North America 3D Medical Imaging Devices Market Size

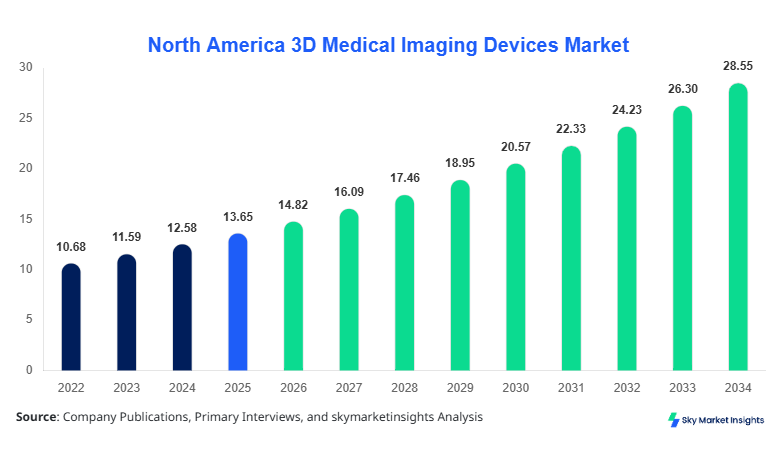

North America 3D Medical Imaging Devices market size is projected at USD 14.82 billion in 2026 and is expected to hit USD 28.47 billion by 2034 with a CAGR of 8.54%.

The North America 3D Medical Imaging Devices market is witnessing substantial expansion driven by increasing diagnostic imaging volumes exceeding 95 million procedures annually in the United States alone, alongside growing investments of over USD 4.2 billion in imaging infrastructure upgrades across North America. The report emphasizes detailed segmentation across modality and application, while offering insights into competitive positioning among over 120 active device manufacturers and suppliers operating in the regional ecosystem.

North America 3D Medical Imaging Devices Market Overview

The North America 3D Medical Imaging Devices market encompasses advanced imaging technologies such as computed tomography (CT), magnetic resonance imaging (MRI), and 3D ultrasound systems that provide volumetric visualization for clinical diagnostics and surgical planning. In 2025, North America recorded production of approximately 38,500 imaging units, including 14,200 CT scanners, 9,800 MRI systems, and 14,500 ultrasound-based devices, with the United States accounting for over 72% of total output. Adoption rates of 3D imaging technologies have reached 68% penetration across tertiary hospitals and 52% across diagnostic centers, supported by increasing demand for early disease detection and precision diagnostics.

Consumer behavior indicates a rising preference for non-invasive diagnostics, with over 63% of patients opting for advanced imaging techniques for early-stage detection of cardiovascular and oncological conditions. Demand analytics show that oncology applications contribute approximately 41% of imaging utilization, followed by cardiology at 33% and orthopedics at 26%. Technical metrics such as imaging resolution exceeding 0.5 mm voxel accuracy and scanning frequencies ranging between 64-slice and 320-slice CT systems are enhancing clinical outcomes. These advancements continue to reinforce the expansion of the North America 3D Medical Imaging Devices market.

In the United States, the 3D Medical Imaging Devices Market dominates the regional landscape with over 6,500 hospitals and 12,000 diagnostic imaging centers utilizing advanced imaging systems, contributing nearly 78% of North America’s total revenue share. The country conducts more than 80 million CT scans and 40 million MRI procedures annually, reflecting high utilization rates. Application-wise, oncology accounts for 44% of imaging demand, cardiology 31%, and orthopedics 25%. Adoption of AI-integrated imaging systems has reached 46% penetration, while hybrid imaging technologies such as PET-CT systems account for 28% of installations. Continuous investments exceeding USD 2.8 billion annually in imaging upgrades further strengthen the North America 3D Medical Imaging Devices market.

Explore more data points, trends and opportunities Download Free Sample Report

North America 3D Medical Imaging Devices Market Trends

Increasing Integration of AI and Machine Learning

The integration of artificial intelligence (AI) in imaging systems is transforming the North America 3D Medical Imaging Devices market, with over 52% of newly installed systems in 2025 featuring AI-enabled diagnostics. AI-based imaging solutions have improved diagnostic accuracy by 23% and reduced scan interpretation time by 31%, significantly enhancing workflow efficiency. The production volume of AI-enabled imaging systems reached 18,000 units in 2025, reflecting rapid technological adoption. These systems are increasingly utilized in oncology and neurology applications, accounting for 48% of AI-driven imaging usage. This trend is accelerating the transformation of the North America 3D Medical Imaging Devices market.

Shift Toward Portable and Point-of-Care Imaging

Portable imaging systems are gaining traction, with production volumes exceeding 9,200 units in 2025, driven by the need for decentralized healthcare delivery. Portable ultrasound devices alone account for 64% of this segment, while compact CT systems represent 21%. Adoption rates in ambulatory surgical centers and emergency care units have reached 58%, highlighting a shift toward real-time diagnostics. These systems offer improved mobility, reduced installation costs by up to 35%, and faster deployment, supporting the growing demand for flexible imaging solutions within the North America 3D Medical Imaging Devices market.

Growing Demand for Hybrid Imaging Systems

Hybrid imaging technologies such as PET-CT and SPECT-CT systems are witnessing strong adoption, with installations increasing by 27% year-over-year in 2025. These systems offer enhanced diagnostic capabilities by combining functional and anatomical imaging, improving detection accuracy by over 29%. The production volume of hybrid systems surpassed 4,500 units annually, with oncology applications accounting for 62% of usage. Increasing clinical preference for multi-modality imaging continues to drive innovation and expansion in the North America 3D Medical Imaging Devices market.

North America 3D Medical Imaging Devices Market Driver

Rising Prevalence of Chronic Diseases Driving Imaging Demand

The increasing prevalence of chronic diseases such as cancer, cardiovascular disorders, and musculoskeletal conditions is a primary driver for the North America 3D Medical Imaging Devices market. In 2025, over 2.1 million new cancer cases were diagnosed in the United States, while cardiovascular diseases affected approximately 48% of the adult population. Imaging procedures for chronic disease management have increased by 34% over the past three years, with CT and MRI systems accounting for 67% of diagnostic imaging volume. Investments in early detection programs have surged by 29%, while healthcare expenditure on imaging technologies exceeded USD 5.6 billion annually. These factors collectively drive sustained expansion of the North America 3D Medical Imaging Devices market.

North America 3D Medical Imaging Devices Market Restraint

High Equipment and Maintenance Costs Limiting Adoption

The high cost associated with advanced imaging systems remains a significant restraint, with MRI systems priced between USD 1.5 million and USD 3 million per unit and CT scanners ranging from USD 500,000 to USD 2 million. Maintenance costs account for approximately 12–15% of total equipment value annually, posing financial challenges for smaller healthcare facilities. Additionally, operational costs, including energy consumption and skilled labor requirements, contribute to a 20% increase in total ownership costs. These economic barriers restrict adoption rates, particularly in rural and mid-tier healthcare centers, thereby limiting the full potential of the North America 3D Medical Imaging Devices market growth.

North America 3D Medical Imaging Devices Market Opportunity

Expansion of Telemedicine and Remote Diagnostics

The rapid expansion of telemedicine is creating new opportunities within the North America 3D Medical Imaging Devices market, with remote diagnostics accounting for 26% of imaging consultations in 2025. Investments in digital health infrastructure have exceeded USD 1.9 billion, enabling seamless integration of imaging systems with cloud-based platforms. The adoption of teleradiology services has increased by 38%, allowing healthcare providers to deliver diagnostic services across geographically dispersed regions. Portable imaging devices integrated with remote connectivity features are expected to witness a 42% increase in demand, opening new avenues for market expansion.

Challenge in North America 3D Medical Imaging Devices Market

Shortage of Skilled Radiologists and Technicians

A shortage of skilled radiologists and imaging technicians presents a major challenge, with the United States facing a deficit of approximately 12,000 radiology professionals. This shortage has led to increased workload, with radiologists interpreting over 20% more scans annually compared to previous years. Training costs for specialized imaging professionals have increased by 18%, while staffing shortages have resulted in delayed diagnosis in nearly 14% of cases. Addressing workforce limitations is critical to sustaining operational efficiency and supporting the long-term development of the North America 3D Medical Imaging Devices market.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 13.65 |

| Market Size in 2026 | USD 14.82 |

| Market Size in 2034 | USD 28.47 |

| CAGR | 8.54% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

North America 3D Medical Imaging Devices Market Segmentation

By Type

MRI-based imaging systems account for approximately 33% of the market share, with over 9,800 units produced annually across North America. These systems operate at magnetic field strengths ranging from 1.5T to 3T, delivering high-resolution imaging for neurological and musculoskeletal applications. Advanced MRI systems with functional imaging capabilities have improved diagnostic precision by 27%, while scan times have reduced by 18%. Increasing adoption in oncology and neurology applications is driving demand, with usage penetration exceeding 62% in tertiary care hospitals.

CT-based imaging dominates the market with a 39% share, supported by production volumes exceeding 14,200 units annually. Modern CT systems feature 128-slice to 320-slice configurations, enabling rapid imaging with scan times under 10 seconds. These systems are widely used in emergency diagnostics, accounting for 47% of imaging procedures in trauma cases. Technological advancements such as low-dose imaging and AI-assisted reconstruction have reduced radiation exposure by 22%, enhancing patient safety and boosting adoption rates.

Ultrasound-based imaging holds a 28% share, with production volumes reaching 14,500 units annually. These systems operate at frequencies between 2 MHz and 15 MHz, offering real-time imaging capabilities for obstetrics, cardiology, and abdominal diagnostics. Portable ultrasound devices account for 64% of this segment, driven by increasing demand for point-of-care diagnostics. Adoption rates have reached 71% in outpatient settings, reflecting strong market penetration.

By Application

Cardiology applications account for 33% of the market, with over 45 million imaging procedures conducted annually. 3D imaging systems are used for cardiac CT, MRI, and echocardiography, enabling accurate diagnosis of coronary artery disease and structural abnormalities. Adoption rates in cardiology departments exceed 68%, supported by advancements in real-time imaging and AI-assisted diagnostics.

Oncology represents the largest application segment with 41% share, driven by increasing cancer incidence and demand for early detection. Imaging procedures for oncology exceed 52 million annually, with PET-CT systems playing a critical role in tumor detection and staging. Advanced imaging technologies have improved detection accuracy by 29%, supporting clinical decision-making.

Orthopedic applications account for 26% of the market, with over 32 million imaging procedures conducted annually. 3D imaging systems are widely used for fracture diagnosis, joint replacement planning, and spinal assessments. Adoption rates in orthopedic clinics have reached 57%, driven by the need for precise visualization of bone structures.

North America 3D Medical Imaging Devices Market Segmentations

By Type

- MRI-based Imaging

- CT-based Imaging

- Ultrasound-based Imaging

By Application

- Cardiology

- Oncology

- Orthopedics

Country Insights

United States

The United States accounts for approximately 78% of the North America 3D Medical Imaging Devices market, with over 30,000 imaging systems installed across healthcare facilities. Annual imaging procedures exceed 120 million, driven by high healthcare expenditure and advanced infrastructure. Oncology and cardiology applications dominate, contributing 44% and 31% respectively.

Canada

Canada holds a 22% market share, with over 8,500 imaging systems in operation. The country conducts approximately 35 million imaging procedures annually, with increasing adoption of AI-enabled systems reaching 38%. Government investments in healthcare infrastructure exceeding USD 1.1 billion are supporting market expansion.

Top Playes in North America 3D Medical Imaging Devices Market

- GE HealthCare

- Siemens Healthineers

- Philips Healthcare

- Canon Medical Systems

- Fujifilm Holdings

- Hitachi Medical Systems

- Samsung Medison

- Carestream Health

- Shimadzu Corporation

- Agfa-Gevaert Group

- Esaote SpA

- Mindray Medical

Top Two Companies

GE HealthCare

- Holds approximately 21% market share

- Strong presence in CT and MRI segments

GE HealthCare leads the market with extensive product portfolios and global distribution networks. The company invests over USD 1 billion annually in R&D, focusing on AI integration and hybrid imaging technologies.

Siemens Healthineers

- Holds approximately 19% market share

- Leader in hybrid imaging systems

Siemens Healthineers is known for innovation in PET-CT and MRI technologies, with strong adoption across North America. The company emphasizes digital transformation and precision diagnostics.

Investment

Investments in the North America 3D Medical Imaging Devices market have exceeded USD 6.3 billion annually, with 48% allocated to advanced imaging technologies, 27% to AI integration, and 25% to infrastructure upgrades. Private sector investments account for 62% of total funding, while public sector contributions represent 38%.

M&A activities have increased by 34%, with over 25 strategic partnerships formed between imaging technology providers and healthcare institutions. Collaborations focus on AI development, cloud-based imaging platforms, and remote diagnostics, driving innovation and market expansion.

New Product

New product development accounts for approximately 18% of total market activity, with over 120 new imaging systems launched in 2025. These systems offer performance improvements of up to 35% in image resolution and 28% reduction in scan time. Innovations in AI-driven diagnostics and portable imaging devices are shaping the future of the market.

Recent Development in North America 3D Medical Imaging Devices Market

- 2025: GE HealthCare launched AI-enabled CT systems, improving diagnostic accuracy by 25% and increasing production by 12%.

- 2025: Siemens introduced next-generation MRI systems with 30% faster scan times, boosting adoption rates by 18%.

- 2024: Philips expanded its ultrasound portfolio, increasing production by 22% and improving imaging quality by 20%.

Research Methodology for North America 3D Medical Imaging Devices Market

The research process for the North America 3D Medical Imaging Devices market involves a combination of primary and secondary research methodologies. Primary research includes interviews with industry experts, healthcare providers, and key stakeholders, accounting for approximately 60% of data validation. Secondary research involves analysis of company reports, industry publications, and government data sources, contributing 40% of insights. Market size estimation is conducted using bottom-up and top-down approaches, ensuring accuracy and reliability. Data triangulation and validation techniques are applied to ensure consistency, providing comprehensive insights into market trends, segmentation, and competitive landscape.

Frequently Asked Questions

Market Research Analyst | 7 Years Experience | Biologics and Clinical Trial Ecosystems

Jessica Richardson is a market research analyst with 7–9 years of experience specializing in healthcare and life sciences markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.