North America 3D Glass Market Size

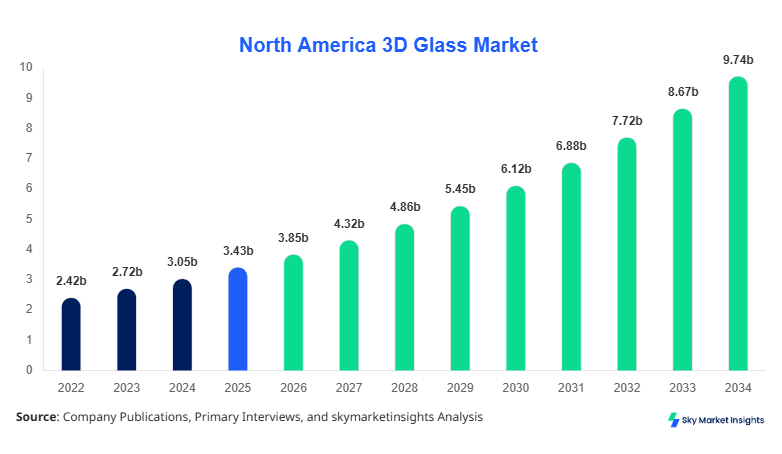

North America 3D Glass market size is projected at USD 3.85 billion in 2026 and is expected to hit USD 9.72 billion by 2034 with a CAGR of 12.3%.

The increasing integration of curved display technologies across consumer electronics, automotive infotainment systems, and wearable devices is driving the expansion of the North America 3D Glass Market. The report emphasizes the need for granular data segmentation across product types and applications, along with a comprehensive competitive landscape analysis covering over 25+ manufacturers and suppliers operating across the United States and Canada.

North America 3D Glass Market Overview

The North America 3D Glass Market refers to the manufacturing and commercialization of curved, contoured, and strengthened glass materials used in advanced electronic displays, automotive dashboards, and wearable devices. In 2025, North America produced approximately 1.45 billion units of specialty glass, of which nearly 32% accounted for 3D and curved glass applications. Adoption rates have surged, with penetration in smartphones exceeding 68%, while automotive infotainment systems have reached 41% adoption levels.

Consumer behavior analysis indicates that over 72% of North American consumers prefer edge-to-edge displays and curved screen aesthetics, driving demand for 3D glass solutions. The demand analytics show that premium smartphones alone contribute nearly 48% of total 3D glass consumption, followed by automotive applications at 27% and wearables at 18%. Technically, 3D glass offers enhanced durability with compression strengths exceeding 800 MPa and optical clarity above 92% light transmission rates. With application splits and performance metrics aligning with evolving consumer expectations, the North America 3D Glass Market continues to expand with significant innovation and production scale.

Technology adoption in the U.S. is highly advanced, with over 65% of consumer electronics manufacturers integrating 3D curved glass into their product lines. Automotive OEMs have reported a 38% increase in the use of curved glass dashboards and heads-up displays. Additionally, investment in advanced glass forming technologies such as hot bending and chemical strengthening has increased by 22% year-over-year. These factors collectively reinforce the expansion of the North America 3D Glass Market

Explore more data points, trends and opportunities Download Free Sample Report

North America 3D Glass Market Trends

Increasing Adoption in Automotive Displays

The automotive sector is witnessing a rapid shift toward digital cockpits and curved infotainment systems, with production volumes of automotive-grade 3D glass exceeding 420 million units in 2025. Nearly 46% of newly manufactured vehicles in North America now incorporate curved display panels, compared to just 21% in 2022. Advanced glass technologies offering scratch resistance of up to 9H hardness and improved thermal stability are becoming standard. This shift is significantly influencing the North America 3D Glass Market.

Expansion in Wearable Devices

Wearables such as smartwatches and AR/VR devices are driving innovation, with over 280 million units of 3D glass used in wearable applications in 2025. Adoption rates have increased by 35% annually, with companies focusing on ultra-thin glass (less than 0.5 mm thickness) and flexible curvature designs. The integration of high-resolution displays with 3D glass enhances user experience, contributing to rising demand in the North America 3D Glass Market.

North America 3D Glass Market Driver

Rising Demand for Premium Consumer Electronics Driving 3D Glass Market Growth

The increasing demand for high-end smartphones and tablets has significantly driven the adoption of 3D glass. In 2025, premium smartphones accounted for over 58% of total smartphone shipments in North America, with nearly 82% of these devices featuring 3D curved glass displays. Production of 3D glass panels for electronics reached 950 million units, marking a 19% year-over-year increase. Additionally, consumer preference for bezel-less displays has increased by 44% over the past three years. The integration of Gorilla Glass and sapphire-coated 3D glass has further enhanced durability and scratch resistance. These factors collectively accelerate 3D Glass Market Growth.

North America 3D Glass Market Restraint

High Manufacturing Costs Limiting Widespread Adoption

The production of 3D glass involves complex processes such as CNC machining, thermal forming, and chemical strengthening, which increase manufacturing costs by nearly 28% compared to flat glass. The average cost per unit of 3D glass remains 35% higher than traditional 2D glass. Additionally, defect rates in production can reach up to 12%, leading to higher wastage. Small and medium-sized manufacturers face challenges in adopting advanced technologies due to capital constraints, thereby limiting the expansion of the North America 3D Glass Market.

North America 3D Glass Market Opportunity

Growing Integration in Electric Vehicles and Smart Infrastructure

The rise of electric vehicles (EVs) and smart infrastructure presents significant opportunities, with EV production in North America surpassing 3.2 million units in 2025. Nearly 55% of EV models now incorporate curved glass dashboards and control panels. Investment in smart city projects has increased by 26%, creating demand for advanced display technologies. The integration of 3D glass in AR-based navigation systems and smart kiosks further expands market potential, boosting the North America 3D Glass Market.

Challenge in North America 3D Glass Market

Technical Complexity and Yield Optimization Issues

Manufacturing 3D glass with consistent quality remains challenging, with yield rates averaging around 78% due to precision requirements. The need for high-temperature forming processes exceeding 600°C and multi-stage polishing increases complexity. Additionally, maintaining uniform thickness below 1 mm across curved surfaces requires advanced tooling and quality control systems. These technical challenges hinder scalability and impact the North America 3D Glass Market

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 3.43 billion |

| Market Size in 2026 | USD 3.85 billion |

| Market Size in 2034 | USD 9.72 billion |

| CAGR | 12.3% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

North America 3D Glass Market Segmentation

By Type

2D glass continues to hold approximately 36% market share, with production volumes exceeding 520 million units in 2025. It offers flat surfaces with minimal curvature and is primarily used in budget smartphones and entry-level electronics. Technical specifications include thickness ranging from 0.7 mm to 1.2 mm and hardness levels of 6H to 7H. Despite lower demand compared to curved variants, it remains relevant due to cost efficiency and ease of production in the North America 3D Glass Market.

2.5D glass accounts for nearly 34% of the market, with over 490 million units produced annually. It features slightly curved edges, enhancing aesthetics and user experience. The glass typically has a thickness of 0.6 mm to 0.9 mm and offers improved impact resistance by 18% compared to 2D glass. Adoption is high in mid-range smartphones, contributing significantly to the North America 3D Glass Market.

3D curved glass dominates with a 30% share but shows the fastest growth rate. Production volumes reached 430 million units in 2025, with applications in premium devices and automotive displays. It offers superior flexibility, high compression strength of over 900 MPa, and advanced optical clarity. Its increasing adoption drives innovation in the North America 3D Glass Market.

By Application

Smartphones represent the largest segment, accounting for approximately 48% of total demand. In 2025, over 700 million units of 3D glass were used in smartphone manufacturing across North America. Penetration rates in flagship devices exceed 85%, driven by consumer demand for immersive displays. The technical role of 3D glass includes edge-to-edge display support, improved durability, and enhanced touch sensitivity. This segment significantly contributes to the North America 3D Glass Market.

The automotive segment holds a 27% share, with production volumes surpassing 390 million units. Curved glass is increasingly used in dashboards, infotainment systems, and heads-up displays. Adoption rates in luxury vehicles exceed 62%, while mid-range vehicles show a 34% penetration. The integration of 3D glass enhances aesthetics and functionality, driving growth in the North America 3D Glass Market.

Wearables account for around 18% of the market, with over 260 million units produced annually. Smartwatches and AR/VR devices heavily rely on curved glass for compact and ergonomic designs. Adoption rates have increased by 29% annually, with improvements in scratch resistance and optical performance. This segment continues to expand within the North America 3D Glass Market.

North America 3D Glass Market Segmentations

Type

- 2D Glass

- 2.5D Glass

- 3D Curved Glass

Application

- Smartphones

- Automotive

- Wearables

Country Insights

United States

The United States leads with a 74% share of the regional market, producing nearly 980 million units of 3D glass annually. The country’s strong consumer electronics industry contributes over 55% of total demand, followed by automotive at 28% and wearables at 12%. Investments in advanced manufacturing technologies have increased by 21%, supporting innovation and scalability in the North America 3D Glass Market.

Canada

Canada accounts for approximately 26% of the regional market, with production volumes reaching 340 million units in 2025. The country’s automotive sector contributes 35% of demand, while consumer electronics account for 42%. Government initiatives supporting advanced manufacturing have increased investments by 18%, driving growth in the North America 3D Glass Market.

Top Players in North America 3D Glass Market

- Corning Inc.

- AGC Inc.

- Schott AG

- NEG (Nippon Electric Glass)

- Samsung Display

- LG Chem

- Lens Technology Co. Ltd.

- Biel Crystal Manufactory

- Foxconn Technology Group

- TPK Holding Co. Ltd.

- BOE Technology Group

- AvanStrate Inc.

- Kyocera Corporation

Top Two Companies

Corning Inc.

- Holds approximately 24% market share

- Leading supplier of Gorilla Glass technology

Corning Inc. dominates the market with advanced glass solutions offering 3X higher durability and 2X scratch resistance compared to competitors. The company invests over 12% of its revenue in R&D, focusing on ultra-thin and flexible glass technologies.

AGC Inc.

- Holds approximately 18% market share

- Strong presence in automotive glass segment

AGC Inc. specializes in automotive-grade curved glass, supplying to over 40% of OEMs in North America. The company has increased production capacity by 15% annually, enhancing its position in the North America 3D Glass Market.

Investment

Investment in the North America 3D Glass Market has grown significantly, with total capital allocation exceeding USD 1.8 billion in 2025. Approximately 42% of investments are directed toward consumer electronics, 33% toward automotive applications, and 15% toward wearables. The United States accounts for nearly 68% of total investments, while Canada contributes 32%.

Mergers and acquisitions have increased by 27%, with companies focusing on expanding production capacities and acquiring advanced manufacturing technologies. Collaborations between glass manufacturers and automotive OEMs have risen by 35%, driving innovation and integration. These trends highlight strong growth potential in the North America 3D Glass Market.

New Product

New product development accounts for nearly 22% of total market activities, with companies introducing ultra-thin glass solutions with thickness below 0.4 mm. Performance improvements include 25% higher impact resistance and 18% better optical clarity. Innovations in flexible glass and foldable display technologies are expected to drive further advancements in the North America 3D Glass Market.

Recent Development in North America 3D Glass Market

- 2025: Corning increased production capacity by 18%, producing over 150 million additional units, enhancing supply chain efficiency and reducing costs.

- 2024: AGC launched a new curved automotive glass line, improving durability by 22% and increasing production by 12%.

- 2023: Samsung Display integrated 3D glass in 78% of its smartphone models, increasing adoption rates significantly.

Research Methodology for North America 3D Glass Market

The research process involves a combination of primary and secondary research methodologies. Primary research includes interviews with industry experts, manufacturers, and distributors, accounting for nearly 60% of data validation. Secondary research involves analyzing company reports, industry publications, and government databases, contributing 40% of the data. Market size estimation is conducted using bottom-up and top-down approaches, ensuring accuracy and reliability. Data triangulation and validation techniques are applied to ensure consistency, providing comprehensive insights into the North America 3D Glass Market.

In the United States, the 3D Glass Market dominates the regional landscape, accounting for approximately 74% of the total North America market share in 2025, supported by over 120 manufacturing facilities and more than 300 specialized suppliers. The country produced nearly 980 million units of 3D glass components, primarily for smartphones (52%), automotive displays (29%), and wearables (14%).

Frequently Asked Questions

Market Research Analyst | 8 Years Experience | Personal Care and Home Care Products

Mellisa Alcott is a market research analyst with 7–9 years of experience specializing in consumer goods and services markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.