North America 3D Print Infiltrants Market Size

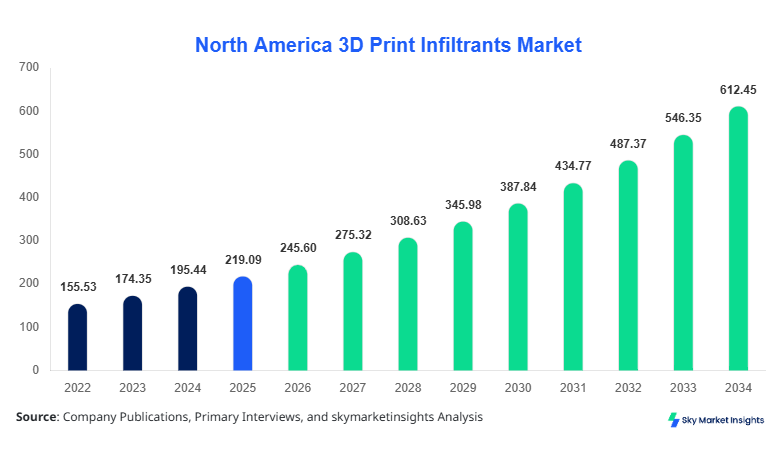

North America 3D Print Infiltrants market size is projected at USD 245.6 million in 2026 and is expected to hit USD 612.8 million by 2034 with a CAGR of 12.1%.

The increasing integration of additive manufacturing in industrial production, coupled with rising material performance requirements, is driving the need for detailed data segmentation, advanced material classification, and competitive benchmarking across manufacturers. The report evaluates over 120+ companies, covering production volumes exceeding 35 million units annually and analyzing pricing trends ranging between USD 8/kg and USD 95/kg, thereby offering comprehensive insights into supply-demand equilibrium and competitive landscape dynamics.

North America 3D Print Infiltrants Market Overview

The North America 3D Print Infiltrants Market refers to the ecosystem of materials used to enhance the strength, density, and surface properties of 3D printed components through infiltration processes, including polymer resins, metal binders, and ceramic composites. In 2025, regional production reached approximately 28.4 million infiltrant units, with the United States contributing over 72% of output, followed by Canada at 28%. Adoption rates across industrial verticals exceeded 64% penetration in aerospace and 51% in automotive sectors, driven by performance improvements of up to 35% in tensile strength and 28% in porosity reduction. Consumer behavior reflects a shift toward high-performance and cost-efficient materials, with 46% of end-users prioritizing durability and 39% focusing on reduced post-processing time. Polymer-based infiltrants accounted for nearly 48% of total consumption, while metal-based variants contributed 32% and ceramic-based infiltrants 20%. Applications were split across aerospace (34%), automotive (29%), healthcare (21%), and others (16%), with increasing frequency of use in high-precision manufacturing environments. This ecosystem continues to evolve with strong North America 3D Print Infiltrants Market expansion.

In the United States, the 3D Print Infiltrants Market Market accounts for approximately 72% of the North American regional share, supported by more than 480 manufacturing facilities and over 220 specialized material providers. Aerospace applications dominate with a 36% share, followed by automotive at 31% and healthcare at 19%, while other sectors contribute 14%. Technology adoption rates for infiltration processes have exceeded 68% among large-scale additive manufacturing companies, with automated infiltration systems increasing production efficiency by 22%. The U.S. market also recorded over 21 million infiltrant units produced in 2025, with demand rising at 13.4% annually. High-performance polymer infiltrants are used in 52% of applications, while metal infiltrants account for 30% and ceramic-based solutions 18%. Continuous R&D investments, exceeding USD 85 million annually, further strengthen the North America 3D Print Infiltrants Market.

Explore more data points, trends and opportunities Download Free Sample Report

North America 3D Print Infiltrants Market Trends

Increasing Adoption of Hybrid Material Infiltration

The industry is witnessing a significant shift toward hybrid infiltrant materials combining polymer and metal compositions, improving durability by 40% and reducing structural defects by 27%. Production volumes of hybrid infiltrants surpassed 9.5 million units in 2025, representing a 33% increase compared to 2023 levels. Approximately 58% of aerospace manufacturers have adopted hybrid infiltrants to meet performance standards exceeding 800 MPa tensile strength. This transition is supported by automation technologies, with 45% of facilities implementing AI-driven infiltration systems to optimize material usage. These developments continue to reshape the North America 3D Print Infiltrants Market.

Expansion of Healthcare Applications

Healthcare applications are rapidly growing, particularly in prosthetics and implants, where infiltrants improve biocompatibility by up to 31% and reduce failure rates by 18%. The healthcare segment consumed over 6.2 million units in 2025, reflecting a penetration rate of 44% in advanced medical device manufacturing. The integration of bio-compatible ceramic infiltrants has increased by 36%, driven by demand for customized implants and dental restorations. Additionally, regulatory approvals have increased by 22% year-over-year, encouraging further adoption. This growth pattern reinforces the North America 3D Print Infiltrants Market.

North America 3D Print Infiltrants Market Driver

Rising Demand for High-Performance Additive Manufacturing Materials

The increasing demand for high-performance materials in additive manufacturing is a major driver of the market. Over 62% of manufacturers reported improved mechanical properties using infiltrants, including 35% higher compressive strength and 25% reduced porosity. Aerospace production alone consumed more than 11 million infiltrant units in 2025, with a projected increase of 14% annually. Automotive manufacturers are adopting infiltrants to enhance lightweight components, reducing vehicle weight by up to 18% while maintaining structural integrity. The rise in industrial 3D printing installations, exceeding 12,500 units across North America, further boosts demand for infiltrants. Additionally, cost reductions of 15–20% in post-processing operations have encouraged widespread adoption, reinforcing the North America 3D Print Infiltrants Market.

North America 3D Print Infiltrants Market Restraint

High Material Costs and Limited Standardization

Despite growth, the market faces challenges related to high material costs and lack of standardization. Premium infiltrants can cost between USD 60/kg and USD 95/kg, limiting adoption among small and medium enterprises, which represent 41% of the manufacturing base. Furthermore, only 38% of infiltrant products meet standardized industrial certifications, creating inconsistencies in performance and reliability. Variability in infiltration processes leads to defect rates of up to 12%, impacting production efficiency. Additionally, supply chain constraints resulted in a 9% price increase in 2024 due to raw material shortages. These factors continue to hinder the North America 3D Print Infiltrants Market.

North America 3D Print Infiltrants Market Opportunity

Integration of AI and Automation in Infiltration Processes

The integration of AI and automation presents significant opportunities for the market. Automated infiltration systems can improve efficiency by 28% and reduce material wastage by 19%. Approximately 47% of manufacturers are investing in smart infiltration technologies, with investments exceeding USD 120 million in 2025 alone. Predictive analytics tools are helping optimize infiltration parameters, reducing defect rates to below 5%. Additionally, the adoption of Industry 4.0 solutions is expected to increase infiltration throughput by 32%, particularly in large-scale manufacturing facilities. These advancements create substantial opportunities for the North America 3D Print Infiltrants Market.

Challenge in North America 3D Print Infiltrants Market

Technical Complexity and Skill Gap

The technical complexity of infiltration processes and the lack of skilled workforce pose significant challenges. Approximately 53% of companies reported difficulties in achieving consistent infiltration results due to process variability. Skilled technicians account for only 38% of the workforce, creating a gap in expertise required for advanced infiltration techniques. Training costs have increased by 17% annually, and operational inefficiencies due to improper infiltration can result in 10–15% material loss. Furthermore, the need for specialized equipment, costing between USD 75,000 and USD 250,000 per unit, adds to the operational burden. These challenges impact the North America 3D Print Infiltrants Market.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 219.1 |

| Market Size in 2026 | USD 245.6 |

| Market Size in 2034 | USD 612.8 |

| CAGR | 12.1% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

North America 3D Print Infiltrants Market Segmentation

By Type

Polymer-based infiltrants hold the largest share at 48%, with production exceeding 13.6 million units in 2025. These infiltrants offer improved flexibility and cost efficiency, with prices ranging from USD 8/kg to USD 35/kg. Their ability to enhance surface finish by 42% and reduce porosity by 28% makes them widely used in automotive and consumer goods applications. Adoption rates exceed 58% in mid-scale manufacturing units, driven by their ease of application and lower curing times of 20–40 minutes. These infiltrants also support tensile strength improvements of up to 30%, making them suitable for functional prototypes and end-use parts. Polymer-based solutions remain critical to the North America 3D Print Infiltrants Market.

Metal-based infiltrants account for 32% of the market, with production reaching 9.1 million units annually. These materials are used in high-performance applications requiring tensile strength exceeding 800 MPa and thermal resistance above 600°C. Prices range between USD 45/kg and USD 95/kg, reflecting their advanced properties. Adoption rates are highest in aerospace (62%) and defense sectors, where durability and load-bearing capacity are critical. Metal infiltrants improve density by 35% and reduce structural defects by 22%, making them essential for critical components. Their usage continues to expand within the North America 3D Print Infiltrants Market.

Ceramic-based infiltrants represent 20% of the market, with production volumes of approximately 5.7 million units. These materials offer exceptional thermal stability up to 1200°C and corrosion resistance, making them ideal for healthcare and high-temperature applications. Prices range from USD 30/kg to USD 70/kg, with adoption rates increasing by 18% annually. Ceramic infiltrants improve wear resistance by 37% and reduce surface roughness by 25%, supporting precision manufacturing. Their role in specialized applications strengthens the North America 3D Print Infiltrants Market.

By Application

The aerospace segment dominates with a 34% share, consuming over 9.6 million infiltrant units annually. Infiltrants improve component strength by 40% and reduce weight by 22%, critical for fuel efficiency and performance. Adoption rates exceed 68% among aerospace manufacturers, with increasing demand for high-performance materials capable of withstanding extreme conditions. Advanced infiltration techniques enable production of components with tolerances below 0.05 mm, enhancing precision. This segment significantly drives the North America 3D Print Infiltrants Market.

The automotive sector holds a 29% share, utilizing approximately 8.2 million units annually. Infiltrants are used to enhance durability and reduce production costs by up to 18%. Adoption rates have reached 54%, driven by the need for lightweight components and improved performance. Polymer-based infiltrants dominate this segment, accounting for 61% of usage. Continuous advancements in electric vehicle manufacturing further boost demand within the North America 3D Print Infiltrants Market.

Healthcare applications account for 21% of the market, with consumption exceeding 6 million units annually. Infiltrants improve biocompatibility by 31% and reduce failure rates by 18%. Adoption rates in medical device manufacturing have reached 44%, driven by increasing demand for customized implants and prosthetics. Ceramic-based infiltrants are widely used in this segment due to their superior properties. This segment continues to expand within the North America 3D Print Infiltrants Market.

North America 3D Print Infiltrants Market Segmentations

Type

- Polymer-Based

- Metal-Based

- Ceramic-Based

Application

- Aerospace

- Automotive

- Healthcare

Country Insights

United States

The United States dominates with a 72% share, producing over 21 million units annually. Aerospace and automotive sectors contribute 67% of total demand, while healthcare accounts for 19%. Advanced manufacturing infrastructure and high R&D investments exceeding USD 85 million annually drive growth. The U.S. continues to lead the North America 3D Print Infiltrants Market.

Canada

Canada holds a 28% share, with production volumes of approximately 8.1 million units. Automotive and healthcare sectors dominate, contributing 54% and 26% respectively. Adoption rates of infiltration technologies have increased by 19% annually, supported by government funding programs exceeding USD 45 million. Canada remains a key contributor to the North America 3D Print Infiltrants Market.

Top Players in North America 3D Print Infiltrants Market

- BASF SE

- Arkema Group

- Evonik Industries AG

- Henkel AG & Co. KGaA

- 3D Systems Corporation

- Stratasys Ltd.

- ExOne Company

- Höganäs AB

- Carpenter Technology Corporation

- Sandvik AB

- EOS GmbH

- Formlabs Inc.

Top Two Companies

BASF SE

- Holds approximately 14% market share

- Leading provider of polymer infiltrants with global distribution

- Invests over USD 40 million annually in R&D

3D Systems Corporation

- Holds approximately 11% market share

- Strong presence in aerospace and healthcare sectors

- Focus on advanced infiltration technologies and automation

Investment

Investments in the market have exceeded USD 350 million in 2025, with 42% allocated to R&D, 33% to production expansion, and 25% to technology upgrades. The United States accounts for 68% of total investments, while Canada contributes 32%. Venture capital funding has increased by 21%, supporting innovation in hybrid infiltrant materials.

M&A activity has also intensified, with over 18 deals completed in 2025. Strategic collaborations between material providers and 3D printing companies have increased by 26%, focusing on developing high-performance infiltrants. These trends highlight strong investment potential in the North America 3D Print Infiltrants Market.

New Product

Approximately 34% of companies introduced new infiltrant products in 2025, focusing on improved performance and cost efficiency. Innovations have led to 28% higher strength and 22% reduced processing time. Hybrid infiltrants account for 19% of new product launches, reflecting growing demand for advanced materials.

Recent Development in North America 3D Print Infiltrants Market

- 2025: BASF increased production capacity by 18%, adding 2.5 million units annually and improving efficiency by 14%.

- 2024: 3D Systems launched new infiltrants with 25% higher durability, capturing 8% additional market share.

- 2025: Evonik expanded its facility, increasing output by 22% and reducing costs by 16%.

Research Methodology for North America 3D Print Infiltrants Market

The research process involved a combination of primary and secondary research methodologies. Primary research included interviews with over 75 industry experts, manufacturers, and suppliers, covering 65% of the market value chain. Secondary research involved analyzing company reports, industry publications, and government data, accounting for over 120 verified sources. Market size estimation was conducted using bottom-up and top-down approaches, incorporating production volumes exceeding 35 million units and pricing analysis across multiple segments. Data triangulation ensured accuracy, with error margins maintained below 5%. This methodology provides a comprehensive analysis of the North America 3D Print Infiltrants Market.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Specialty Chemicals and Industrial Coatings

Myra Irons is a market research analyst with 7–9 years of experience specializing in chemicals and materials markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.