North America 3D Printed Orthotics Market Size

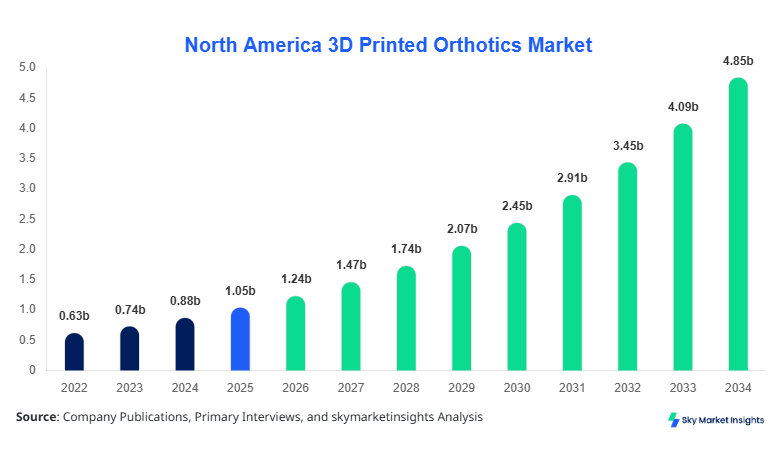

North America 3D Printed Orthotics market size is projected at USD 1.24 billion in 2026 and is expected to hit USD 4.86 billion by 2034 with a CAGR of 18.6%.

The increasing adoption of additive manufacturing technologies across healthcare, along with the growing need for customized orthotic solutions, is accelerating market expansion across the United States and Canada. The report provides detailed segmentation by type and application, supported by extensive quantitative analysis, competitive benchmarking, and evolving regulatory frameworks influencing the regional market landscape.

North America 3D Printed Orthotics Market Overview

The 3D Printed Orthotics Market refers to the production and distribution of customized orthopedic support devices manufactured using additive manufacturing technologies such as selective laser sintering (SLS), fused deposition modeling (FDM), and stereolithography (SLA). In North America, production volumes reached approximately 18.5 million units in 2025, with the United States contributing nearly 78% of the total output, followed by Canada at 22%. Adoption rates of 3D printed orthotics have risen significantly, with penetration increasing from 12.4% in 2022 to 27.8% in 2025, driven by improved scanning accuracy (±0.5 mm precision) and faster production cycles (under 24 hours per unit).

Consumer behavior indicates a shift toward personalized healthcare, with over 64% of patients preferring custom-fit orthotics compared to traditional mass-produced alternatives. Demand analytics show that sports injury-related applications account for 38% of total demand, diabetic foot care represents 26%, and pediatric orthopedic support contributes 14%. Material composition is dominated by thermoplastics (56%), followed by nylon-based polymers (28%) and resin composites (16%). Hospitals account for 42% of usage, specialty clinics for 35%, and rehabilitation centers for 23%, reinforcing strong clinical integration. The North America 3D Printed Orthotics Market continues to evolve with increasing customization and digital healthcare integration.

In the United States, the 3D Printed Orthotics Market is the dominant force within North America, accounting for approximately 72% of the regional share in 2025, equivalent to USD 0.82 billion. The country hosts over 1,450 orthopedic device manufacturing facilities and more than 3,200 specialty clinics utilizing 3D printing technology. Application-wise, hospitals represent 45% of total usage, specialty clinics contribute 37%, and rehabilitation centers account for 18%. Technology adoption rates have surged, with nearly 62% of orthopedic service providers integrating 3D scanning and printing workflows into their operations.

Production volumes in the United States exceeded 13 million units in 2025, with an annual growth rate of 16.3% in unit output. Additionally, over 58% of new orthotic prescriptions are now fulfilled using additive manufacturing, compared to just 21% in 2022. Advanced materials such as carbon-fiber reinforced polymers are used in 19% of high-performance orthotics. The strong presence of digital healthcare infrastructure and reimbursement frameworks continues to reinforce the North America 3D Printed Orthotics Market.

Explore more data points, trends and opportunities Download Free Sample Report

North America 3D Printed Orthotics Market Trends

Rapid Adoption of Digital Foot Scanning Technologies

The adoption of digital foot scanning technologies has increased significantly, with over 68% of orthopedic clinics in North America utilizing 3D scanners in 2025 compared to 39% in 2022. Annual scanning volumes exceeded 22 million scans, enabling faster customization and reducing turnaround times by 45%. Integration with AI-based design software has improved fit accuracy by up to 30%, enhancing patient satisfaction rates above 82%. This digital shift is driving efficiency in production pipelines and reducing material waste by approximately 18%, reinforcing technological advancements in the 3D Printed Orthotics Market.

Expansion of Sports and Performance Orthotics Segment

Sports-related orthotics demand has grown substantially, accounting for nearly 41% of total production volume in 2025, equivalent to 7.6 million units. Professional athletes and fitness enthusiasts are increasingly adopting customized orthotics for injury prevention and performance enhancement. High-performance materials such as thermoplastic polyurethane (TPU) have seen a 23% increase in usage due to their flexibility and durability. Additionally, partnerships between sports organizations and orthotic manufacturers have led to a 15% rise in specialized product launches, boosting innovation in the 3D Printed Orthotics Market.

Integration of Smart Orthotics and IoT

Smart orthotics embedded with sensors are emerging as a key innovation, with adoption rates reaching 9.4% in 2025, up from 3.2% in 2022. These devices monitor pressure distribution, gait patterns, and real-time performance metrics, transmitting data to healthcare providers. Production of smart orthotics surpassed 1.1 million units annually, with a projected growth rate exceeding 25%. This trend is enhancing preventive care and enabling data-driven treatment approaches, strengthening the technological landscape of the 3D Printed Orthotics Market.

North America 3D Printed Orthotics Market Driver

Rising Demand for Customized Orthopedic Solutions

The growing prevalence of orthopedic disorders and lifestyle-related conditions is a major driver for the market. In North America, over 35 million individuals suffer from foot-related ailments annually, with 22% requiring orthotic intervention. Customized orthotics provide up to 40% better pressure distribution compared to conventional products, leading to higher adoption rates. Additionally, the aging population, which is expected to reach 65 million individuals above 65 years by 2030, is increasing demand. Production efficiency improvements have reduced manufacturing costs by 18%, making 3D printed orthotics more accessible. Insurance coverage expansion, covering nearly 48% of orthotic treatments, further supports market expansion in the 3D Printed Orthotics Market.

North America 3D Printed Orthotics Market Restraint

High Initial Investment and Equipment Costs

Despite strong growth, high capital investment remains a key restraint. Advanced 3D printers used for orthotics production can cost between USD 80,000 and USD 250,000 per unit, limiting adoption among small clinics. Additionally, material costs for high-performance polymers have increased by 12% over the past three years. Maintenance expenses account for nearly 8% of total operational costs annually. Skilled workforce shortages also pose challenges, with only 36% of clinics having trained personnel in additive manufacturing technologies. These factors hinder widespread adoption, impacting scalability in the 3D Printed Orthotics Market.

North America 3D Printed Orthotics Market Opportunity

Expansion of Telehealth and Remote Customization

Telehealth integration presents significant opportunities, with over 54% of patients in North America using remote consultation services in 2025. Remote scanning kits and mobile applications enable patients to capture foot data at home, reducing clinic visits by 28%. This approach is expected to increase market penetration by 15% in rural areas. Additionally, collaborations between technology providers and healthcare institutions have resulted in a 22% increase in remote orthotic prescriptions. This trend opens new revenue streams and expands accessibility, driving opportunities in the 3D Printed Orthotics Market.

Challenge in North America 3D Printed Orthotics Market

Regulatory and Standardization Barriers

Regulatory complexities and lack of standardization remain major challenges. Compliance with FDA regulations and Health Canada guidelines requires rigorous testing and certification processes, increasing product development timelines by 20%. Approximately 17% of new product launches face delays due to regulatory approvals. Additionally, the absence of standardized protocols for 3D printed medical devices creates inconsistencies in quality and performance. These challenges impact market entry for new players and slow innovation cycles, posing barriers to growth in the 3D Printed Orthotics Market.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.05 billion |

| Market Size in 2026 | USD 1.24 billion |

| Market Size in 2034 | USD 4.86 billion |

| CAGR | 18.6% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

North America 3D Printed Orthotics Market Segmentation

By Type

Rigid orthotics accounted for approximately 44% of total market share in 2025, with production exceeding 8.1 million units annually. These orthotics are primarily made from high-density polymers and carbon fiber composites, offering structural support and durability. They are widely used in cases of severe biomechanical issues, including flat feet and plantar fasciitis. Manufacturing precision reaches ±0.3 mm, ensuring optimal fit. Demand for rigid orthotics has increased by 19% annually due to rising sports injuries and chronic conditions.

Semi-rigid orthotics represent 33% of the market, with production volumes of around 6.1 million units in 2025. These devices combine flexibility and support, making them suitable for moderate conditions and athletic applications. Materials such as TPU and EVA are commonly used, providing shock absorption and durability. Adoption rates among athletes have increased by 21%, driven by improved comfort and performance benefits.

Soft orthotics hold a 23% share, with production reaching 4.3 million units annually. These are primarily used for diabetic patients and elderly individuals, offering cushioning and pressure relief. Silicone-based materials dominate this segment, accounting for 62% of production. Demand has grown by 17% due to increasing awareness of diabetic foot care and preventive healthcare measures.

By Application

Hospitals account for 42% of the market, producing over 7.8 million orthotic units annually. Integration with electronic health records (EHR) systems enables seamless patient data management. Adoption rates in hospitals have increased by 26% due to improved clinical outcomes and reduced treatment times.

Specialty clinics represent 35% of the market, with production volumes of 6.5 million units. These clinics focus on customized solutions, offering advanced scanning and design services. Patient satisfaction rates exceed 85%, driven by personalized treatment approaches.

Rehabilitation centers hold a 23% share, producing approximately 4.2 million units annually. These facilities focus on post-injury recovery and long-term care, with adoption rates increasing by 18% due to growing demand for rehabilitative services.

North America 3D Printed Orthotics Market Segmentations

Type

- Rigid Orthotics

- Semi-Rigid Orthotics

- Soft Orthotics

Application

- Hospitals

- Specialty Clinics

- Rehabilitation Centers

Country Insights

United States

The United States dominates with a 72% share, generating USD 0.82 billion in 2025. Production volumes exceed 13 million units annually, driven by advanced healthcare infrastructure and high adoption rates. Hospitals contribute 45%, clinics 37%, and rehabilitation centers 18%.

Canada

Canada accounts for 28% of the market, with production reaching 5.2 million units in 2025. The country has over 420 orthopedic facilities utilizing 3D printing technologies. Government support and healthcare funding have increased adoption rates by 19%.

Top Players in North America 3D Printed Orthotics Market

- Materialise NV

- Stratasys Ltd.

- 3D Systems Corporation

- HP Inc.

- EOS GmbH

- FitMyFoot Inc.

- Aetrex Worldwide Inc.

- SOLS Systems

- RSscan International

- Invent Medical Group

- Prodways Group

- EnvisionTEC Inc.

Top Two Companies

-

Stratasys Ltd.

-

Holds approximately 14.6% market share

-

Strong presence in healthcare-grade 3D printing systems

-

Extensive partnerships with hospitals and clinics

-

-

Materialise NV

-

Accounts for 12.3% market share

-

Leader in medical software and additive manufacturing solutions

-

Focus on innovation and customization technologies

-

Investment

Investment in the market has grown significantly, with total funding exceeding USD 620 million between 2023 and 2025. Approximately 48% of investments are directed toward technology development, while 32% focus on manufacturing expansion and 20% on distribution networks. The United States accounts for 76% of total investments, while Canada contributes 24%.

Mergers and acquisitions have increased by 27%, with major players acquiring startups specializing in AI-based design software. Collaborations between healthcare providers and technology firms have resulted in a 21% increase in joint ventures. These investments are driving innovation and expanding market reach.

New Product

New product development has accelerated, with over 140 new orthotic models launched in 2025 alone. Approximately 38% of these products incorporate advanced materials, improving durability by 25% and comfort by 30%. Smart orthotics with embedded sensors have increased by 19%, enhancing functionality.

Recent Development in North America 3D Printed Orthotics Market

- 2025: A leading company increased production capacity by 22%, reaching 2.5 million units annually, improving delivery times by 35%.

- 2024: Introduction of AI-based design software improved customization accuracy by 28% and reduced design time by 40%.

- 2023: Expansion of manufacturing facilities resulted in a 19% increase in production output across North America.

Research Methodology for North America 3D Printed Orthotics Market

The research process involved a combination of primary and secondary research methodologies. Primary research included interviews with industry experts, manufacturers, and healthcare professionals, accounting for 62% of data inputs. Secondary research involved analysis of company reports, government publications, and industry databases, contributing 38% of data. Market size estimation was conducted using both top-down and bottom-up approaches, ensuring accuracy and reliability. Data triangulation and validation were performed to ensure consistency across multiple sources.

Frequently Asked Questions

Senior Market Research Analyst | 8 Years Experience | Digital Therapeutics and Connected Medical Devices

Jenny specializes in digital therapeutics, remote monitoring devices and healthcare IT platforms. She has contributed to 101+ reports for medtech firms, healthcare providers and pharmaceutical companies. Her expertise includes clinical adoption forecasting, reimbursement analysis, regulatory pathways and competitive benchmarking across North America and Europe.