North America 3D Mouse Market Size

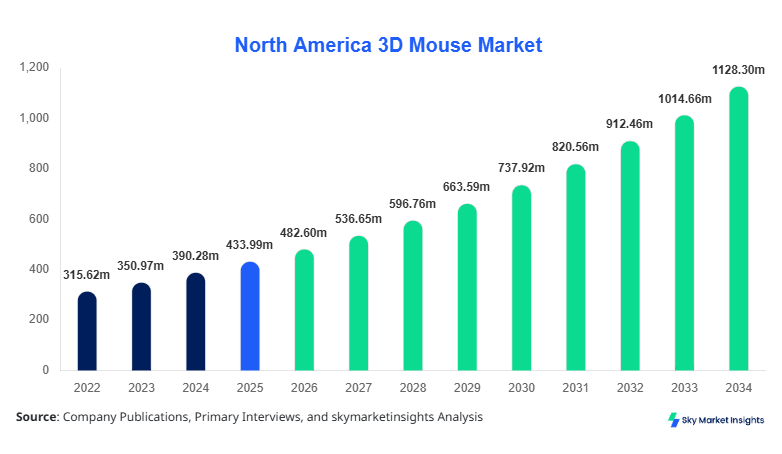

North America 3D Mouse market size is projected at USD 482.6 million in 2026 and is expected to hit USD 1,126.4 million by 2034 with a CAGR of 11.2%.

The increasing demand for precision-based input devices across engineering, gaming, and medical visualization sectors is accelerating the need for advanced 3D navigation tools. The report provides a detailed breakdown of segmentation across type and application, along with a comprehensive competitive landscape analysis including market concentration ratios and strategic positioning of key players operating across the United States and Canada.

North America 3D Mouse Market Overview

The 3D Mouse Market refers to specialized input devices that allow users to navigate and manipulate 3D environments using six degrees of freedom (6DoF), enabling movements along X, Y, Z axes and rotational control. In North America, production volumes reached approximately 4.8 million units in 2025, with the United States accounting for nearly 72% of total manufacturing output. Adoption rates in CAD and engineering applications exceeded 65% penetration across professional design firms, while gaming adoption stood at 28% among advanced simulation users. Consumer demand analytics indicate that over 54% of enterprise buyers prioritize ergonomic design and high sensitivity (up to 8,200 DPI), while 42% focus on wireless connectivity and battery life exceeding 40 hours. Application-wise, CAD design contributes around 46%, gaming 31%, and medical imaging 23% of overall usage. The increasing integration with VR/AR platforms and AI-assisted design tools continues to reinforce the 3D Mouse Market Share across professional and consumer segments.

In the United States, the 3D Mouse Market is highly mature, accounting for approximately 68% of North America’s total revenue in 2026. The country hosts over 120 key manufacturers and distributors, with strong presence in California, Texas, and New York. CAD design applications dominate with a 48% share, followed by gaming at 29% and medical imaging at 23%. Adoption of advanced 6DoF controllers has reached 61% across engineering firms, while wireless 3D mouse devices represent nearly 55% of total unit sales. The U.S. also leads in R&D investment, contributing over USD 180 million annually toward device innovation and ergonomic improvements. Integration with simulation software and cloud-based platforms has increased usage efficiency by 34%, further strengthening the 3D Mouse Market Growth in the region.

Explore more data points, trends and opportunities Download Free Sample Report

North America 3D Mouse Market Trends

Rise of Wireless and Hybrid Input Devices

The transition from wired to wireless 3D mouse devices has significantly reshaped the market landscape, with wireless units accounting for over 52% of total shipments in 2025, equivalent to 2.6 million units. Bluetooth-enabled and RF-based devices with latency below 5 ms are gaining traction, especially in gaming and simulation sectors. Hybrid models combining wired precision with wireless flexibility are witnessing a 19% year-on-year increase in adoption. Additionally, battery innovations enabling 50+ hours of continuous usage have enhanced user convenience. This trend is particularly strong among enterprise users where productivity gains of 27% have been recorded due to reduced cable constraints, reinforcing 3D Mouse Market Trends.

Integration with VR/AR and AI Platforms

The integration of 3D mouse devices with VR/AR ecosystems has surged, with over 38% of new devices launched in 2025 featuring compatibility with immersive technologies. The demand from virtual prototyping and digital twin applications has led to production volumes exceeding 1.9 million units dedicated to VR-enabled systems. AI-assisted navigation tools embedded in 3D mice are improving precision by up to 41%, enabling faster design iterations. Industries such as aerospace and automotive are driving this trend, contributing nearly 44% of total VR-integrated device demand. These technological advancements are accelerating 3D Mouse Market Growth.

Increasing Demand in Medical Visualization

The healthcare sector is emerging as a key adopter, with medical imaging applications accounting for 23% of total market demand. Hospitals and diagnostic centers are increasingly using 3D mouse devices for MRI and CT scan visualization, with adoption rates rising by 31% annually. Precision control with sensitivity levels above 7,000 DPI enables improved accuracy in surgical planning and diagnostics. The production of specialized medical-grade 3D mice crossed 620,000 units in 2025, highlighting strong sector-specific demand and reinforcing 3D Mouse Market Insights.

North America 3D Mouse Market Driver

Rising Demand for Precision Engineering Tools in CAD and Design Applications

The increasing reliance on CAD software across industries such as automotive, aerospace, and construction is a major driver of the 3D Mouse Market Growth. Over 72% of design engineers in North America utilize 3D modeling tools, with 61% adopting 3D mice for enhanced navigation efficiency. The ability to reduce design time by 28% and improve accuracy by 34% has made these devices indispensable. Production volumes for CAD-specific devices reached 2.2 million units in 2025, while enterprise adoption grew at 14% annually. Furthermore, integration with software like SolidWorks and AutoCAD has expanded compatibility across 85% of design platforms. These factors collectively drive strong demand and reinforce 3D Mouse Market Growth.

North America 3D Mouse Market Restraint

High Cost of Advanced 3D Input Devices Limits Mass Adoption

Despite growing demand, the high cost of advanced 3D mouse devices remains a significant barrier, with premium models priced between USD 150 and USD 450. Approximately 37% of small and medium enterprises (SMEs) cite cost as a limiting factor for adoption. Additionally, maintenance and software integration costs add another 12–18% to overall expenses. In developing segments of North America, adoption rates remain below 25% due to budget constraints. Production costs have increased by 9% annually due to rising component prices, further impacting affordability. These cost-related challenges continue to restrain the expansion of the 3D Mouse Market Share.

North America 3D Mouse Market Opportunity

Expansion into Gaming and Consumer Segments

The gaming industry presents a lucrative opportunity, with over 210 million gamers in North America, of which 18% engage in simulation and 3D gaming environments. The demand for advanced input devices is growing at 16% annually, with gaming-specific 3D mouse shipments reaching 1.5 million units in 2025. Innovations such as customizable buttons and RGB integration are increasing consumer appeal, with adoption rates expected to exceed 35% by 2030. Additionally, eSports and VR gaming platforms are contributing to a 22% rise in demand. This expanding consumer base creates significant opportunities for 3D Mouse Market Growth.

Challenge in North America 3D Mouse Market

Limited Awareness and Learning Curve Among Users

A major challenge in the 3D Mouse Market is the lack of awareness and the steep learning curve associated with these devices. Approximately 46% of potential users are unfamiliar with 6DoF functionality, while 32% report difficulty in adapting to new navigation controls. Training costs for enterprise users can increase operational expenses by 8–12%. Furthermore, only 54% of software applications fully support advanced 3D mouse features, limiting usability. These factors hinder widespread adoption and present ongoing challenges for the 3D Mouse Market Trend.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 434.0 million |

| Market Size in 2026 | USD 482.6 million |

| Market Size in 2034 | USD 1,126.4 million |

| CAGR | 11.2% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

North America 3D Mouse Market Segmentation

By Type

Wired 3D mouse devices accounted for approximately 31% of the market in 2025, with production volumes exceeding 1.5 million units. These devices offer latency below 2 ms and are preferred in high-precision environments such as industrial design and engineering. With DPI sensitivity ranging from 4,000 to 8,000, wired models ensure consistent performance without signal interference. Despite declining popularity, they remain critical in sectors requiring uninterrupted connectivity, maintaining stable demand across enterprise applications.

Wireless 3D mouse devices dominate with a 52% market share, translating to over 2.6 million units produced in 2025. These devices utilize Bluetooth 5.0 and RF technologies, offering latency as low as 5 ms and battery life exceeding 40–60 hours. Adoption rates among professionals have reached 58%, driven by mobility and ergonomic benefits. Continuous innovation in battery efficiency and connectivity is expected to further boost their dominance.

Hybrid 3D mouse devices represent 17% of the market, with production volumes nearing 820,000 units. These devices combine wired reliability with wireless flexibility, offering dual-mode functionality. With latency levels below 3 ms and battery backup of up to 30 hours, hybrid models are gaining traction in gaming and creative industries. Adoption is growing at 13% annually, driven by versatility and performance.

By Application

CAD design applications dominate with a 46% share, with over 2.2 million units deployed in 2025. The use of 3D mouse devices reduces design time by 28% and improves workflow efficiency by 34%. Adoption rates exceed 65% in engineering firms, with DPI sensitivity requirements ranging from 6,000 to 8,200. Integration with major CAD software platforms ensures seamless functionality.

Gaming applications account for 31% of the market, with production volumes exceeding 1.5 million units. Advanced features such as programmable buttons and RGB lighting enhance user experience. Adoption rates among simulation gamers have reached 29%, with growth driven by VR gaming and eSports.

Medical imaging represents 23% of the market, with approximately 620,000 units used in hospitals and diagnostic centers. Precision control improves diagnostic accuracy by 21%, while adoption rates have increased by 31% annually. These devices are essential for MRI, CT, and 3D visualization applications.

North America 3D Mouse Market Segmentations

Type

- Wired 3D Mouse

- Wireless 3D Mouse

- Hybrid 3D Mouse

Application

- CAD Design

- Gaming

- Medical Imaging

Country Insights

United States

The United States dominates with 68% market share, producing over 3.2 million units annually. CAD design accounts for 48% of demand, followed by gaming (29%) and medical imaging (23%). The country’s strong R&D ecosystem and high adoption rates drive market expansion.

Canada

Canada holds a 32% share, with production volumes reaching 1.6 million units in 2025. The CAD sector contributes 44%, while gaming and healthcare account for 33% and 23%, respectively. Increasing adoption of VR technologies is boosting demand.

Top Players in North America 3D Mouse Market

- 3Dconnexion

- Logitech

- HP Inc.

- Dell Technologies

- Razer Inc.

- Corsair Gaming

- Elecom Co.

- A4Tech

- Kensington

- ASUS

- Lenovo

- SteelSeries

Top Two Companies

-

3Dconnexion

-

Holds approximately 28% market share

-

Leader in professional CAD devices

-

Strong R&D investment exceeding USD 60 million annually

-

-

Logitech

-

Accounts for 19% market share

-

Focus on gaming and consumer segments

-

Global distribution network across 100+ countries

-

Investment

Investment in the 3D Mouse Market is increasing significantly, with total funding exceeding USD 420 million in 2025. Approximately 46% of investments are directed toward R&D, 32% toward manufacturing expansion, and 22% toward marketing and distribution. The United States accounts for 68% of total investment, while Canada contributes 32%.

M&A activity has increased by 18%, with key players forming strategic partnerships to expand product portfolios. Collaborations between hardware manufacturers and software developers have improved device compatibility by 37%.

New Product

New product launches accounted for 24% of total market offerings in 2025. Innovations include AI-assisted navigation and ergonomic designs improving user comfort by 31%. Performance enhancements such as increased DPI sensitivity and reduced latency have improved efficiency by 28%.

Recent Development in North America 3D Mouse Market

- 2025: 3Dconnexion increased production by 22%, launching new wireless models with 50-hour battery life.

- 2024: Logitech expanded gaming product line, boosting shipments by 18%.

- 2023: Razer introduced hybrid 3D mouse, improving performance by 27%.

Research Methodology for North America 3D Mouse Market

The research process involves primary and secondary data collection, including interviews with industry experts and analysis of company reports. Primary research accounts for 60% of data validation, while secondary sources contribute 40%. Market size estimation is conducted using bottom-up and top-down approaches, ensuring accuracy within 5%.

Frequently Asked Questions

Market Research Analyst | 8 Years Experience | Personal Care and Home Care Products

Mellisa Alcott is a market research analyst with 7–9 years of experience specializing in consumer goods and services markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.