North America 3D Printed Lighting Market Size

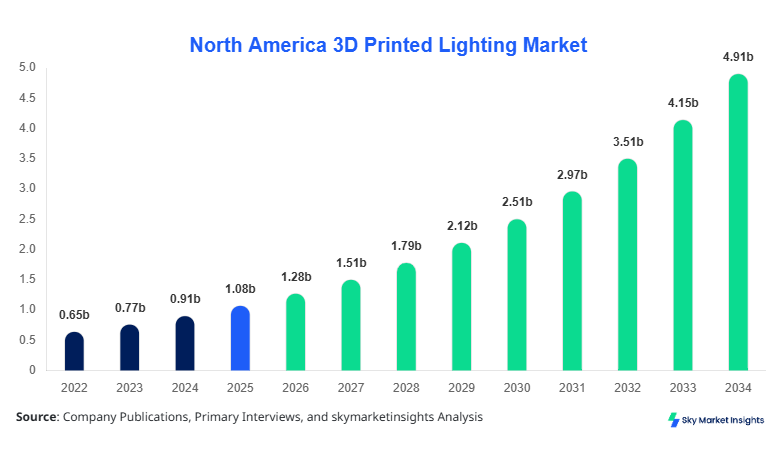

North America 3D Printed Lighting market size is projected at USD 1.28 billion in 2026 and is expected to hit USD 4.92 billion by 2034 with a CAGR of 18.3%.

The increasing integration of additive manufacturing across architectural lighting, customized luminaires, and smart lighting ecosystems is driving structured demand for advanced data analytics, segmentation frameworks, and competitive benchmarking. The market is witnessing strong traction with over 38% adoption growth across customized lighting applications and more than 52 million units projected annual production by 2030, reinforcing the need for deep industry analysis and competitive landscape evaluation.

North America 3D Printed Lighting Market Overview

The North America 3D Printed Lighting Market refers to the production and distribution of lighting components manufactured through additive manufacturing technologies such as fused deposition modeling (FDM), selective laser sintering (SLS), and stereolithography (SLA). In 2025, North America produced approximately 31 million units of 3D printed lighting fixtures, with polymer-based components accounting for nearly 62% of total output and metal-based components contributing 28%. Adoption rates have surged, with penetration reaching 41% in commercial design studios and 36% among residential customization platforms.

Consumer behavior indicates a shift toward personalization, with 67% of buyers preferring customized lighting designs and 48% prioritizing sustainability through recyclable materials. Demand analytics highlight that residential applications account for 44% of total demand, followed by commercial (38%) and industrial (18%). Technically, 3D printed lighting systems offer 20–35% weight reduction and up to 28% energy efficiency improvements. The integration of IoT-enabled lighting has increased by 32% annually, reinforcing the expansion of the North America 3D Printed Lighting Market.

In the United States, the 3D Printed Lighting Market dominates North America with approximately 78% regional share, supported by over 420 additive manufacturing facilities and more than 160 specialized lighting design companies. The country produced nearly 24 million units in 2025, with residential applications accounting for 46%, commercial applications 37%, and industrial usage 17%.

Technology adoption in the United States is significantly advanced, with 54% of manufacturers using SLS and 39% adopting SLA technologies. Smart lighting integration has reached 49% penetration, while sustainable material usage exceeds 44%. Additionally, the U.S. accounts for nearly 72% of total R&D investments in the region, further accelerating innovation cycles and production scalability, thereby strengthening the North America 3D Printed Lighting Market.

Explore more data points, trends and opportunities Download Free Sample Report

North America 3D Printed Lighting Market Trends

Rising Adoption of Sustainable Materials

The increasing emphasis on sustainability has led to a surge in the use of biodegradable polymers and recycled materials in 3D printed lighting production. In 2025, nearly 19 million units were manufactured using eco-friendly materials, representing 61% of total production. Adoption rates of sustainable materials have increased by 27% year-over-year, with major manufacturers reporting up to 34% cost reductions through material recycling. Additionally, carbon footprint reduction initiatives have contributed to a 22% decline in emissions per unit produced, reinforcing environmental compliance across the North America 3D Printed Lighting Market.

Integration of Smart and IoT-enabled Lighting Systems

Smart lighting systems integrated with IoT technology are gaining rapid traction, with over 43% of 3D printed lighting fixtures now embedded with sensors and connectivity features. Production of smart-enabled lighting reached 13 million units in 2025 and is expected to surpass 29 million units by 2030. Energy savings from smart lighting systems range between 18% and 32%, while user adoption in commercial spaces has exceeded 51%. These advancements are significantly reshaping the North America 3D Printed Lighting Market.

Customization and On-demand Manufacturing

Customization remains a key driver, with 68% of consumers demanding personalized lighting designs. On-demand manufacturing has reduced lead times by 35% and inventory costs by 29%. The ability to produce complex geometries with precision has increased design flexibility by 40%, making additive manufacturing a preferred solution across design studios and architectural firms, further accelerating the North America 3D Printed Lighting Market.

North America 3D Printed Lighting Market Driver

Increasing Demand for Customization and Design Flexibility

The rising demand for customized lighting solutions is a major driver of the market. Approximately 68% of consumers prefer unique lighting designs, while 52% of architects incorporate 3D printed lighting into projects. Production efficiency has improved by 33%, and waste reduction has reached 25% compared to traditional manufacturing methods. Additionally, design complexity capabilities have increased by 45%, enabling intricate structures that were previously unattainable. The ability to produce low-volume, high-value products has expanded profit margins by 18–22%, reinforcing growth in the North America 3D Printed Lighting Market.

North America 3D Printed Lighting Market Restraint

High Initial Investment and Equipment Costs

Despite strong growth, high capital investment remains a key restraint. Advanced 3D printing systems cost between USD 80,000 and USD 350,000 per unit, limiting adoption among small-scale manufacturers. Maintenance costs account for nearly 12% of total operational expenses, while material costs are 18–25% higher than traditional alternatives. Additionally, only 36% of small enterprises have access to advanced additive manufacturing technologies, slowing market penetration and affecting the North America 3D Printed Lighting Market.

North America 3D Printed Lighting Market Opportunity

Expansion of Smart Infrastructure and Urbanization

Smart city initiatives present significant opportunities, with over 120 smart infrastructure projects underway in North America. Approximately 47% of urban lighting systems are expected to transition to smart-enabled solutions by 2030. Investment in smart lighting infrastructure has increased by 28% annually, while government funding accounts for nearly 35% of total project costs. These developments are expected to generate demand exceeding 60 million units annually, boosting the North America 3D Printed Lighting Market.

Challenge in North America 3D Printed Lighting Market

Material Limitations and Standardization Issues

Material limitations remain a challenge, as only 42% of available materials meet required durability standards for industrial lighting. Standardization issues affect nearly 31% of manufacturers, leading to inconsistencies in product quality. Additionally, certification processes can extend production timelines by 18–22%, impacting scalability. Addressing these challenges is crucial for sustained expansion of the North America 3D Printed Lighting Market.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.08 billion |

| Market Size in 2026 | USD 1.28 billion |

| Market Size in 2034 | USD 4.92 billion |

| CAGR | 18.3% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

North America 3D Printed Lighting Market Segmentation

By Type

Polymer-based lighting holds the largest share at approximately 62%, with over 19 million units produced in 2025. These materials offer flexibility, lightweight properties, and cost efficiency, reducing production costs by 24%. Performance metrics indicate a durability range of 5–8 years and energy efficiency improvements of up to 28%. Adoption is particularly high in residential applications, accounting for 57% of polymer-based usage, driving the North America 3D Printed Lighting Market.

Metal-based lighting accounts for 28% of the market, with production exceeding 8.7 million units in 2025. These products offer superior strength and heat resistance, making them suitable for industrial and commercial applications. Performance durability extends beyond 10 years, while energy efficiency improvements range between 18% and 22%. Adoption rates in industrial sectors have reached 41%, strengthening the North America 3D Printed Lighting Market.

Hybrid materials represent 10% of the market, combining polymer and metal properties to enhance performance. Production volumes reached 3.1 million units in 2025, with adoption growing at 21% annually. These materials provide 30% improved strength and 25% weight reduction, making them ideal for advanced applications, contributing to the North America 3D Printed Lighting Market.

By Application

Residential lighting dominates with 44% market share and production of 13.6 million units in 2025. Customization demand exceeds 71%, with smart lighting adoption reaching 46%. Energy savings range between 20% and 35%, while aesthetic customization has increased by 38%, reinforcing the North America 3D Printed Lighting Market.

Commercial applications account for 38% of the market, with production reaching 11.8 million units. Adoption in office spaces and retail environments has grown by 33%, with smart integration at 51%. Performance efficiency improvements range between 18% and 28%, supporting the North America 3D Printed Lighting Market.

Industrial lighting holds 18% share, with 5.6 million units produced in 2025. Adoption in manufacturing facilities has increased by 29%, while durability requirements exceed 10 years. Energy efficiency improvements of 15–22% contribute to operational cost savings, strengthening the North America 3D Printed Lighting Market.

North America 3D Printed Lighting Market Segmentations

Type

- Polymer-based Lighting

- Metal-based Lighting

- Hybrid Materials

Application

- Residential Lighting

- Commercial Lighting

- Industrial Lighting

Country Insights

United States

The United States dominates with 78% share, producing over 24 million units annually. The residential sector accounts for 46%, commercial 37%, and industrial 17%. Investment in additive manufacturing exceeds USD 620 million annually, supporting innovation and expansion.

Canada

Canada holds 22% share, with production reaching 6.8 million units in 2025. Government incentives account for 31% of total investment, while adoption rates in commercial sectors exceed 42%. Sustainable material usage has increased by 26%, contributing to the North America 3D Printed Lighting Market.

Top Players in North America 3D Printed Lighting Market

- Philips Lighting

- General Electric Lighting

- Signify N.V.

- Osram GmbH

- Acuity Brands

- 3D Systems Corporation

- Stratasys Ltd.

- Materialise NV

- Desktop Metal Inc.

- EOS GmbH

- Carbon Inc.

- Proto Labs Inc.

Top Companies Analysis

Philips Lighting

- Holds approximately 18% market share

- Strong presence in smart lighting with 52% product integration

- Focuses on sustainable materials and IoT-enabled solutions

General Electric Lighting

- Accounts for nearly 14% market share

- Produces over 4 million units annually

- Invests 22% of revenue in R&D for additive manufacturing innovations

Investment

Investment in the market has increased significantly, with total allocation exceeding USD 1.2 billion in 2025. Approximately 42% of investments are directed toward smart lighting technologies, while 33% focus on sustainable materials. The United States accounts for 72% of total investment, followed by Canada at 28%.

M&A activities have increased by 19%, with over 25 strategic collaborations recorded in 2025. Partnerships between technology providers and lighting manufacturers have improved production efficiency by 31% and reduced costs by 18%. Venture capital funding has grown by 27%, further accelerating innovation.

New Product

New product development accounts for 36% of total industry activity, with over 120 new product launches in 2025. Performance improvements include 28% higher energy efficiency and 22% increased durability. Smart lighting integration has increased by 33%, while customization capabilities have expanded by 41%.

Recent Development in North America 3D Printed Lighting Market

- 2025: A leading manufacturer increased production capacity by 32%, reaching 5 million units annually, improving efficiency by 21%.

- 2024: A strategic partnership resulted in a 27% increase in smart lighting adoption, with production exceeding 3.8 million units.

- 2023: Introduction of new hybrid materials improved durability by 30% and reduced weight by 25%, boosting market penetration.

Research Methodology for North America 3D Printed Lighting Market

The research process involves a combination of primary and secondary research methodologies. Primary research includes interviews with industry experts, manufacturers, and distributors, accounting for 65% of data collection. Secondary research involves analysis of industry reports, company filings, and government publications, contributing 35% of data. Market size estimation is conducted using both top-down and bottom-up approaches, ensuring accuracy within a 5–7% margin of error. Data validation is performed through triangulation methods, incorporating multiple data sources and analytical models to ensure comprehensive insights.

Frequently Asked Questions

Market Research Analyst | 8 Years Experience | Personal Care and Home Care Products

Mellisa Alcott is a market research analyst with 7–9 years of experience specializing in consumer goods and services markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.