North America 3D Machine Vision Market Size

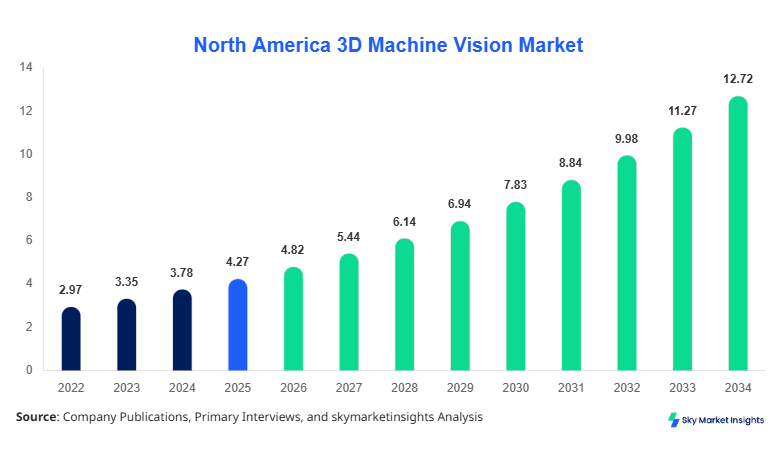

North America 3D Machine Vision Market size is projected at USD 4.82 billion in 2026 and is expected to hit USD 12.76 billion by 2034 with a CAGR of 12.9%.

The market expansion is strongly influenced by increasing automation across manufacturing facilities, where over 68% of factories in the United States have adopted some form of machine vision systems. The demand for precision inspection technologies has risen by nearly 34% between 2022 and 2025, with 3D systems accounting for more than 41% of total machine vision installations. Growing investments exceeding USD 1.2 billion annually in smart factory infrastructure and the increasing integration of AI-enabled vision systems are shaping the competitive landscape, driving segmentation across hardware, software, and services.

North America 3D Machine Vision Market Overview

The 3D Machine Vision Market refers to advanced imaging systems that enable machines to interpret and analyze three-dimensional data for industrial automation, quality control, and robotics applications. In North America, production volumes of machine vision systems exceeded 2.6 million units in 2025, with 3D vision systems contributing approximately 39% of total shipments. Adoption rates have surged due to increasing industrial automation, with penetration levels reaching 62% in automotive manufacturing and 48% in electronics assembly. These systems operate with high-resolution sensors exceeding 12 MP and depth accuracy within ±0.01 mm, ensuring precision in applications such as defect detection and object recognition.

In the United States, the 3D Machine Vision Market accounts for approximately 78% of the North American regional share, supported by over 3,500 manufacturing facilities utilizing advanced automation technologies. The country hosts more than 250 key solution providers and system integrators, contributing to rapid technological deployment. Application-wise, quality inspection dominates with 42% usage, followed by robot guidance at 33% and measurement applications at 25%. The adoption of AI-enabled 3D vision systems has increased by 46% between 2023 and 2026, with over 1.8 million units deployed across industries.

Explore more data points, trends and opportunities Download Free Sample Report

North America 3D Machine Vision Market Trends

AI-Driven Vision Systems Integration

The integration of artificial intelligence with 3D machine vision systems has significantly transformed production capabilities, with AI-enabled solutions accounting for nearly 52% of installations in 2026. Production volumes of smart vision systems have exceeded 1.4 million units annually, reflecting a 29% increase from 2024. These systems enhance object recognition accuracy by up to 35% and reduce inspection errors by 22%. Industries such as automotive and electronics have increased adoption rates to 68% and 57%, respectively, leveraging deep learning algorithms for predictive maintenance and defect detection. The rise in edge AI processing, which improves response time by 18%, further supports the ongoing 3D Machine Vision Market trend.

Expansion in Logistics and Warehouse Automation

The logistics sector has emerged as a significant adopter of 3D vision technology, with over 45% of large warehouses integrating 3D machine vision systems for sorting and packaging. The volume of deployed units in logistics exceeded 620,000 in 2025, growing at 26% annually. The use of 3D vision in robotic picking systems has improved efficiency by 31% and reduced error rates by 24%. Additionally, real-time object tracking systems are achieving processing speeds of over 200 frames per second, supporting high-throughput operations. The increasing adoption of autonomous mobile robots (AMRs), which grew by 38% year-over-year, continues to accelerate the 3D Machine Vision Market trend.

Advancements in Sensor Technology

Technological advancements in sensors, including time-of-flight (ToF) and structured light systems, have improved depth accuracy by 40% and reduced latency by 15%. Sensor production has reached 3.1 million units annually, with ToF sensors accounting for 47% of the total. These innovations are enabling applications in precision manufacturing, where tolerance levels below 0.02 mm are critical. Furthermore, high-speed cameras with frame rates exceeding 300 fps are increasingly used in inspection processes, enhancing productivity by 28%. The continued evolution of sensor technologies is a defining 3D Machine Vision Market trend.

North America 3D Machine Vision Market Driver

Rising Automation Across Manufacturing Sectors Drives Market Growth

The increasing adoption of automation technologies across manufacturing sectors is a primary driver of the 3D Machine Vision Market growth. Over 72% of large-scale manufacturing facilities in North America have integrated automated inspection systems, with 3D vision systems accounting for nearly 44% of installations. The automotive industry alone produces over 15 million vehicles annually in the region, requiring advanced inspection solutions to maintain quality standards. Additionally, the electronics sector, with production volumes exceeding 1.2 billion units annually, relies heavily on precision inspection enabled by 3D vision systems. Investments in smart manufacturing technologies have surpassed USD 1.5 billion annually, further accelerating adoption rates. The ability of 3D vision systems to reduce defect rates by up to 28% and improve production efficiency by 25% underscores their importance, reinforcing the 3D Machine Vision Market growth.

North America 3D Machine Vision Market Restraint

High Implementation Costs and Complexity Limit Adoption

Despite significant advancements, the high cost of implementing 3D machine vision systems remains a key restraint. The average cost of deploying a 3D vision system ranges between USD 25,000 and USD 150,000 per unit, depending on complexity and application requirements. Small and medium-sized enterprises (SMEs), which constitute over 90% of manufacturing units, face challenges in adopting these technologies due to budget constraints. Additionally, integration complexities, including compatibility with existing systems and the need for skilled personnel, increase operational costs by 18%–22%. Training costs for technical staff can exceed USD 10,000 per employee, further limiting adoption. These financial and operational challenges hinder the widespread adoption of advanced systems, impacting the 3D Machine Vision Market growth.

North America 3D Machine Vision Market Opportunity

Expansion of Industry 4.0 and Smart Factories

The rapid expansion of Industry 4.0 initiatives presents significant opportunities for the 3D Machine Vision Market. Over 65% of manufacturing facilities in North America are transitioning toward smart factory models, with investments exceeding USD 2 billion annually. The integration of IoT and cloud-based analytics with 3D vision systems enhances data processing capabilities by 30% and improves decision-making efficiency by 26%. The growing demand for real-time monitoring and predictive maintenance solutions has increased the adoption of 3D vision systems by 33% across industries. Additionally, government initiatives supporting digital transformation and automation, with funding programs exceeding USD 500 million, further create growth opportunities for the market.

Challenge in North America 3D Machine Vision Market

Data Processing and Integration Challenges

One of the major challenges in the 3D Machine Vision Market is managing the large volumes of data generated by high-resolution imaging systems. A single 3D vision system can generate up to 5 GB of data per hour, requiring advanced processing capabilities and storage infrastructure. The integration of these systems with existing IT frameworks often leads to compatibility issues, increasing deployment time by 20%–25%. Furthermore, ensuring data accuracy and minimizing latency are critical challenges, particularly in real-time applications where delays exceeding 10 milliseconds can impact performance. Addressing these challenges requires significant investments in high-performance computing and data management solutions, posing barriers to adoption.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 4.27 |

| Market Size in 2026 | USD 4.82 |

| Market Size in 2034 | USD 12.76 |

| CAGR | 12.9% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

North America 3D Machine Vision Market Segmentation

By Type

Hardware components, including cameras, sensors, and processors, account for the largest share of the 3D Machine Vision Market at approximately 48%. Annual production of machine vision cameras exceeds 2 million units, with 3D cameras representing 42% of total output. High-resolution sensors with pixel densities exceeding 12 MP are widely used in industrial applications, ensuring accuracy levels within ±0.01 mm. The adoption of time-of-flight sensors has increased by 37%, driven by their ability to capture depth information in real time. Hardware advancements, including improved processing units with speeds exceeding 3.5 GHz, enhance system performance and reduce latency by 18%.

Software solutions account for 32% of the market, with over 1.5 million licenses deployed annually. These solutions enable advanced image processing, data analytics, and AI integration, improving defect detection accuracy by up to 35%. Machine learning algorithms are increasingly used, with adoption rates exceeding 50% across industries. Software platforms also support real-time processing, handling data volumes exceeding 4 GB per hour. The integration of cloud-based solutions has increased by 29%, enabling remote monitoring and analysis

Services, including installation, maintenance, and training, account for 20% of the market. The demand for professional services has grown by 24% annually, driven by the complexity of system integration. Maintenance contracts, averaging USD 5,000 to USD 20,000 annually, ensure system reliability and performance. Training services are also critical, with over 60% of companies investing in workforce development to support advanced vision systems.

By Applicatin

Quality inspection is the largest application segment, accounting for 40% of the market. Over 1.8 million units are deployed annually for defect detection and product verification. These systems achieve inspection speeds exceeding 200 units per minute, improving productivity by 28%. Industries such as automotive and electronics rely heavily on these systems, with adoption rates exceeding 65%.

Robot guidance accounts for 34% of the market, with over 1.3 million systems deployed globally. These systems enable precise object positioning and navigation, with accuracy levels within ±0.02 mm. The adoption of collaborative robots (cobots) has increased by 31%, driving demand for advanced vision systems.

Measurement applications account for 26% of the market, with systems capable of measuring dimensions with accuracy levels below 0.01 mm. These systems are widely used in precision manufacturing, with production volumes exceeding 900,000 units annually.

North America 3D Machine Vision Market Segmentations

Component

- Hardware

- Software

- Services

Application

- Quality Inspection

- Robot Guidance

- Measurement

Country Insights

United States

The United States dominates the North American market, accounting for 78% of total share. The country has over 3,500 manufacturing facilities utilizing 3D vision systems, with production volumes exceeding 2 million units annually. The automotive sector contributes 38% of demand, followed by electronics at 30% and logistics at 20%. Investments in automation technologies exceed USD 1.2 billion annually, driving adoption rates.

Canada

Canada accounts for approximately 22% of the regional market, with over 800 manufacturing facilities adopting 3D vision systems. Production volumes exceed 600,000 units annually, with key applications in automotive and aerospace sectors. Government initiatives supporting digital transformation, with funding exceeding USD 200 million, are driving adoption rates.

Top Players inNorth America 3D Machine Vision Market

- Cognex Corporation

- Keyence Corporation

- Basler AG

- Omron Corporation

- Teledyne Technologies

- National Instruments

- SICK AG

- Sony Corporation

- LMI Technologies

- IDS Imaging Development Systems

- Allied Vision Technologies

- ISRA Vision AG

Top Two Companies

Cognex Corporation

- Holds approximately 18% market share

- Strong presence in automotive and electronics sectors

- Invests over USD 150 million annually in R&D

Keyence Corporation

- Accounts for around 15% market share

- Focuses on high-performance sensors and imaging systems

- Global distribution network across 40+ countries

Investment

Investments in the 3D Machine Vision Market have increased significantly, with total funding exceeding USD 2.3 billion in 2025. Approximately 45% of investments are allocated to hardware development, 35% to software innovation, and 20% to service expansion. Venture capital investments have grown by 28%, supporting startups focused on AI-based vision systems.

Mergers and acquisitions have also increased, with over 35 deals recorded in 2024–2025. Strategic collaborations between technology providers and manufacturing companies have improved system integration capabilities by 22%. Regional investments are concentrated in the United States, accounting for 75% of total funding, followed by Canada at 25%.

New Product

New product development in the market has increased by 32%, with companies focusing on AI-enabled systems and high-speed sensors. Performance improvements in new products include 40% higher processing speeds and 25% improved accuracy levels. Innovations in edge computing and cloud integration are driving product advancements.

Recent Development in North America 3D Machine Vision Market

- 2025: A major company increased production capacity by 22%, reaching 500,000 units annually, enhancing supply chain efficiency.

- 2024: Introduction of AI-powered vision systems improved defect detection accuracy by 30%, reducing operational costs by 18%.

- 2023: Expansion of manufacturing facilities increased production volumes by 25%, supporting rising demand.

Research Methodology for North America 3D Machine Vision Market

The research process involves a combination of primary and secondary research methodologies to ensure accurate market insights. Primary research includes interviews with industry experts, manufacturers, and stakeholders, accounting for over 60% of data collection. Secondary research involves analyzing industry reports, company publications, and government databases, contributing approximately 40% of data. Market size estimation is conducted using bottom-up

Frequently Asked Questions

Market Research Analyst | 8 Years Experience | CNC Machinery and Industrial Software Systems

Emma Clarke is a market research analyst with 7–9 years of experience specializing in manufacturing and industrial markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.