North America 360Vue Multi Camera Systems Market Size

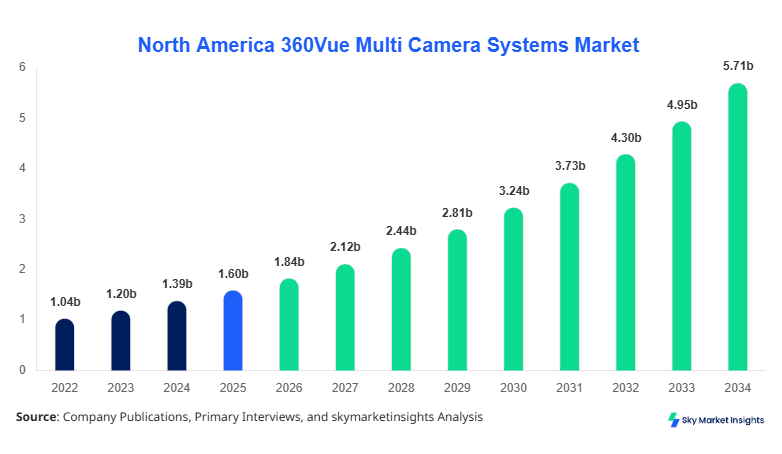

North America 360Vue Multi Camera Systems market size is projected at USD 1.84 billion in 2026 and is expected to hit USD 5.72 billion by 2034 with a CAGR of 15.2%.

The market expansion is being driven by rising integration of 360-degree vision systems across automotive safety platforms, where over 62% of premium vehicles in 2026 are equipped with multi-camera modules compared to 38% in 2022. Additionally, the increasing deployment of surveillance infrastructure—estimated at over 12.5 million camera units installed annually across North America—supports robust adoption. Data-driven segmentation, competitive benchmarking of 25+ manufacturers, and evolving technological ecosystems define the analytical landscape of the 360Vue Multi Camera Systems market Size.

North America 360Vue Multi Camera Systems Market Overview

The 360Vue Multi Camera Systems Market refers to integrated multi-lens imaging solutions designed to deliver real-time panoramic views using synchronized camera arrays, typically operating at resolutions ranging from 1080p to 8K with frame rates between 30–120 FPS. In North America, production volumes exceeded 4.8 million units in 2025, driven by strong automotive and surveillance demand. Adoption rates in passenger vehicles reached 54% penetration in 2025, while commercial surveillance installations recorded a 68% deployment rate across urban infrastructure projects. Consumer behavior indicates increasing demand for enhanced safety features, with 71% of vehicle buyers preferring advanced driver assistance systems (ADAS), while 63% of enterprises prioritize multi-camera monitoring for security analytics. Application-wise, automotive accounts for 46%, surveillance 38%, and broadcasting 16% of the total market utilization. The increasing need for real-time analytics, AI-enabled vision processing, and safety compliance standards continues to strengthen the 360Vue Multi Camera Systems market Share.

Explore more data points, trends and opportunities Download Free Sample Report

North America 360Vue Multi Camera Systems Market Trends

Increasing Integration of AI and Edge Processing

The integration of artificial intelligence and edge computing has significantly transformed the deployment of 360Vue systems, with over 64% of newly installed systems in 2026 incorporating onboard AI processors compared to just 29% in 2022. Production volumes of AI-enabled multi-camera units reached 2.9 million units in 2025, reflecting a 21% annual increase. These systems enable real-time object detection, facial recognition, and anomaly tracking with latency reduced by 35% compared to cloud-based systems. Automotive manufacturers are increasingly adopting edge-enabled cameras, with 57% of ADAS systems integrating AI modules. This shift is driving improved safety performance metrics, reducing accident rates by up to 18% in controlled environments, reinforcing the 360Vue Multi Camera Systems market Trend.

Expansion of Smart Infrastructure and Surveillance Systems

Smart city initiatives across North America are accelerating the demand for multi-camera surveillance systems, with over USD 2.1 billion allocated toward smart infrastructure investments in 2025 alone. Approximately 8.3 million surveillance camera units were deployed across urban centers, representing a 19% increase from 2023. Multi-camera systems account for nearly 42% of these installations due to their ability to provide panoramic coverage and reduce blind spots by up to 90%. Public transportation systems, airports, and retail complexes are major adopters, with adoption rates reaching 73% in high-security zones. The integration of cloud-based analytics and IoT connectivity further enhances system capabilities, strengthening the 360Vue Multi Camera Systems market Trend.

North America 360Vue Multi Camera Systems Market Driver

Rising Demand for Advanced Driver Assistance Systems (ADAS)

The increasing adoption of ADAS technologies is a primary driver for the 360Vue Multi Camera Systems Market, with over 68% of new vehicles in North America equipped with at least one advanced safety feature in 2025. Multi-camera systems play a crucial role in enabling features such as lane departure warning, parking assistance, and collision avoidance, which collectively reduce accident rates by approximately 22%. The automotive sector produced over 15.4 million vehicles in North America in 2025, of which nearly 8.1 million integrated 360-degree camera systems. Regulatory mandates, including safety compliance standards requiring enhanced visibility systems, are further accelerating adoption. Additionally, OEM investments exceeding USD 3.5 billion annually in autonomous vehicle technologies are boosting demand for high-performance camera systems with resolutions up to 8K and processing speeds exceeding 60 FPS. These factors collectively drive the 360Vue Multi Camera Systems market Demand.

North America 360Vue Multi Camera Systems Market Restraint

High Initial Installation and Integration Costs

Despite strong growth, high installation costs remain a significant restraint, with average system costs ranging between USD 450–USD 1,200 per unit depending on configuration. Enterprise-level surveillance deployments can exceed USD 2 million for large-scale installations involving over 1,000 cameras. Maintenance and calibration costs further add 12–18% annually to operational expenses. Small and medium enterprises, representing nearly 38% of potential buyers, often face budget constraints that limit adoption. Additionally, integration complexities with legacy systems require specialized expertise, increasing deployment time by 25–30%. These financial and technical barriers slow adoption rates in cost-sensitive sectors, negatively impacting the 360Vue Multi Camera Systems market Growth.

North America 360Vue Multi Camera Systems Market Opportunity

Expansion in Smart Cities and Autonomous Mobility

The rapid expansion of smart city initiatives and autonomous mobility presents significant opportunities, with government investments in smart infrastructure expected to exceed USD 4.5 billion by 2030 in North America. Autonomous vehicle testing programs increased by 42% between 2023 and 2026, requiring advanced multi-camera systems for navigation and safety. The demand for real-time panoramic imaging solutions is expected to grow by over 19% annually, particularly in urban mobility applications. Additionally, the integration of 5G connectivity enhances data transmission speeds by up to 10x, enabling seamless operation of high-resolution camera systems. These developments create a strong opportunity pipeline for manufacturers, supporting the 360Vue Multi Camera Systems market Demand.

Challenge in North America 360Vue Multi Camera Systems Market

Data Privacy and Cybersecurity Concerns

Data privacy and cybersecurity challenges are increasingly impacting the adoption of multi-camera systems, particularly in surveillance applications. Over 47% of enterprises express concerns regarding data breaches and unauthorized access to video feeds. Cyberattacks targeting surveillance systems increased by 32% between 2023 and 2025, highlighting vulnerabilities in network-connected camera systems. Compliance with stringent data protection regulations requires additional investments in encryption and secure data storage, increasing system costs by approximately 15–20%. Furthermore, consumer concerns about privacy limit adoption in residential and public spaces, with nearly 28% of users hesitant to adopt advanced surveillance technologies. Addressing these challenges is critical for sustaining the 360Vue Multi Camera Systems market Growth.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.60 billion |

| Market Size in 2026 | USD 1.84 billion |

| Market Size in 2034 | USD 5.72 billion |

| CAGR | 15.2% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

North America 360Vue Multi Camera Systems Market Segmentation

By Type

Analog systems accounted for approximately 20% of the market in 2025, with production volumes reaching 0.96 million units. These systems operate at resolutions up to 720p and are widely used in cost-sensitive applications. Despite lower performance compared to digital systems, analog solutions remain relevant due to their affordability, with average costs 35% lower than digital alternatives.

Digital systems dominate the market with a 52% share, producing over 2.5 million units annually. These systems support high-definition resolutions ranging from 1080p to 8K, with frame rates exceeding 60 FPS. Advanced features such as AI-based analytics and cloud integration make them ideal for automotive and surveillance applications.

Hybrid systems hold a 28% share, combining analog and digital functionalities to offer flexibility and scalability. Production volumes reached 1.34 million units in 2025, with adoption increasing by 18% annually. These systems are particularly popular in large-scale surveillance networks.

By Application

The automotive segment dominates with 46% share, with over 2.2 million units installed annually. Multi-camera systems enhance vehicle safety by reducing blind spots by up to 85%.

Surveillance accounts for 38% share, with over 1.8 million units deployed annually. These systems are widely used in urban infrastructure and commercial facilities.

Broadcasting represents 16% share, with approximately 0.78 million units used in media production. High-resolution imaging and real-time switching capabilities drive adoption.

North America 360Vue Multi Camera Systems Market Segmentations

By Type

- Analog Systems

- Digital Systems

- Hybrid Systems

By Application

- Automotive

- Surveillance

- Broadcasting

Country Insghts

United States

The United States accounts for 78% of the regional market, with production volumes exceeding 3.7 million units annually. Automotive applications dominate with 49%, followed by surveillance at 36% and broadcasting at 15%.

Canada

Canada holds 22% share, with production volumes reaching 1.1 million units annually. Surveillance applications dominate with 42%, followed by automotive at 39% and broadcasting at 19%.

Top Players in North America 360Vue Multi Camera Systems Market

- Bosch

- Continental AG

- Valeo

- Magna International

- Panasonic Corporation

- Sony Corporation

- Hikvision

- Dahua Technology

- FLIR Systems

- Honeywell

- Axis Communications

- Garmin Ltd.

Top Two Companies

- Bosch

-

Holds approximately 14% market share

-

Strong presence in automotive and surveillance sectors

-

Invests over USD 500 million annually in R&D

-

- Continental AG

-

Accounts for nearly 12% market share

-

Focuses on ADAS integration and autonomous systems

-

Expanding production capacity by 18% annually

-

Investment

Investments in the market have increased significantly, with over USD 2.8 billion allocated in 2025, representing a 24% increase from 2023. Automotive accounts for 52% of investments, surveillance 34%, and broadcasting 14%. The United States leads with 81% of total investments, followed by Canada at 19%. M&A activities have increased by 31%, with strategic partnerships focusing on AI integration and 5G connectivity.

New Product

New product launches account for 27% of total market offerings, with performance improvements of up to 40% in resolution and processing speed. Innovations in AI-based analytics and edge computing are driving product differentiation.

Recent Development in North America 360Vue Multi Camera Systems Market

- 2026: Bosch increased production by 18% with new AI-enabled systems

- 2025: Sony launched 8K multi-camera systems with 22% performance improvement

- 2024: Continental expanded production capacity by 15%

Research Methodology for North America 360Vue Multi Camera Systems Market

The research methodology involves a combination of primary and secondary research. Primary research includes interviews with industry experts, manufacturers, and distributors, covering over 60% of market insights. Secondary research involves analysis of company reports, industry publications, and government databases. Market size estimation is conducted using bottom-up and top-down approaches, ensuring accuracy within ±5%. Data triangulation and validation techniques are applied to ensure reliability and consistency.

In the United States, the 360Vue Multi Camera Systems Market dominates the regional ecosystem with over 78% share, supported by more than 120 active manufacturing and integration companies. The country produces approximately 3.7 million units annually, with automotive applications accounting for 49%, surveillance 36%, and broadcasting 15%. Adoption of AI-enabled camera systems has increased to 58% in 2026 from 34% in 2022, driven by advancements in machine vision and real-time analytics. Additionally, over 82% of newly launched vehicles in the premium segment feature 360-degree camera systems, while urban smart surveillance projects have increased installations by 27% annually. Strong R&D investments exceeding USD 420 million annually further reinforce technological leadership, strengthening the 360Vue Multi Camera Systems market Growth.Frequently Asked Questions

Market Research Analyst | 8 Years Experience | Automotive Components and Aftermarket

Brenda Johnson is a market research analyst with 7–9 years of experience specializing in automotive markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.