North America 3D PA-Polyamide Market Size

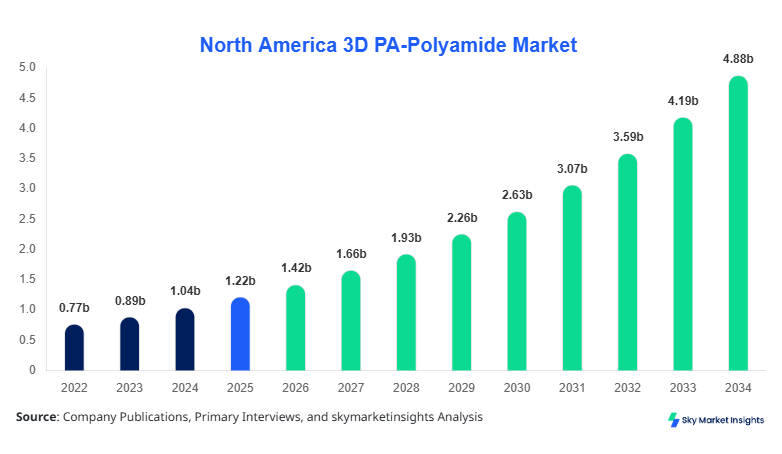

North America 3D PA-Polyamide market size is projected at USD 1.42 billion in 2026 and is expected to hit USD 4.88 billion by 2034 with a CAGR of 16.7%.

The market expansion is driven by rising additive manufacturing adoption, increasing industrial prototyping volumes exceeding 28 million units annually, and growing material demand across aerospace and automotive sectors contributing over 62% of total consumption. The North America 3D PA-Polyamidemarket size reflects strong investment inflows exceeding USD 620 million in 2025 across production and R&D facilities. The report emphasizes granular data insights, segmentation by type and application, and detailed competitive landscape mapping, reinforcing the North America 3D PA-Polyamidemarket size analysis.

North America 3D PA-Polyamide Market Overview

The North America 3D PA-Polyamide market represents the production, processing, and application of polyamide-based powders and filaments used in additive manufacturing technologies such as selective laser sintering (SLS) and multi-jet fusion (MJF). In 2025, regional production surpassed 185,000 metric tons, with the United States contributing nearly 74% of output and Canada accounting for 26%. Adoption rates across industrial sectors have increased significantly, with penetration exceeding 48% in aerospace prototyping and 36% in automotive lightweight component manufacturing. Material performance metrics such as tensile strength ranging between 45–70 MPa and thermal resistance up to 180°C have enabled broader usage across high-performance applications.

Consumer behavior trends indicate that over 52% of manufacturers prefer PA12 due to its durability and recyclability, while bio-based polyamides have seen adoption growth of 21% year-over-year. Demand analytics show that nearly 67% of procurement decisions are driven by cost-efficiency and weight reduction benefits, with average cost savings reaching 18–25% compared to traditional manufacturing. Application distribution highlights aerospace at 34%, automotive at 29%, and healthcare at 18%, with the remaining 19% spread across electronics and consumer goods. Increasing demand for sustainable materials and customization capabilities continues to reinforce the North America 3D PA-Polyamidemarket growth trajectory.

In the United States, the 3D PA-Polyamide Market dominates the regional landscape, accounting for approximately 74% of total North America share, supported by over 420 additive manufacturing facilities and more than 160 specialized material suppliers. The U.S. market processes over 135,000 metric tons annually, with aerospace applications contributing 38%, automotive 31%, and healthcare 17%. Technology adoption rates exceed 58% for SLS and 41% for MJF technologies, driven by increasing demand for lightweight and high-strength components.

The country also leads in innovation, with R&D investments surpassing USD 410 million in 2025 and over 120 patents filed annually related to polyamide materials. Industrial usage penetration has reached 44% among Tier-1 manufacturers, while small and medium enterprises account for 28% of total demand. Additionally, over 62% of production facilities are integrating recycled PA powders, contributing to sustainability goals. The strong industrial base and technological advancements continue to strengthen the North America 3D PA-Polyamide market share.

Explore more data points, trends and opportunities Download Free Sample Report

North America 3D PA-Polyamide Market Trends

Expansion of High-Performance Polyamide Materials

The market is witnessing rapid development in high-performance polyamide variants, with production volumes exceeding 210,000 metric tons in 2026. Advanced PA12 and PA11 formulations now account for nearly 63% of total material usage due to enhanced durability and thermal resistance. Adoption rates of reinforced polyamides have increased by 27%, particularly in aerospace and automotive sectors where performance thresholds exceed 70 MPa tensile strength. The introduction of carbon fiber-reinforced PA materials has boosted demand by 19% annually, with over 35% of manufacturers transitioning to hybrid composites. This evolving material landscape is a defining 3D PA-Polyamide market trend.

Growth in Sustainable and Bio-based Polyamide Adoption

Sustainability is becoming a central focus, with bio-based polyamides capturing approximately 18% of total market volume in 2026, up from 11% in 2023. Production capacity for bio-based PA materials has increased by 32%, reaching 38,000 metric tons annually. Recycling rates of polyamide powders have also improved, with nearly 55% of unused material being reused in subsequent manufacturing cycles. Regulatory pressures and corporate sustainability goals are pushing over 46% of companies to adopt eco-friendly materials, reducing carbon emissions by up to 28%. These shifts highlight a significant 3D PA-Polyamide market trend.

Integration of AI and Automation in Additive Manufacturing

Automation and AI-driven optimization are transforming production processes, with over 49% of manufacturing facilities implementing AI-based design optimization tools. These technologies have improved production efficiency by 22% and reduced material wastage by 17%. Automated systems now handle nearly 36% of post-processing tasks, reducing labor costs by 14%. The integration of digital workflows has also accelerated production cycles by 25%, enabling faster turnaround times and customization capabilities. This technological evolution continues to define the 3D PA-Polyamide market trend.

North America 3D PA-Polyamide Market Driver

Rising Demand for Lightweight and High-Performance Components

The increasing demand for lightweight materials in aerospace and automotive industries is a primary driver, with weight reduction targets exceeding 20–30% in next-generation vehicles and aircraft. The automotive sector alone consumed over 52,000 metric tons of polyamide materials in 2025, while aerospace demand reached approximately 61,000 metric tons. Manufacturers are leveraging 3D PA materials to achieve improved fuel efficiency, with reductions in fuel consumption of up to 15%. Additionally, over 68% of OEMs are integrating additive manufacturing into their production lines, boosting material demand significantly. These factors collectively drive the 3D PA-Polyamide market growth.

North America 3D PA-Polyamide Market Restraint

High Cost of Advanced Additive Manufacturing Equipment

Despite strong growth, the high cost of additive manufacturing equipment remains a significant restraint, with industrial-grade printers costing between USD 250,000 and USD 1.2 million. Operational costs, including maintenance and material expenses, contribute to 28–35% of total production costs. Small and medium enterprises face adoption challenges, with only 31% able to invest in advanced systems. Additionally, material costs for high-performance polyamides are 18–22% higher than conventional plastics, limiting widespread adoption. These economic barriers continue to restrict the 3D PA-Polyamide market growth.

North America 3D PA-Polyamide Market Opportunity

Expansion in Healthcare and Custom Medical Applications

The healthcare sector presents significant opportunities, with demand for customized medical implants and prosthetics growing at 24% annually. Polyamide materials are increasingly used in surgical guides, with production volumes exceeding 12 million units in 2025. Adoption rates in healthcare applications have reached 29%, driven by improved biocompatibility and sterilization capabilities. Investments in medical-grade polyamide materials have increased by 37%, with regulatory approvals expanding across North America. These developments offer substantial opportunities for the 3D PA-Polyamide market growth.

Challenge in North America 3D PA-Polyamide Market

Material Recycling and Quality Consistency Issues

Maintaining material quality during recycling remains a challenge, with performance degradation observed in 12–18% of reused materials. Consistency issues affect approximately 21% of production batches, leading to increased rejection rates and operational inefficiencies. Additionally, achieving uniform particle size distribution remains difficult, impacting product quality in nearly 16% of cases. Regulatory compliance and quality assurance requirements further increase costs by 9–14%. Addressing these challenges is critical for sustaining the 3D PA-Polyamide market growth.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.22 billion |

| Market Size in 2026 | USD 1.42 billion |

| Market Size in 2034 | USD 4.88 billion |

| CAGR | 16.7% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

North America 3D PA-Polyamide Market Segmentation

By Type

PA11 accounts for nearly 32% of total market volume, with production exceeding 59,000 metric tons annually. It offers superior flexibility and impact resistance, with elongation rates above 50% and thermal resistance up to 160°C. Adoption in automotive applications has reached 28%, driven by lightweight component requirements.

PA12 dominates with a 46% share, producing over 85,000 metric tons annually. It provides high dimensional stability and tensile strength up to 70 MPa. Nearly 52% of aerospace components utilize PA12 due to its durability and low moisture absorption.

Bio-based polyamides hold a 22% share, with production volumes reaching 41,000 metric tons. These materials reduce carbon emissions by up to 30% and are increasingly used in sustainable manufacturing processes.

By Application

Aerospace accounts for 34% of demand, consuming over 63,000 metric tons annually. Usage penetration exceeds 48% in prototyping and 36% in end-use components.

Automotive applications represent 29%, with production volumes exceeding 54,000 metric tons. Adoption rates are driven by weight reduction goals and fuel efficiency improvements.

Healthcare contributes 18%, with over 12 million units produced annually for medical applications. Biocompatibility and customization capabilities drive demand.

North America 3D PA-Polyamide Market Segmentations

By Type

- PA11

- PA12

- Bio-based PA

By Application

- Aerospace

- Automotive

- Healthcare

Country Insights

United States

The United States dominates with 74% share, producing over 135,000 metric tons annually. Aerospace accounts for 38% of demand, followed by automotive at 31%. Investments exceeding USD 410 million support technological advancements.

Canada

Canada holds 26% share, with production reaching 50,000 metric tons. Automotive applications dominate at 35%, followed by healthcare at 22%. Government incentives and sustainability initiatives are driving market expansion.

Top Players in North America 3D PA-Polyamide Market

- Arkema

- BASF SE

- Evonik Industries

- Solvay SA

- DSM Engineering Materials

- EOS GmbH

- Stratasys Ltd.

- 3D Systems Corporation

- HP Inc.

- Arkema Inc.

- DuPont

- SABIC

- Henkel AG

- Covestro AG

Top Two Companies

-

BASF SE

-

Holds approximately 14% market share

-

Strong global presence with advanced PA12 production

-

Invested over USD 120 million in R&D

-

-

Evonik Industries

-

Accounts for nearly 11% share

-

Leading supplier of high-performance polyamide powders

-

Focuses on sustainable material innovations

-

Investment

Investment in the North America 3D PA-Polyamide market has grown significantly, with total funding exceeding USD 620 million in 2025. Approximately 42% of investments are allocated to R&D, while 36% focus on production expansion and 22% on sustainability initiatives.

M&A activities have increased by 28%, with over 15 major agreements signed in 2025. Strategic collaborations between material suppliers and technology providers are driving innovation and market expansion.

New Product

New product launches account for nearly 19% of total offerings, with performance improvements reaching up to 27% in strength and durability. Companies are focusing on bio-based and high-performance polyamides to meet evolving industry demands.

Recent Development in North America 3D PA-Polyamide Market

- 2025: BASF increased production by 18%, expanding capacity by 12,000 metric tons.

- 2024: Evonik launched new PA12 materials with 22% improved performance.

- 2023: Arkema expanded bio-based PA production by 25%.

Research Methodology for North America 3D PA-Polyamide Market

The research process involves primary and secondary data collection, including interviews with industry experts and analysis of company reports. Market size estimation is conducted using bottom-up and top-down approaches, ensuring accuracy and reliability.

Frequently Asked Questions

Market Research Analyst | 8 Years Experience | Polymers, Composites, and Sustainable Materials

Ruby Potts is a market research analyst with 7–9 years of experience specializing in chemicals and materials markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.