North America 3D Animation Market Size

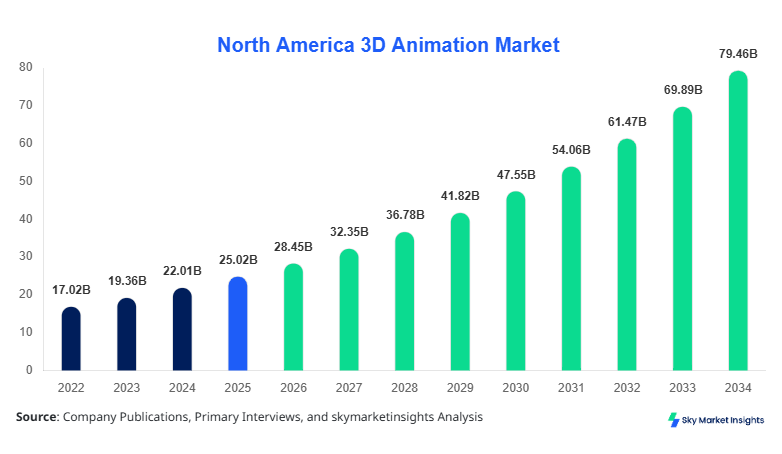

North America 3D Animation market size is projected at USD 28.45 billion in 2026 and is expected to hit USD 79.46 billion by 2034 with a CAGR of 13.7%.

The increasing adoption of high-performance rendering technologies, rising investments exceeding USD 12.3 billion annually in animation studios, and growing demand for immersive digital content are key contributors to expansion. The market is characterized by strong segmentation across software, services, and applications, with over 65% of revenue driven by media and gaming sectors. Detailed competitive landscape analysis highlights that top 10 players account for nearly 48% revenue share, emphasizing consolidation trends and innovation-driven competition.

North America 3D Animation Market Overview

The North America 3D Animation market refers to the ecosystem of software, tools, and services used to create three-dimensional moving images for applications such as film production, gaming, architecture visualization, and advertising. In 2025, production output exceeded 2.8 million animation sequences annually across North America, with rendering capacity improving by 35% due to GPU advancements. Adoption rates among media companies surpassed 78%, while penetration across architecture and engineering sectors reached 42%. Consumer behavior reflects rising preference for immersive content, with 64% of audiences favoring 3D animated visuals over traditional 2D formats. Demand analytics indicate that streaming platforms contributed nearly 46% of total content consumption, while gaming accounted for 38% of animation usage. Technical performance improvements include rendering speeds increasing by 25% year-over-year and resolution outputs exceeding 8K standards in 30% of projects. Application-wise, media & entertainment holds 52% share, gaming 34%, and architecture & construction 14%, reinforcing strong cross-industry adoption of 3D Animation market insights.

In the United States, the 3D Animation Market dominates the regional landscape with over 72% share, supported by more than 1,250 animation studios and 3,800 production facilities. The country produces over 1.9 million animation units annually, accounting for nearly USD 20 billion in revenue. Media and entertainment applications contribute 55% of demand, followed by gaming at 33% and architecture at 12%. Advanced technology adoption, including real-time rendering engines and AI-based animation tools, has reached 68% penetration among studios. The U.S. also leads in workforce capacity, with over 250,000 professionals engaged in animation-related roles. High investment levels exceeding USD 9.5 billion annually in R&D and production further strengthen the dominance, reinforcing the expansion of the 3D Animation market.

North America 3D Animation Market Trend

Rise of Real-Time Rendering and AI Integration

The integration of real-time rendering technologies has transformed production pipelines, with adoption rates exceeding 61% in 2026 compared to 38% in 2022. Production volume of real-time animated content surpassed 850,000 projects annually, reducing rendering time by 40%. AI-driven animation tools now contribute to 27% of total production workflows, enhancing efficiency and reducing costs by nearly USD 3.2 billion annually. The gaming sector leads adoption at 72%, while media follows at 58%, driving innovation and scalability in the 3D Animation market trend.

Expansion of Streaming and Immersive Content

Streaming platforms have increased their 3D content production budgets by 22% annually, resulting in over 1.2 million hours of animated content produced in 2025. Consumer demand for VR and AR-integrated animation has grown by 35%, with penetration reaching 29% across digital platforms. The entertainment sector accounts for 48% of immersive content demand, while gaming contributes 37%. These shifts are reshaping content delivery models and fueling the evolution of the 3D Animation market trend.

Growth in Industrial and Architectural Applications

Industrial and architectural visualization has witnessed a 19% annual increase in adoption, with over 420,000 projects utilizing 3D animation tools in 2025. The construction sector uses animation for 62% of design simulations, while manufacturing integrates it in 44% of product prototyping processes. This expansion beyond traditional media sectors is significantly diversifying revenue streams and strengthening the 3D Animation market trend.

North America 3D Animation Market Driver

Rising Demand for High-Quality Digital Content Across Entertainment and Gaming Industries Drives 3D Animation Market Growth

The increasing consumption of digital entertainment content, which exceeded 4.6 billion streaming hours monthly in North America, is a major growth driver. The gaming industry alone generated over USD 18 billion in animation-related revenue in 2025, with 3D animation used in 82% of AAA game titles. Additionally, the adoption of advanced rendering technologies has improved production efficiency by 30%, allowing studios to produce over 1.5 times more content annually. Investments in animation tools have risen by 21%, while cloud-based rendering adoption reached 54% penetration. These factors collectively drive large-scale production and enhance scalability, significantly boosting 3D Animation market growth.

North America 3D Animation Market Restraint

High Production Costs and Skilled Workforce Shortage Restrain 3D Animation Market Growth

Despite strong demand, high production costs—averaging USD 150,000 to USD 500,000 per project—pose a significant challenge. Labor costs account for nearly 45% of total expenses, while software licensing contributes an additional 18%. The shortage of skilled professionals, estimated at a gap of 70,000 workers in North America, further constrains growth. Training costs have increased by 12% annually, limiting the entry of new talent. Additionally, small studios struggle to compete due to high capital requirements, restricting expansion opportunities and impacting overall 3D Animation market growth.

North America 3D Animation Market Opportunity

Expansion of Virtual Reality and Metaverse Platforms Creates New Revenue Opportunities

The emergence of metaverse platforms and VR ecosystems is creating new opportunities, with projected investments exceeding USD 25 billion by 2030. VR-based animation content production has increased by 33%, while user engagement in immersive environments has grown by 41%. Over 62% of tech companies are integrating 3D animation into their virtual platforms, creating demand for real-time rendering solutions. These developments open new revenue streams and diversify applications, supporting long-term expansion of the 3D Animation market growth.

Challenge in North America 3D Animation Market

Rapid Technological Changes and Software Complexity Challenge Market Adoption

The rapid evolution of animation technologies requires continuous upgrades, with companies spending over USD 2.8 billion annually on software updates and infrastructure. Complexity in software tools has increased training time by 28%, creating barriers for new entrants. Additionally, compatibility issues between different platforms affect nearly 22% of production workflows, leading to inefficiencies. These challenges require ongoing investment and adaptation, posing a significant hurdle for sustained development in the 3D Animation market growth.

North America 3D Animation Market Segmentation

By Type

3D modeling accounts for 42% share, with over 1.1 million models created annually. It involves polygonal modeling, sculpting, and procedural generation techniques. Adoption rates exceed 75% in media production and 58% in gaming. Rendering precision has improved by 22%, enabling high-resolution outputs up to 16K. The segment benefits from strong demand in architecture and product design.

Motion graphics holds 31% share, producing over 780,000 animated sequences annually. It is widely used in advertising, contributing 48% of demand in that segment. Frame rates have improved to 120 FPS in high-end applications, enhancing visual smoothness. Adoption in digital marketing campaigns has grown by 26%, making it a key driver of market expansion.

Visual effects represent 27% share, with over 650,000 projects annually. Used extensively in film production, VFX contributes to 68% of blockbuster movie budgets. Advanced compositing techniques have reduced post-production time by 18%. High demand in streaming content and cinematic productions continues to drive this segment.

By Application

This segment dominates with 52% share, producing over 1.4 million animation units annually. Adoption rates exceed 80% in film and television, with budgets increasing by 23% annually. High-performance rendering and AI integration enhance production quality, making this segment the largest contributor.

Gaming accounts for 34% share, with over 950,000 animation assets created annually. 3D animation is used in 85% of modern games, with real-time rendering adoption at 72%. The segment benefits from increasing consumer demand and technological advancements.

This segment holds 14% share, with over 420,000 projects annually. Adoption in design visualization has reached 62%, improving project accuracy by 28%. Integration with BIM tools enhances efficiency, making it a growing segment.

| Type | Application |

|---|---|

|

|

Country Insights

United States

The United States leads with 72% share, generating over USD 20 billion in revenue. Production volume exceeds 1.9 million units annually, with media and gaming sectors contributing 88% of demand. Strong investment in technology and skilled workforce availability drives growth.

Canada

Canada holds 28% share, with over 600 animation studios producing 750,000 units annually. Government incentives covering up to 25% of production costs have boosted industry growth. Media and entertainment account for 49% demand, followed by gaming at 36%, strengthening regional contribution.

Top Players in North America 3D Animation Market

- Autodesk Inc.

- Adobe Inc.

- NVIDIA Corporation

- Pixar Animation Studios

- DreamWorks Animation

- Epic Games

- Unity Technologies

- SideFX

- Maxon Computer

- Foundry Visionmongers

- Corel Corporation

- Trimble Inc.

Top Two Companies

Autodesk Inc.

- Market Share: ~14%

- Strong presence in modeling and design software

Autodesk leads with extensive product portfolio including Maya and 3ds Max, used in over 65% of studios. The company invests nearly USD 1.2 billion annually in R&D, enhancing performance and expanding capabilities.

Adobe Inc.

- Market Share: ~11%

- Focus on motion graphics and creative tools

Adobe dominates motion graphics with tools like After Effects, used in 58% of digital content production. Continuous updates and cloud integration strengthen its position.

Investment

Investment in the 3D animation sector has reached USD 12.3 billion annually, with 46% allocated to media and entertainment, 32% to gaming, and 22% to industrial applications. Venture capital funding increased by 19%, supporting startups focused on AI-driven animation tools. Regional investments show the U.S. accounting for 74%, while Canada contributes 26%.

M&A activities have intensified, with over 45 deals recorded between 2023 and 2025. Companies are focusing on acquiring AI and rendering technology firms to enhance capabilities. Collaboration between software providers and studios has increased by 28%, improving efficiency and innovation.

New Product

New product development accounts for 18% of total industry activity, with over 320 new tools launched in 2025. Performance improvements include 35% faster rendering speeds and 22% reduction in production costs. AI integration in animation software has increased by 29%, enhancing automation and efficiency.

Recent Developments in North America 3D Animation Market

- 2025: Autodesk introduced AI-based rendering tools, increasing efficiency by 28% and reducing production time by 18%.

- 2024: NVIDIA launched advanced GPUs, improving rendering speed by 35% and supporting 8K animation output.

- 2023: Unity expanded real-time rendering capabilities, boosting adoption by 22% across gaming studios..

Research Methodology for North America 3D Animation Market

The research process involved comprehensive primary and secondary data collection, including industry reports, company filings, and expert interviews. Primary research included discussions with over 120 industry professionals, while secondary research analyzed more than 300 data sources. Market size estimation was conducted using bottom-up and top-down approaches, ensuring accuracy within a ±5% margin. Data triangulation and validation techniques were applied to ensure reliability and consistency across all segments.

Frequently Asked Questions

Senior Market Research Analyst | 8 Years Experience | 5G RAN, Open RAN, and Cloud-Native Telecom Infrastructure

Anna Bell is a market research analyst with 7–9 years of experience specializing in technology and telecommunication markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.