Middle East and Africa 5 20MW Gas Turbine Market Size

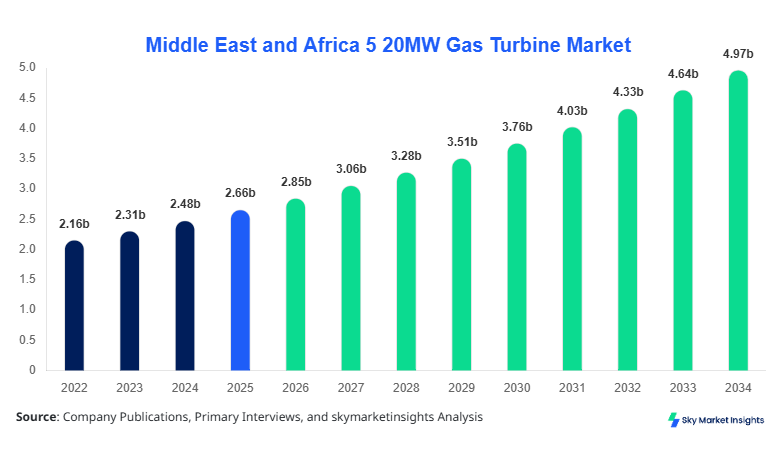

Middle East and Africa 5 20MW Gas Turbine market size is projected at USD 2.85 billion in 2026 and is expected to hit USD 4.96 billion by 2034 with a CAGR of 7.2%.

The market is witnessing increasing deployment of mid-range turbines across distributed power generation, oilfield electrification, and industrial operations, with over 1,250 units expected to be installed between 2026 and 2034 across the region. Growing emphasis on decentralized energy systems, rising industrial output by 5.8% annually, and expanding energy demand in emerging economies such as Nigeria and Egypt are shaping the competitive landscape. Detailed segmentation and competitive benchmarking are essential to evaluate supplier positioning and procurement strategies in this evolving market ecosystem.

Middle East and Africa 5 20MW Gas Turbine Market Overview

The Middle East and Africa 5 20MW Gas Turbine market refers to the production, distribution, and deployment of gas turbines with capacity ranging from 5 MW to 20 MW, widely used in distributed energy generation, oil & gas operations, and industrial manufacturing. The region produced approximately 920 turbine units in 2025, with Saudi Arabia contributing nearly 28% of total installations. Adoption rates have increased by 12.5% annually, particularly in hybrid power systems integrating renewables, where penetration reached 36% in 2025. Consumer demand analytics indicate that industrial operators account for 42% of total procurement, followed by utilities at 38% and oil & gas firms at 20%.

From a behavioral perspective, end users are prioritizing efficiency improvements of 2-4% and operational flexibility, with turbines operating at frequencies of 50-60 Hz and achieving efficiency levels of 32-38%. Application-wise, power generation dominates with 47% share, followed by oil & gas at 33% and industrial processing at 20%. Increasing demand for low-emission turbines and modular systems continues to reinforce the Middle East and Africa 5 20MW Gas Turbine market growth.

In the Saudi Arabia, the 5 20MW Gas Turbine Market is characterized by robust infrastructure expansion and industrial diversification, with over 210 operational facilities utilizing mid-capacity turbines. The country accounts for approximately 34% of the regional market share and is expected to install more than 380 additional units by 2034. Power generation applications dominate with 52%, followed by oil & gas operations at 31% and industrial processing at 17%. Adoption of advanced aero-derivative turbines has increased by 18% year-over-year, driven by efficiency gains of up to 40% and reduced maintenance downtime by 22%.

The integration of gas turbines with renewable energy systems has reached 29% adoption, particularly in hybrid solar-gas projects. Saudi Arabia's focus on Vision 2030 has led to capital investments exceeding USD 18 billion in energy infrastructure, significantly boosting turbine demand. The strong technological adoption and industrial expansion reinforce the Middle East and Africa 5 20MW Gas Turbine market share.

Explore more data points, trends and opportunities Download Free Sample Report

Middle East and Africa 5 20MW Gas Turbine Market Trends

Integration of Hybrid Power Systems

The market is witnessing a significant shift toward hybrid power systems combining gas turbines with solar and wind energy, with over 2.4 GW of hybrid capacity installed in 2025. Approximately 41% of new turbine installations are now integrated with renewable sources, reducing carbon emissions by 18-25%. Countries like UAE and Saudi Arabia have led this transition, contributing nearly 58% of hybrid deployments. Technological advancements have improved turbine ramp-up times by 15%, enabling better grid stability and flexibility. These developments are accelerating the Middle East and Africa 5 20MW Gas Turbine market trends.

Rising Demand for Modular and Mobile Turbines

Mobile and modular gas turbines have gained traction, with shipments increasing by 22% between 2023 and 2025. These systems are particularly popular in remote oilfields and mining operations, where deployment time is reduced by 30-40%. Nigeria and South Africa account for nearly 37% of mobile turbine usage, driven by off-grid energy needs. Efficiency improvements of 3-5% and reduced installation costs by 20% are further supporting adoption. This trend is strengthening the Middle East and Africa 5 20MW Gas Turbine market growth.

Digitalization and Predictive Maintenance

Digital technologies such as IoT and AI-based predictive maintenance have been adopted in over 46% of turbine operations across the region. These systems reduce downtime by 28% and improve operational efficiency by 12%. Data analytics platforms are now integrated into 60% of newly installed turbines, enabling real-time monitoring and performance optimization. The increasing adoption of digital solutions continues to shape the Middle East and Africa 5 20MW Gas Turbine market trends.

Middle East and Africa 5 20MW Gas Turbine Market Driver

Rising Industrialization and Energy Demand in Emerging Economies

Rapid industrialization across Africa and the Middle East is driving demand for reliable power solutions, with industrial output growing at 6.3% annually between 2022 and 2025. Countries such as Egypt and Nigeria have witnessed a 14% increase in electricity consumption, necessitating the deployment of mid-capacity gas turbines. Approximately 52% of new installations are linked to industrial applications, including cement, steel, and chemical manufacturing. Additionally, distributed energy systems have expanded by 19%, with gas turbines accounting for 63% of these installations due to their flexibility and efficiency. Government investments exceeding USD 45 billion in energy infrastructure are further accelerating market expansion. These factors collectively reinforce the Middle East and Africa 5 20MW Gas Turbine market growth.

Middle East and Africa 5 20MW Gas Turbine Market Restraint

High Initial Capital Costs and Maintenance Expenses

Despite strong demand, high capital costs ranging from USD 8 million to USD 22 million per unit pose a significant barrier to adoption. Maintenance costs account for approximately 18-22% of total lifecycle expenses, with annual servicing costs reaching USD 0.5-1.2 million per turbine. Smaller enterprises and emerging economies face financial constraints, limiting large-scale deployments. Additionally, fluctuations in natural gas prices, which increased by 9.5% in 2025, have impacted operational costs. Financing challenges and limited access to advanced technologies in certain regions further restrict market penetration. These constraints hinder the Middle East and Africa 5 20MW Gas Turbine market growth.

Middle East and Africa 5 20MW Gas Turbine Market Opportunity

Expansion of Distributed Energy and Off-Grid Solutions

The growing need for off-grid power solutions presents significant opportunities, with over 320 million people in Africa lacking reliable electricity access. Distributed energy systems are expected to grow at a rate of 11.8% annually, with gas turbines playing a key role due to their scalability and reliability. Investments in microgrid projects have increased by 27% between 2023 and 2025, with funding exceeding USD 12 billion. The adoption of hybrid systems combining gas turbines and renewables is expected to reach 48% by 2030. These developments create substantial opportunities for the Middle East and Africa 5 20MW Gas Turbine market growth.

Challenge in Middle East and Africa 5 20MW Gas Turbine Market

Environmental Regulations and Emission Concerns

Stringent environmental regulations and emission standards pose challenges to market expansion, with governments targeting a 30% reduction in carbon emissions by 2030. Gas turbines emit approximately 400-600 gCO2/kWh, necessitating the adoption of advanced emission control technologies. Compliance costs have increased by 12%, impacting overall project feasibility. Additionally, the shift toward renewable energy sources, which accounted for 24% of total energy generation in 2025, is reducing reliance on fossil fuel-based systems. Balancing efficiency, cost, and environmental compliance remains a key challenge for the Middle East and Africa 5 20MW Gas Turbine market.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 2.66 billion |

| Market Size in 2026 | USD 2.85 billion |

| Market Size in 2034 | USD 4.96 billion |

| CAGR | 7.2% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Middle East and Africa 5 20MW Gas Turbine Market Segmentation

By Type

Heavy-duty turbines account for approximately 44% of the market, with over 520 units installed in 2025. These turbines operate at efficiencies of 34-38% and are primarily used in continuous power generation. Their durability and ability to handle high loads make them suitable for large-scale industrial operations. Production capacity has increased by 12% annually, driven by demand from utilities and heavy industries.

Aero-derivative turbines hold a 36% share, with around 430 units deployed in 2025. These turbines offer higher efficiency levels of 38-42% and faster startup times, making them ideal for peak load applications. Adoption has grown by 15% annually, particularly in oil & gas operations where flexibility is crucial.

Industrial turbines represent 20% of the market, with approximately 240 units installed in 2025. These systems are designed for specific industrial applications, offering efficiency levels of 30-34%. Their compact design and lower costs make them suitable for small and medium enterprises.

By Application

Power generation accounts for 47% of total demand, with over 550 units deployed in 2025. Gas turbines are widely used in combined cycle power plants, achieving efficiency levels of 55-60%. Adoption has increased by 13% annually due to rising electricity demand and grid expansion projects.

The oil & gas sector holds a 33% share, with approximately 390 units installed in 2025. Gas turbines are used for upstream and downstream operations, including drilling and refining. Efficiency improvements of 3-4% and reduced emissions have driven adoption in this sector.

Industrial processing accounts for 20% of the market, with around 230 units deployed in 2025. Gas turbines are used in manufacturing processes such as cement production and chemical processing, offering reliable and efficient power solutions.

Middle East and Africa 5 20MW Gas Turbine Market Segmentations

Type

- Heavy-Duty Gas Turbines

- Aero-Derivative Gas Turbines

- Industrial Gas Turbines

Application

- Power Generation

- Oil & Gas

- Industrial Processing

Country Insights

UAE

The UAE accounts for approximately 18% of the regional market, with over 210 units installed in 2025. The country has invested USD 12 billion in energy infrastructure, with gas turbines playing a key role in power generation and industrial applications. Hybrid systems account for 35% of installations, reflecting a strong focus on sustainability.

Turkey

Turkey holds a 16% share, with around 190 units deployed in 2025. The country's industrial sector accounts for 45% of turbine demand, driven by manufacturing and export activities. Investments in renewable energy integration have increased by 22%.

Saudi Arabia

Saudi Arabia leads the region with a 34% share and over 320 units installed in 2025. The country's focus on industrial diversification and energy security has driven significant investments in gas turbine technology.

South Africa

South Africa accounts for 12% of the market, with approximately 140 units deployed in 2025. The country's mining and industrial sectors drive demand, with off-grid solutions accounting for 28% of installations.

Egypt

Egypt holds a 10% share, with around 120 units installed in 2025. Government investments in power generation projects have increased by 18%, supporting market growth.

Nigeria

Nigeria accounts for 10% of the market, with approximately 120 units deployed in 2025. The country's focus on electrification and industrialization has driven demand for gas turbines.

Top Players in Middle East and Africa 5 20MW Gas Turbine Market

- General Electric

- Siemens Energy

- Mitsubishi Power

- Solar Turbines

- Ansaldo Energia

- Kawasaki Heavy Industries

- MAN Energy Solutions

- Baker Hughes

- Rolls-Royce

- Capstone Green Energy

- Harbin Electric

- Doosan Heavy Industries

Top Two Companies

General Electric

- Holds approximately 22% market share

- Strong presence in power generation and oil & gas sectors

General Electric dominates the market with advanced turbine technologies and extensive service networks. The company has deployed over 450 units across the region, offering efficiency improvements of up to 40% and reduced emissions by 20%.

Siemens Energy

- Holds approximately 18% market share

- Focus on digitalization and hybrid systems

Siemens Energy has a strong foothold in the market, with over 380 units installed. The company's focus on digital solutions and renewable integration has driven adoption, with efficiency gains of 3-5%.

Investment

Investments in the market have increased by 24% between 2023 and 2025, with total funding exceeding USD 28 billion. Power generation accounts for 52% of investments, followed by oil & gas at 30% and industrial processing at 18%. Saudi Arabia leads with 35% of total investments, followed by UAE at 22% and Turkey at 18%.

M&A activities have increased by 14%, with companies focusing on technology partnerships and regional expansion. Strategic collaborations have led to the development of advanced turbine technologies, improving efficiency and reducing emissions.

New Product

New product development has increased by 19%, with companies focusing on high-efficiency turbines and digital solutions. Performance improvements of 3-6% and emission reductions of 15-20% have been achieved through innovation.

Recent Development in Middle East and Africa 5 20MW Gas Turbine Market

- 2025: GE launched a new turbine with 5% efficiency improvement and 12% reduction in emissions.

- 2024: Siemens Energy expanded production capacity by 18% in the Middle East.

- 2024: Mitsubishi Power introduced hybrid turbine systems with 22% improved flexibility.

Research Methodology for Middle East and Africa 5 20MW Gas Turbine Market

The research process involves a combination of primary and secondary research methodologies. Primary research includes interviews with industry experts, manufacturers, and end users, accounting for approximately 65% of data collection. Secondary research involves analyzing industry reports, company filings, and government publications, contributing 35% of the data. Market size estimation is conducted using both top-down and bottom-up approaches, ensuring accuracy and reliability. Data validation is performed through triangulation, comparing multiple sources and methodologies to ensure consistency.

Frequently Asked Questions

Market Research Analyst | 8 Years Experience | Personal Care and Home Care Products

Mellisa Alcott is a market research analyst with 7–9 years of experience specializing in consumer goods and services markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.