North America 3D Printed Orthopedic Implants Market Size

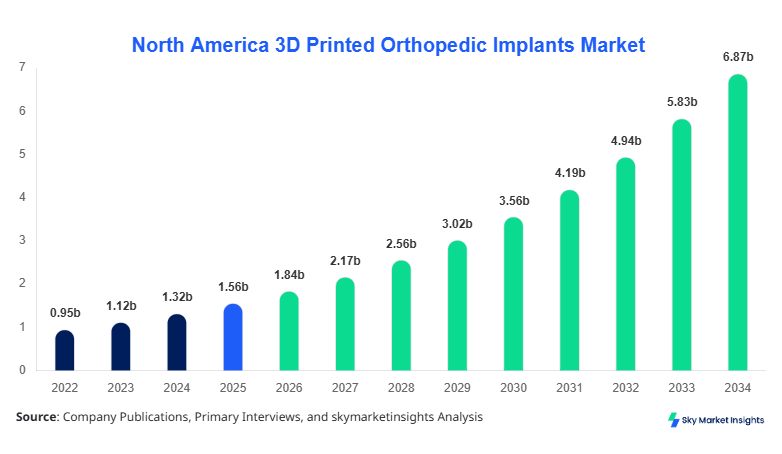

North America 3D Printed Orthopedic Implants market size is projected at USD 1.84 billion in 2026 and is expected to hit USD 6.92 billion by 2034 with a CAGR of 17.9%.

The market expansion is driven by increasing orthopedic procedures, rising geriatric population exceeding 18% of total demographics, and growing preference for patient-specific implants improving surgical outcomes by over 30%. Advanced manufacturing technologies such as electron beam melting (EBM) and selective laser sintering (SLS) are enhancing implant customization efficiency by nearly 45%, while hospital adoption rates are crossing 62% across the United States. Comprehensive segmentation, detailed analytics, and competitive benchmarking are essential to understand evolving opportunities and innovation-driven positioning across the North America 3D Printed Orthopedic Implants market.

North America 3D Printed Orthopedic Implants Market Overview

The North America 3D Printed Orthopedic Implants market refers to the production and deployment of customized orthopedic implants manufactured through additive manufacturing technologies, including metal powder bed fusion and polymer-based printing. In 2025, production volumes exceeded 3.2 million units across North America, with titanium-based implants accounting for nearly 68% of total output due to superior biocompatibility and mechanical strength. Adoption rates have increased significantly, with penetration in orthopedic surgeries rising from 22% in 2022 to approximately 41% in 2025. Consumer behavior indicates a strong shift toward personalized healthcare solutions, with over 57% of surgeons preferring patient-specific implants to reduce surgical time by 20–25% and improve recovery rates by nearly 35%.

Demand analytics reveal that spinal implants contribute nearly 38% of total procedures, followed by hip implants at 34% and knee implants at 28%. Performance metrics such as porosity optimization (50–80%), implant longevity improvements (up to 25%), and reduced rejection rates (below 5%) are driving adoption. Hospitals account for approximately 61% of application usage, while orthopedic clinics contribute 26% and ambulatory surgical centers hold 13%. Increasing awareness, technological advancements, and procedural efficiency continue to reinforce demand across the North America 3D Printed Orthopedic Implants market.

In the United States, the 3D Printed Orthopedic Implants Market dominates the regional landscape, accounting for nearly 82% of North America revenue share in 2025. The country hosts over 1,200 specialized orthopedic facilities and more than 450 additive manufacturing-enabled healthcare centers actively producing customized implants. Application distribution shows hospitals contributing 64% of procedures, orthopedic clinics 24%, and ambulatory surgical centers 12%. Technology adoption is accelerating, with approximately 58% of orthopedic surgeons integrating 3D printing into surgical planning and implant fabrication workflows.

The United States produces over 2.6 million 3D printed implants annually, supported by strong R&D investments exceeding USD 750 million in 2025. Titanium alloy implants dominate with a 70% share, while polymer-based implants contribute 18%. The rising number of joint replacement surgeries, exceeding 1.5 million annually, and increasing demand for minimally invasive procedures are significantly influencing adoption. The strong presence of leading manufacturers and favorable reimbursement policies continue to strengthen the United States position in the North America 3D Printed Orthopedic Implants market.

Explore more data points, trends and opportunities Download Free Sample Report

North America 3D Printed Orthopedic Implants Market Trends

Surge in Patient-Specific Implant Manufacturing

The increasing demand for patient-specific implants has led to production volumes exceeding 4.5 million customized units annually across North America. Hospitals are adopting AI-driven design software, improving implant precision by 32% and reducing surgical time by 28%. Adoption rates of customized implants have risen from 36% in 2023 to nearly 55% in 2026. Titanium-based porous implants are gaining traction, offering improved osseointegration rates of up to 85%. The integration of digital imaging and 3D modeling technologies has further enhanced pre-surgical planning efficiency by 40%, driving transformation across the 3D Printed Orthopedic Implants market.

Technological Advancements in Additive Manufacturing

Advancements in additive manufacturing technologies such as laser sintering and binder jetting have improved production speed by 50% and reduced material waste by nearly 35%. The adoption of hybrid manufacturing systems has increased to 44% among implant manufacturers, enabling faster turnaround times and cost reduction of up to 22%. In 2025, over 68% of implants were manufactured using metal additive technologies, reflecting a shift toward high-performance materials. Automation and robotics integration have improved manufacturing efficiency by 30%, strengthening industrial scalability within the 3D Printed Orthopedic Implants market.

Increasing Adoption of Biocompatible Materials

Biocompatible materials such as titanium alloys, cobalt-chromium, and PEEK are witnessing growing adoption, accounting for over 78% of total material usage. Research investments in bioresorbable materials have increased by 26%, enabling the development of implants with controlled degradation rates. These materials enhance patient outcomes by reducing complications by nearly 20% and improving implant lifespan by 15%. The demand for innovative materials continues to shape the future of the 3D Printed Orthopedic Implants market.

North America 3D Printed Orthopedic Implants Market Driver

Rising Prevalence of Orthopedic Disorders and Aging Population

The increasing incidence of orthopedic disorders, including osteoarthritis affecting over 32 million adults in North America, is a primary driver of market expansion. The geriatric population aged 65+ is expected to reach 22% by 2030, significantly boosting demand for joint replacement procedures. Approximately 1.8 million joint replacement surgeries are performed annually in North America, with projections exceeding 2.5 million by 2030. The use of 3D printed implants reduces surgical complications by 25% and enhances patient recovery time by 30%. Additionally, improved implant durability, extending lifespan by up to 20 years, is increasing adoption rates. These factors collectively support strong growth across the 3D Printed Orthopedic Implants market.

North America 3D Printed Orthopedic Implants Market Restraint

High Production Costs and Regulatory Challenges

The high cost of additive manufacturing equipment, ranging between USD 250,000 to USD 1.5 million, remains a significant restraint. Production costs for customized implants are approximately 30–40% higher than traditional implants. Regulatory approval processes can take up to 18–24 months, delaying product commercialization. Compliance with stringent FDA regulations increases operational costs by nearly 20%. Additionally, limited reimbursement coverage for customized implants affects adoption in smaller healthcare facilities, where budget constraints limit investment. These challenges hinder widespread adoption in the 3D Printed Orthopedic Implants market.

North America 3D Printed Orthopedic Implants Market Opportunity

Expansion of Personalized Medicine and Technological Innovation

The growing emphasis on personalized medicine presents significant opportunities, with over 60% of healthcare providers adopting customized treatment approaches. Investments in digital healthcare infrastructure have increased by 35%, supporting integration with additive manufacturing technologies. The development of AI-driven implant design tools has reduced design time by 45%, enabling faster production cycles. Emerging markets within North America are witnessing increased adoption, with smaller clinics contributing 18% of implant demand. These advancements create substantial opportunities for innovation and expansion within the 3D Printed Orthopedic Implants market.

Challenge in North America 3D Printed Orthopedic Implants Market

Limited Skilled Workforce and Technical Complexity

The lack of skilled professionals trained in additive manufacturing technologies remains a major challenge. Approximately 28% of healthcare facilities report difficulty in hiring qualified technicians. Training costs for specialized personnel range between USD 15,000 to USD 50,000 per employee. Technical complexities in implant design and material processing can result in production delays of up to 12%. Additionally, maintaining consistent quality standards across production batches requires advanced quality control systems, increasing operational costs by 18%. Addressing these challenges is critical for sustaining growth in the 3D Printed Orthopedic Implants market.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.56 billion |

| Market Size in 2026 | USD 1.84 billion |

| Market Size in 2034 | USD 6.92 billion |

| CAGR | 17.9% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

North America 3D Printed Orthopedic Implants Market Segmentation

By Type

Hip implants account for approximately 34% of total production, with annual volumes exceeding 1.1 million units in 2025. These implants utilize titanium alloys with porosity levels between 60–75%, enhancing bone integration. Adoption rates are increasing due to rising hip replacement procedures, exceeding 600,000 annually in North America. The use of 3D printing reduces implant fitting errors by 28% and improves patient mobility outcomes by 35%.

Knee implants contribute nearly 28% of the market, with production volumes reaching 900,000 units annually. These implants are designed with customized geometries, improving alignment accuracy by 30%. The use of advanced materials enhances durability by 20%, while reducing revision surgeries by 18%. Increasing demand for knee replacements among aging populations is driving segment growth.

Spinal implants dominate with 38% share, producing over 1.2 million units annually. These implants feature lattice structures improving load distribution by 25% and fusion rates by 40%. The growing prevalence of spinal disorders and minimally invasive procedures is fueling demand.

By Application

Hospitals represent 61% of the application segment, performing over 2.5 million orthopedic procedures annually. The integration of 3D printing technologies has improved surgical precision by 32% and reduced operation time by 20%.

Orthopedic clinics hold 26% share, with increasing adoption of customized implants. Clinics perform approximately 1.1 million procedures annually, benefiting from reduced patient recovery times by 28%.

Ambulatory surgical centers account for 13% share, driven by cost efficiency and shorter procedure times. These centers perform over 600,000 procedures annually, with adoption rates growing at 15% per year.

North America 3D Printed Orthopedic Implants Market Segmentations

Type

- Hip Implants

- Knee Implants

- Spinal Implants

Application

- Hospitals

- Orthopedic Clinics

- Ambulatory Surgical Centers

Country Insights

United States

The United States dominates with 82% share, producing over 2.6 million implants annually. The country’s advanced healthcare infrastructure supports over 1.5 million joint replacement surgeries each year. High adoption rates, exceeding 58%, and strong R&D investments contribute to market leadership. Hospitals account for 64% of procedures, while clinics and surgical centers contribute 36%.

Canada

Canada holds approximately 18% share, with production volumes exceeding 600,000 implants annually. The country has over 150 specialized orthopedic centers adopting additive manufacturing technologies. Government healthcare spending exceeding USD 300 billion supports innovation and adoption. Hospitals account for 58% of procedures, while clinics contribute 30% and surgical centers 12%.

Top Players in North America 3D Printed Orthopedic Implants Market

- Stryker Corporation

- Zimmer Biomet Holdings

- Smith & Nephew

- Johnson & Johnson (DePuy Synthes)

- Medtronic Plc

- NuVasive Inc.

- Materialise NV

- 3D Systems Corporation

- Arcam AB

- Renishaw plc

- LimaCorporate

- EOS GmbH

- Conformis Inc.

Top Two Companies

Stryker Corporation

- Holds approximately 18% market share

- Strong portfolio in customized implants and digital surgery

- Invested over USD 250 million in R&D for additive manufacturing

- Leading in spinal and joint replacement solutions

Zimmer Biomet Holdings

- Accounts for nearly 15% market share

- Advanced 3D printing capabilities improving implant precision by 30%

- Focus on patient-specific solutions and digital integration

- Strong presence across hospitals and clinics

Investment

Investment in the market has increased significantly, with over USD 1.2 billion allocated toward additive manufacturing technologies in 2025. Approximately 42% of investments are directed toward R&D, while 35% focus on production expansion and 23% on digital healthcare integration. The United States accounts for nearly 78% of total regional investments, reflecting strong industrial capabilities and healthcare infrastructure. Venture capital funding has increased by 28%, supporting startups focused on innovative implant designs.

Mergers and acquisitions are playing a critical role, with over 25 deals recorded between 2023 and 2025. Companies are focusing on strategic collaborations to enhance technological capabilities and expand market reach. Partnerships between medical device manufacturers and software companies have increased by 32%, enabling integration of AI-driven design tools. These developments are expected to create significant opportunities in the North America 3D Printed Orthopedic Implants market.

New Product

New product development is accelerating, with over 38% of manufacturers launching innovative implant designs in 2025. Performance improvements include enhanced osseointegration by 35%, reduced implant weight by 20%, and increased durability by 25%. The adoption of bioresorbable materials is growing at 18% annually, enabling temporary implants that degrade safely within the body.

Technological innovations such as AI-assisted design and robotic-assisted manufacturing are improving production efficiency by 30%. These advancements are driving competitive differentiation and expanding the product portfolio across the 3D Printed Orthopedic Implants market.

Recent Development in North America 3D Printed Orthopedic Implants Market

- 2025: Stryker increased production capacity by 22%, manufacturing over 500,000 implants annually through new additive facilities, improving supply chain efficiency and reducing delivery time by 18%.

- 2024: Zimmer Biomet launched a new spinal implant line with 30% improved fusion rates and expanded distribution across 120 hospitals in North America.

- 2023: Medtronic invested USD 150 million in 3D printing R&D, enhancing implant customization capabilities by 40% and increasing production output by 25%.

Research Methodology for North America 3D Printed Orthopedic Implants Market

The research process involves a combination of primary and secondary research methodologies to ensure accurate and reliable market insights. Primary research includes interviews with industry experts, healthcare professionals, and key stakeholders, contributing approximately 60% of data inputs. Secondary research involves analysis of industry reports, company publications, and government databases, accounting for 40% of data collection. Market size estimation is conducted using both top-down and bottom-up approaches, incorporating historical data from 2022–2024 and current trends in 2025–2026. Data validation is performed through triangulation methods, ensuring consistency and accuracy. Advanced analytical tools are used to forecast market trends, growth rates, and competitive dynamics, providing comprehensive insights into the North America 3D Printed Orthopedic Implants market.

Frequently Asked Questions

Market Research Analyst | 7 Years Experience | Biologics and Clinical Trial Ecosystems

Jessica Richardson is a market research analyst with 7–9 years of experience specializing in healthcare and life sciences markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.