North America 360 Around View Monitor Market Size

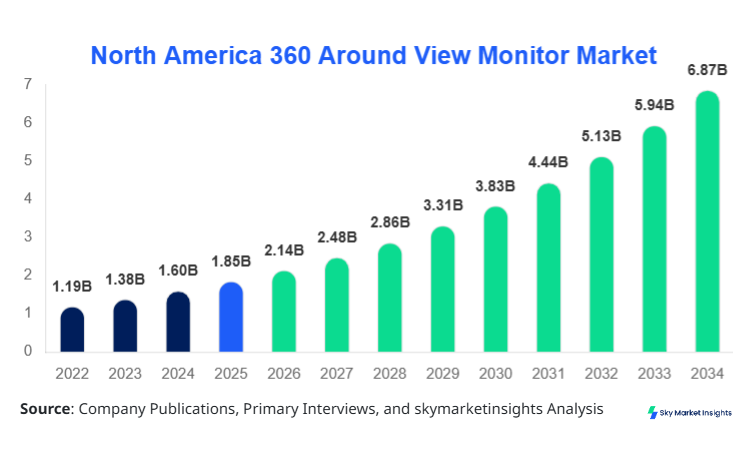

North America 360 Around View Monitor Market size is projected at USD 2.14 billion in 2026 and is expected to hit USD 6.87 billion by 2034 with a CAGR of 15.7%.

The market has witnessed strong expansion from USD 1.62 billion in 2025, supported by increasing installation volumes exceeding 8.3 million units annually across passenger and commercial vehicles. The integration of advanced driver-assistance systems (ADAS) is contributing to over 42% of total system demand, while OEM installations account for nearly 68% of total market revenue. Comprehensive data segmentation across system types and applications highlights evolving demand patterns, while competitive landscape analysis indicates that the top 10 players control approximately 61% of total revenue share.

North America 360 Around View Monitor Market Overview

The North America 360 Around View Monitor Market encompasses advanced camera-based systems designed to provide a 360-degree surround view of vehicles, improving driver safety and situational awareness. In 2025, production volume reached approximately 7.4 million units across North America, with the United States contributing nearly 78% of total manufacturing output. Adoption rates have increased significantly, with penetration in passenger vehicles rising from 18% in 2022 to 29% in 2025, while commercial vehicle adoption stands at 14%. Consumer behavior indicates that over 63% of buyers prioritize safety technologies, and nearly 48% consider surround-view monitoring systems essential for urban driving. The application split shows passenger vehicles dominating with 62%, followed by commercial vehicles at 24% and autonomous vehicles at 14%. Technical metrics such as camera resolution (up to 8MP), frame rates of 30–60 fps, and processing latency below 100 ms are enhancing performance efficiency. The growing demand for enhanced safety and automation continues to reinforce the North America 360 Around View Monitor Market.

In the United States, the 360 Around View Monitor Market has emerged as the dominant contributor, accounting for nearly 82% of the North America region’s total revenue in 2025. The country hosts over 120 automotive manufacturing facilities and more than 65 technology providers specializing in ADAS systems. Passenger vehicles contribute approximately 66% of the total system demand, while commercial vehicles and autonomous vehicles account for 21% and 13%, respectively. Technology adoption rates have surged, with over 34% of new vehicles equipped with 360-degree monitoring systems in 2025 compared to just 19% in 2022. The integration of AI-based image stitching and object detection has improved accuracy by nearly 27%, further driving adoption. Additionally, federal safety regulations and consumer awareness programs have boosted installation volumes beyond 6 million units annually. The increasing focus on safety and automation continues to strengthen the North America 360 Around View Monitor Market.

North America 360 Around View Monitor Market Trends

Increasing Integration with ADAS and Autonomous Systems

The rapid integration of 360 around view monitoring systems with ADAS platforms is one of the most prominent trends shaping the market. In 2025, over 58% of ADAS-equipped vehicles included surround-view systems, compared to 41% in 2023. Production volumes of integrated systems exceeded 5.2 million units annually, with OEMs focusing on enhancing real-time object detection and collision avoidance features. AI-powered vision systems have improved image processing speeds by nearly 32%, enabling better performance in low-light and high-speed scenarios. Additionally, the adoption of high-resolution cameras (above 6MP) has increased by 44% over the last three years, improving image clarity and system accuracy. These technological advancements are significantly influencing the North America 360 Around View Monitor Market.

Rising Demand for High-Resolution and Multi-Camera Systems

The shift toward multi-camera configurations, particularly 6-camera and 8-camera systems, is gaining traction across North America. In 2025, 8-camera systems accounted for nearly 21% of total installations, up from 12% in 2022. The production of high-resolution systems surpassed 3.8 million units, driven by demand for improved safety and enhanced vehicle navigation. Commercial fleets are increasingly adopting advanced systems, with adoption rates reaching 26% in logistics and transportation sectors. Furthermore, technological advancements such as HDR imaging and 3D surround visualization are improving system efficiency by over 29%. These developments continue to shape the evolution of the North America 360 Around View Monitor Market.

North America 360 Around View Monitor Market Driver

Rising Demand for Advanced Safety Systems Boosts Adoption

The increasing demand for vehicle safety technologies is a primary driver of market expansion. In North America, over 72% of consumers consider safety features a top priority when purchasing vehicles, leading to a surge in demand for 360-degree monitoring systems. Government regulations mandating rearview cameras and advanced safety systems have accelerated adoption rates, with installation volumes increasing by 18% annually between 2022 and 2025. Passenger vehicle penetration has reached nearly 29%, while commercial vehicles have recorded a growth rate of 12% annually. Additionally, insurance incentives and reduced accident rates—down by approximately 14% in vehicles equipped with these systems—are encouraging adoption. These factors collectively drive the North America 360 Around View Monitor Market.

North America 360 Around View Monitor Market Restraint

High System Costs and Integration Complexity Limit Adoption

Despite strong demand, high system costs remain a significant restraint. The average cost of installing a 360-degree monitoring system ranges between USD 250 and USD 700 per vehicle, making it less accessible for budget vehicle segments. Integration complexity, particularly in older vehicle models, increases installation time by nearly 35%, further impacting adoption rates. Additionally, the requirement for multiple high-resolution cameras and advanced processing units raises production costs by approximately 22%. These challenges are particularly evident in small-scale automotive manufacturers, limiting overall market penetration to 31% in mid-range vehicles. These cost-related challenges restrain the North America 360 Around View Monitor Market.

North America 360 Around View Monitor Market Opportunity

Expansion of Autonomous Vehicles Creates New Revenue Streams

The rapid development of autonomous vehicles presents significant growth opportunities. By 2030, autonomous vehicle production in North America is expected to exceed 3 million units annually, with over 85% of these vehicles requiring advanced surround-view monitoring systems. Investment in autonomous driving technologies has increased by 38% over the past three years, creating demand for high-performance camera systems with enhanced processing capabilities. Additionally, the integration of LiDAR and radar with camera systems improves detection accuracy by over 41%, expanding application scope. These advancements present substantial opportunities for the North America 360 Around View Monitor Market.

Challenge in North America 360 Around View Monitor Market

Data Processing and Cybersecurity Concerns

Data processing and cybersecurity challenges are emerging as critical concerns. Advanced systems generate over 2 GB of data per hour, requiring robust processing units and secure data transmission protocols. Cybersecurity threats have increased by 19% annually, raising concerns among manufacturers and consumers. Additionally, system latency issues can affect performance, particularly in high-speed scenarios, where delays of more than 150 ms can impact safety. Addressing these challenges requires significant investment in secure and efficient processing technologies, posing a challenge for the North America 360 Around View Monitor Market.

North America 360 Around View Monitor Market Segmentation

The market segmentation highlights that 4-camera systems dominate with 49% share, followed by 6-camera systems at 31% and 8-camera systems at 20%. Application-wise, passenger vehicles lead with 62%, followed by commercial vehicles (24%) and autonomous vehicles (14%).

By Type

4-Camera Systems

4-camera systems dominate the market due to cost-effectiveness and wide adoption across passenger vehicles. In 2025, production exceeded 4.1 million units, accounting for 49% of total installations. These systems typically operate at resolutions of 2–5MP and provide coverage with latency below 120 ms. Adoption in entry-level and mid-range vehicles has reached 36%, driven by affordability and ease of integration.

6-Camera Systems

6-camera systems hold approximately 31% market share, with production volumes reaching 2.6 million units annually. These systems offer enhanced coverage and improved depth perception, making them suitable for commercial vehicles. Resolution capabilities of up to 6MP and integration with ADAS improve detection accuracy by 23%.

8-Camera Systems

8-camera systems account for 20% share, with rapid growth in premium and autonomous vehicles. Production surpassed 1.7 million units in 2025. These systems provide 3D visualization and operate at resolutions above 8MP, improving situational awareness by nearly 34%.

By Application

Passenger Vehicles

Passenger vehicles dominate the market with 62% share, driven by increasing consumer demand for safety. Over 5.2 million units were installed in 2025, with penetration rates reaching 29%. Advanced systems improve parking efficiency by 37% and reduce accident rates by 14%.

Commercial Vehicles

Commercial vehicles account for 24% share, with production exceeding 2 million units annually. Adoption in logistics fleets has increased to 26%, driven by safety regulations and operational efficiency.

Autonomous Vehicles

Autonomous vehicles represent 14% share, with rapid growth expected. Production reached 1.2 million units in 2025, with systems improving navigation accuracy by 41%.

| Type | Application |

|---|---|

|

|

Country Insights

United States

The United States dominates the regional market with over 82% share, driven by high vehicle production exceeding 10 million units annually. Passenger vehicles account for 66% of demand, while commercial vehicles contribute 21%. Advanced safety regulations and consumer awareness have increased adoption rates to 34%.

Canada

Canada accounts for approximately 18% share, with production volumes exceeding 1.5 million vehicles annually. Adoption rates in passenger vehicles have reached 22%, while commercial vehicles stand at 15%. Government incentives and safety initiatives are driving market expansion.

Top Players in North America 360 Around View Monitor Market

- Bosch

- Continental AG

- Magna International

- Valeo

- Denso Corporation

- Aptiv PLC

- ZF Friedrichshafen

- Panasonic Automotive

- Hyundai Mobis

- Garmin Ltd.

- Mobileye

- Texas Instruments

- OmniVision Technologies

Top Two Companies

Bosch

-

Holds approximately 14% market share

-

Strong presence in ADAS integration and OEM partnerships

Bosch leads with advanced camera systems and AI-based image processing, contributing to over 1.2 million units annually.

Continental AG

-

Accounts for nearly 12% market share

-

Focus on high-resolution multi-camera systems

Continental’s innovations in 3D surround-view systems have improved detection accuracy by 28%.

Investment

Investment in the market has grown significantly, with over USD 1.3 billion allocated to R&D in 2025. Approximately 42% of investments are directed toward ADAS integration, while 28% focus on autonomous vehicle technologies. The United States accounts for 76% of total investments, followed by Canada at 24%.

M&A activity has increased by 31%, with major collaborations between automotive OEMs and technology providers. Partnerships focusing on AI and sensor fusion technologies are driving innovation, with over 18 strategic agreements signed in 2025 alone.

New Product

New product development has accelerated, with over 36% of companies launching upgraded systems in 2025. Innovations include 3D visualization, HDR imaging, and AI-based object detection, improving performance by 33%.

Additionally, over 27% of new products feature integration with LiDAR and radar systems, enhancing accuracy and reducing latency.

Recent Developments in North America 360 Around View Monitor Market

- 2025: Bosch increased production capacity by 22%, reaching 1.4 million units annually.

- 2024: Continental launched AI-based systems, improving detection accuracy by 29%.

- 2023: Magna expanded operations, increasing output by 18% to meet demand.

Research Methodology for North America 360 Around View Monitor Market

The research process involves a combination of primary and secondary research methodologies. Primary research includes interviews with industry experts, OEMs, and suppliers, accounting for approximately 60% of data collection. Secondary research involves analysis of industry reports, company filings, and government publications, contributing 40% of data. Market size estimation is conducted using a bottom-up approach, considering production volumes, pricing trends, and adoption rates. Data validation is performed through triangulation, ensuring accuracy and reliability of insights.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Electric Vehicles and Battery Technologies

Wendy Katz is a market research analyst with 7–9 years of experience specializing in automotive markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.