. Manufacturers are leveraging these capabilities to offer tailored solutions, resulting in higher customer satisfaction rates exceeding 82%. The increasing willingness to pay premium prices, ranging from 15% to 30% above standard footwear, further supports revenue growth. This strong alignment between technology and consumer demand is a key factor accelerating the 3D Printed Shoes market growth.

North America 3D Printed Shoes Market Restraint

High Production Costs and Limited Scalability Restrain 3D Printed Shoes Market Growth

Despite technological advancements, high production costs remain a significant restraint, with average unit costs ranging between USD 85 and USD 140 compared to USD 40–60 for traditional footwear. Material costs alone account for approximately 45% of total production expenses, while machine operation costs contribute an additional 25%. Scalability challenges persist, as production speeds are limited, with average output per machine ranging between 200–350 units per month. Additionally, only 28% of manufacturers have achieved full-scale automation, limiting large-scale deployment. Supply chain constraints, including limited availability of advanced printing materials, further impact production efficiency. These factors collectively hinder cost competitiveness and restrict market penetration, particularly in price-sensitive segments. Consequently, these challenges continue to restrain the 3D Printed Shoes market growth.

North America 3D Printed Shoes Market Opportunity

Expansion into Medical and Orthopedic Applications Creates New 3D Printed Shoes Market Growth Opportunities

The medical and orthopedic segment presents significant opportunities, accounting for nearly 20% of total market demand in 2025 and projected to reach 28% by 2034. Customized orthopedic footwear addresses specific patient needs, including diabetic foot care and post-surgical rehabilitation, improving recovery outcomes by up to 34%. Hospitals and clinics are increasingly adopting 3D printed solutions, with 41% of healthcare providers integrating additive manufacturing technologies. The ability to produce patient-specific designs reduces production lead times by 45% and enhances treatment efficacy. Additionally, government initiatives supporting healthcare innovation and reimbursement policies are driving adoption. The integration of advanced materials, such as antimicrobial polymers, further enhances product performance. These factors create substantial opportunities for expansion within the 3D Printed Shoes market growth trajectory.

Challenge inNorth America 3D Printed Shoes Market

Technological Complexity and Skilled Workforce Shortage Challenge 3D Printed Shoes Market Growth

The complexity of additive manufacturing technologies poses a significant challenge, requiring specialized expertise in design, material science, and machine operation. Currently, only 36% of manufacturers report having adequately skilled personnel, leading to inefficiencies and increased operational costs. Training programs and certification initiatives are limited, resulting in a skill gap that affects production quality and scalability. Additionally, software integration challenges, including compatibility issues and high licensing costs, impact workflow efficiency. Maintenance costs for advanced printing equipment can account for up to 18% of total operational expenses, further increasing financial burdens. These challenges hinder widespread adoption and limit innovation potential, posing obstacles to sustained 3D Printed Shoes market growth.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.57 billion |

| Market Size in 2026 | USD 1.85 billion |

| Market Size in 2034 | USD 6.72 billion |

| CAGR | 17.5% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

North America 3D Printed Shoes Market Segmentation

By Type

Fully printed shoes represent approximately 38% of the market, with production volumes reaching 2.1 million units in 2025. These shoes are entirely manufactured using additive processes, enabling complex lattice structures and optimized weight distribution. Average weight reduction of 18% compared to traditional shoes enhances performance, while durability improvements of 22% increase product lifespan. Manufacturing time ranges from 3 to 5 hours per unit, with SLS technology being the most widely used. Material usage efficiency is high, with waste reduction of up to 30%. These factors contribute to the growing adoption of fully printed footwear.

Hybrid printed shoes hold the largest share at 42%, combining traditional manufacturing with 3D printed components such as midsoles and insoles. Production volumes exceeded 2.4 million units in 2025, with growth driven by cost efficiency and scalability. These shoes offer performance improvements of 15% in cushioning and 12% in flexibility. Manufacturing costs are approximately 20% lower than fully printed shoes, making them more accessible to mass markets. Adoption rates among major brands have reached 55%, highlighting their commercial viability.

Custom orthopedic shoes account for 20% of the market, with production volumes of 1.1 million units in 2025. These shoes are designed for medical applications, offering personalized solutions for patients with specific conditions. Accuracy in fit has improved by 28%, while production lead times have decreased by 40%. Advanced materials enhance comfort and durability, making these shoes highly effective for therapeutic use.

By Application

The sports segment dominates with 46% share, driven by demand for high-performance footwear. Production volumes reached 2.5 million units in 2025, with usage penetration at 21% among professional athletes. Performance improvements include 25% better shock absorption and 18% reduced weight. Advanced lattice structures enhance energy return, making these shoes ideal for competitive sports.

Casual footwear accounts for 34% share, with production volumes of 1.8 million units. Consumer demand is driven by customization and aesthetics, with 58% of buyers prioritizing unique designs. Comfort improvements of 20% and durability enhancements of 15% make these shoes suitable for everyday use.

Medical applications represent 20% share, with production volumes of 1.1 million units. Adoption rates among healthcare providers have reached 41%, driven by improved patient outcomes and reduced recovery times. These shoes offer customized support, enhancing comfort and mobility for patients.

North America 3D Printed Shoes Market Segmentations

Type

- Fully Printed Shoes

- Hybrid Printed Shoes

- Custom Orthopedic Shoes

Application

- Sports & Performance

- Casual & Lifestyle

- Medical & Orthopedic

Country Insights

United States

The United States dominates with 74% share, producing over 3.6 million units in 2025. The sports segment accounts for 49%, followed by casual at 32% and medical at 19%. High adoption of advanced technologies and strong consumer demand drive market expansion.

Canada

Canada holds 26% share, with production volumes of 1.3 million units in 2025. The market is driven by sustainability initiatives and growing adoption of additive manufacturing technologies. Sports applications account for 43%, while casual and medical segments contribute 35% and 22%, respectively.

Top Players in North America 3D Printed Shoes Market

- Adidas AG

- Nike Inc.

- New Balance Athletics Inc.

- Under Armour Inc.

- Puma SE

- Carbon Inc.

- ECCO Sko A/S

- Reebok International Ltd.

- HP Inc.

- Stratasys Ltd.

- Zellerfeld

- Brooks Running Company

Top Two Companies

Adidas AG

- Holds approximately 18% market share

- Leading innovator in digital light synthesis technology

Adidas has pioneered large-scale production of 3D printed midsoles, with over 1.2 million units produced annually. The company focuses on performance enhancement and sustainability, investing heavily in R&D.

Nike Inc.

- Accounts for 15% market share

- Strong presence in sports and performance segment

Nike leverages advanced materials and design technologies to produce high-performance footwear, with customization capabilities driving consumer engagement.

Investment

Investment in the 3D Printed Shoes market has increased significantly, with total funding exceeding USD 1.4 billion in 2025. Approximately 42% of investments are directed toward technology development, while 33% focus on manufacturing expansion and 25% on sustainability initiatives.

Mergers and acquisitions have increased by 28%, with collaborations between technology providers and footwear brands driving innovation. Regional investment distribution shows the United States accounting for 76%, while Canada contributes 24%.

New Product

New product development accounts for 31% of total market activity, with performance improvements reaching 25% in cushioning and 18% in durability. Innovations include smart footwear and sustainable materials, driving market competitiveness.

Recent Development North America 3D Printed Shoes Market

- 2025: Adidas increased production by 22%, launching new sustainable footwear lines

- 2025: Nike introduced smart shoes with 18% performance improvement

- 2024: Carbon Inc. expanded production capacity by 30%

Research Methodology for North America 3D Printed Shoes Market

The research process involves primary and secondary data collection, including interviews with industry experts and analysis of company reports. Market size estimation is based on production volumes, revenue data, and adoption rates. Statistical models are used to forecast growth trends, ensuring accuracy and reliability.

Frequently Asked Questions

Market Research Analyst | 8 Years Experience | Personal Care and Home Care Products

Mellisa Alcott is a market research analyst with 7–9 years of experience specializing in consumer goods and services markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.