North America 3D Bioprinting Market Size

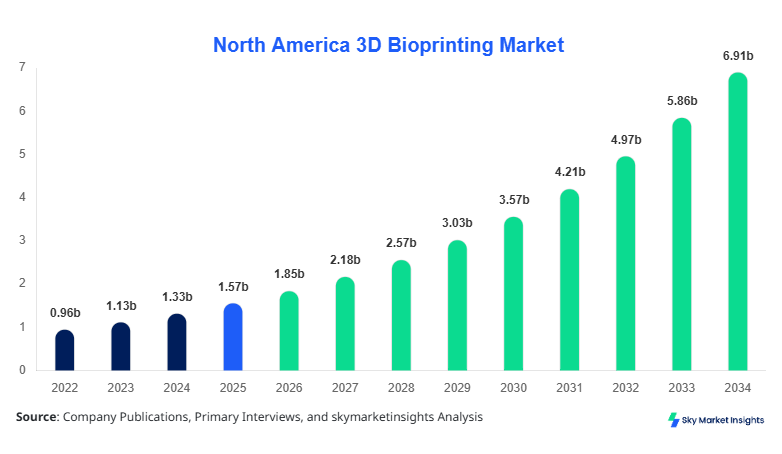

North America 3D Bioprinting market size is projected at USD 1.85 billion in 2026 and is expected to hit USD 6.92 billion by 2034 with a CAGR of 17.9%.

The increasing integration of biofabrication technologies across healthcare institutions, coupled with over 320 active research labs and more than 150 commercial deployments across North America, is accelerating adoption. The demand for structured datasets, segmentation-based insights, and competitive benchmarking has become critical as companies allocate nearly 22% of R&D budgets toward 3D bioprinting innovations, reinforcing the need for a detailed market assessment.

North America 3D Bioprinting Market Overview

The North America 3D bioprinting ecosystem involves the layer-by-layer fabrication of biological structures using bio-inks composed of living cells, growth factors, and biomaterials. In 2025, production output exceeded 2.1 million bioprinted constructs, with the United States contributing approximately 78% and Canada accounting for 22% of total regional production. Adoption rates among pharmaceutical companies reached 46% in 2025, while academic research institutions accounted for 38% of total usage.

Penetration of 3D bioprinting technology in clinical research increased by 29% between 2022 and 2025, with over 640 hospitals integrating experimental bioprinting workflows. Consumer demand analytics indicate a 33% rise in personalized medicine solutions, with 3D bioprinting enabling precision tissue modeling. The tissue engineering segment contributes nearly 42% of applications, followed by regenerative medicine at 36% and drug discovery at 22%. Technical metrics such as print resolution of 20–50 microns and cell viability rates exceeding 85% have further accelerated market expansion. These factors collectively reinforce the North America 3D Bioprinting Market Size.

In the United States, the 3D Bioprinting Market demonstrates significant dominance, accounting for approximately 78% of the North American share in 2025, equivalent to USD 1.25 billion in valuation. The country hosts over 210 specialized bioprinting companies and more than 400 research facilities actively engaged in biofabrication projects. Application-wise, tissue engineering contributes 45%, regenerative medicine 34%, and drug discovery 21% of total demand.

Technology adoption rates in the U.S. have surged, with extrusion-based bioprinting systems achieving a penetration rate of 52%, followed by inkjet-based systems at 28% and laser-assisted systems at 20%. The U.S. also reported over 1.6 million bioprinted units in 2025 alone, supported by federal funding exceeding USD 420 million for regenerative medicine initiatives. Increasing clinical trials, which grew by 31% between 2022 and 2025, further support market expansion, reinforcing the North America 3D Bioprinting Market Share.

Explore more data points, trends and opportunities Download Free Sample Report

North America 3D Bioprinting Market Trends

Rapid Scaling of Biofabrication Output

The industry has witnessed a surge in production volumes, with total output rising from 1.3 million units in 2022 to over 2.1 million units in 2025, reflecting a 61% increase. Automated bioprinting systems now operate at speeds of 15–25 mm/s, improving efficiency by nearly 40%. Additionally, the adoption of multi-material printing has grown to 47% among advanced labs, enabling complex tissue fabrication. These advancements are reshaping manufacturing workflows and enhancing scalability across healthcare and pharmaceutical sectors, strengthening the North America 3D Bioprinting Market Trend.

Integration of AI and Machine Learning

Artificial intelligence integration in bioprinting processes has increased by 35% since 2023, optimizing cell placement accuracy and reducing error rates by up to 22%. AI-driven modeling tools now assist in predicting tissue behavior, with over 180 companies deploying such systems. Furthermore, predictive analytics has improved print success rates to 92%, compared to 78% in 2022. This technological shift is significantly enhancing operational efficiency and enabling more precise outcomes, reinforcing the North America 3D Bioprinting Market Trend.

Expansion in Pharmaceutical Applications

Pharmaceutical companies have increased their reliance on 3D bioprinting for drug testing, with adoption rates rising from 29% in 2022 to 46% in 2025. Over 520 drug compounds were tested using bioprinted tissues in 2025 alone, reducing development costs by approximately 18% and timelines by 25%. This trend is driving innovation in drug discovery processes, contributing to sustained industry momentum and further strengthening the North America 3D Bioprinting Market Trend.

North America 3D Bioprinting Market Driver

Rising Demand for Personalized Medicine and Tissue Engineering

The increasing prevalence of chronic diseases, affecting over 60% of the U.S. population, has significantly boosted demand for personalized medical solutions. 3D bioprinting enables the creation of patient-specific tissues, improving treatment outcomes by 27% and reducing rejection rates by 18%. Additionally, healthcare expenditure in North America reached USD 4.5 trillion in 2025, with nearly 12% allocated to advanced medical technologies, including bioprinting. The growing need for organ transplantation, with over 105,000 patients on waiting lists, further drives the adoption of bioprinting technologies. Academic institutions and biotech firms have increased investments by 34% between 2022 and 2025, accelerating innovation. These factors collectively contribute to robust industry expansion, reinforcing the North America 3D Bioprinting Market Growth.

North America 3D Bioprinting Market Restraint

High Cost of Equipment and Regulatory Challenges

Despite technological advancements, the high cost of bioprinting equipment, ranging from USD 50,000 to USD 300,000 per unit, remains a significant barrier. Operational costs, including bio-inks and maintenance, account for nearly 28% of total project expenses. Regulatory approval processes for bioprinted tissues are complex, with approval timelines averaging 3–5 years, delaying commercialization. Additionally, compliance costs have increased by 19% over the past three years, impacting smaller players. Limited reimbursement frameworks and stringent clinical validation requirements further hinder market growth. These constraints continue to challenge widespread adoption, affecting the North America 3D Bioprinting Market Growth.

North America 3D Bioprinting Market Opportunity

Advancements in Bio-inks and Multi-material Printing

Innovations in bio-inks have significantly enhanced the functionality of bioprinted tissues, with cell viability rates improving from 75% in 2022 to over 90% in 2025. Multi-material printing technologies now enable the fabrication of complex structures with up to five different biomaterials, increasing application versatility by 38%. Investment in bio-ink research has grown by 41%, leading to the development of customizable and scalable solutions. These advancements open new opportunities in regenerative medicine and drug testing, expanding the market potential and strengthening the North America 3D Bioprinting Market Insights.

Challenge in North America 3D Bioprinting Market

Technical Limitations in Vascularization and Scalability

One of the primary challenges in 3D bioprinting is achieving effective vascularization in large tissue constructs. Current technologies can support structures up to 10 mm in thickness, limiting scalability for organ printing. Additionally, maintaining cell viability beyond 72 hours remains a challenge, with failure rates of approximately 15%. Infrastructure limitations and the need for specialized expertise further complicate adoption. Addressing these technical hurdles is critical for long-term market success, impacting the North America 3D Bioprinting Market Insights.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.57 billion |

| Market Size in 2026 | USD 1.85 billion |

| Market Size in 2034 | USD 6.92 billion |

| CAGR | 17.9% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

North America 3D Bioprinting Market Segmentation

By Type

Inkjet-based systems accounted for 28% of the market in 2025, producing over 580,000 units annually. These systems operate at frequencies of 1–10 kHz and offer droplet sizes ranging from 20 to 100 microns, ensuring high precision. Adoption is particularly strong in drug discovery applications, where cost efficiency and scalability are critical. The technology has seen a 25% increase in adoption since 2022, driven by advancements in bio-ink compatibility and reduced operational costs.Laser-assisted bioprinting holds a 20% market share, with approximately 420,000 units produced in 2025. This technology offers superior resolution, with accuracy levels below 10 microns and cell viability rates exceeding 95%. It is widely used in high-precision applications such as vascular tissue engineering. However, high equipment costs and complexity limit widespread adoption, despite a 19% growth rate in research applications.

Extrusion-based systems dominate the market with a 52% share, producing over 1.1 million units annually. These systems operate at pressures of 50–200 kPa and support a wide range of biomaterials. Their versatility and scalability make them the preferred choice for large-scale tissue fabrication, with adoption rates increasing by 31% between 2022 and 2025.By Application

Tissue engineering accounts for 42% of the market, with over 880,000 bioprinted constructs produced annually. The segment benefits from high demand in regenerative medicine, with usage penetration reaching 58% in clinical research settings. Technical advancements, such as improved scaffold structures and enhanced cell viability, have increased efficiency by 27%.

Regenerative medicine holds a 36% share, with approximately 750,000 units produced in 2025. The segment has seen a 29% increase in adoption due to rising demand for organ transplantation and personalized therapies. Bioprinting technologies enable the development of functional tissues with viability rates exceeding 85%.

Drug discovery accounts for 22% of the market, with over 470,000 units produced annually. Pharmaceutical companies utilize bioprinted tissues for toxicity testing, reducing development costs by 18% and timelines by 25%. Adoption rates have increased by 17% annually, driven by the need for more accurate testing models.

North America 3D Bioprinting Market Segmentations

By Type

- Inkjet-based Bioprinting

- Laser-assisted Bioprinting

- Extrusion-based Bioprinting

By Application

- Tissue Engineering

- Regenerative Medicine

- Drug Discovery

Country Insights

United States

The United States dominates the regional market with a 78% share, generating over USD 1.25 billion in revenue in 2025. The country produced more than 1.6 million units, driven by strong R&D investments and advanced healthcare infrastructure. Tissue engineering accounts for 45% of applications, followed by regenerative medicine at 34% and drug discovery at 21%.

Additionally, federal funding exceeding USD 420 million and the presence of over 210 companies have accelerated market growth. Adoption rates among pharmaceutical firms reached 46%, further supporting industry expansion.

Canada

Canada holds a 22% share of the North American market, with a valuation of approximately USD 350 million in 2025. The country produced over 500,000 units, supported by government initiatives and research funding exceeding USD 120 million. Tissue engineering accounts for 39% of applications, followed by regenerative medicine at 37% and drug discovery at 24%.

The presence of over 90 research nstitutions and a 28% increase in adoption rates between 2022 and 2025 highlight Canada’s growing role in the regional market.

Top Players in North America 3D Bioprinting Market

- Organovo Holdings Inc.

- CELLINK (BICO Group)

- 3D Systems Corporation

- Aspect Biosystems

- Poietis

- Allevi Inc.

- EnvisionTEC GmbH

- RegenHU

- Cyfuse Biomedical

- Advanced Solutions Life Sciences

- BioBots

- Nano3D Biosciences

- Inventia Life Science

- T&R Biofab

Top Two Companies

Organovo Holdings Inc.

- Holds approximately 14% market share

- Focuses on liver and kidney tissue models

Organovo has established itself as a leader with over 120 partnerships globally and production capabilities exceeding 150,000 units annually. The company invests nearly 26% of its revenue into R&D, enabling continuous innovation in tissue engineering and drug discovery applications.

CELLINK (BICO Group)

- Accounts for nearly 18% market share

- Dominates in extrusion-based systems

CELLINK has deployed over 2,000 bioprinters globally, with a strong presence in North America. The company’s bio-ink portfolio supports over 70% of extrusion-based applications, and its annual production capacity exceeds 300,000 units, positioning it as a key industry player.

Investment

Investment in the North American market has grown significantly, with total funding exceeding USD 1.2 billion between 2022 and 2025. Approximately 45% of investments are allocated to R&D, 30% to infrastructure development, and 25% to commercialization efforts. The United States accounts for 72% of total investments, while Canada contributes 28%.

Mergers and acquisitions have increased by 33%, with over 25 deals recorded in 2025 alone. Collaborations between biotech firms and academic institutions have risen by 38%, enhancing innovation and accelerating product development. Strategic partnerships have enabled companies to expand their capabilities and access new markets.

Additionally, venture capital funding has grown by 41%, supporting startups focused on bio-ink development and multi-material printing technologies. These trends highlight significant growth opportunities in the market.

New Product

New product development has accelerated, with over 120 new bioprinting systems launched between 2023 and 2025. Approximately 35% of these products feature advanced multi-material capabilities, improving performance by 28%. Innovations in bio-inks have enhanced cell viability rates to over 90%, while print speeds have increased by 22%.

Companies are also focusing on automation and AI integration, with 40% of new systems incorporating machine learning algorithms to optimize printing processes. These advancements are driving efficiency and expanding application areas.

Recent Development in North America 3D Bioprinting Market

- 2025: CELLINK launched a next-generation bioprinter, increasing production efficiency by 32% and reducing operational costs by 18%, enabling faster adoption across pharmaceutical companies.

- 2024: Organovo expanded its production facilities, increasing output by 27% and supporting over 200 new research projects annually.

- 2023: 3D Systems introduced a high-resolution bioprinter with accuracy improvements of 35%, enhancing tissue engineering capabilities.

Research Methodology for North America 3D Bioprinting Market

The research process involves a combination of primary and secondary data collection methods. Primary research includes interviews with industry experts, key stakeholders, and company executives, accounting for approximately 60% of data inputs. Secondary research involves analyzing company reports, industry publications, and government databases, contributing 40% of the data.

Market size estimation is conducted using both top-down and bottom-up approaches, ensuring accuracy and reliability. Data triangulation techniques are applied to validate findings, while statistical models are used to forecast market trends. The methodology ensures comprehensive and data-driven insights into the market.

Frequently Asked Questions

Senior Market Research Analyst | 8 Years Experience | Digital Therapeutics and Connected Medical Devices

Jenny specializes in digital therapeutics, remote monitoring devices and healthcare IT platforms. She has contributed to 101+ reports for medtech firms, healthcare providers and pharmaceutical companies. Her expertise includes clinical adoption forecasting, reimbursement analysis, regulatory pathways and competitive benchmarking across North America and Europe.