Middle East and Africa 4K Ultra HD Television Market Size

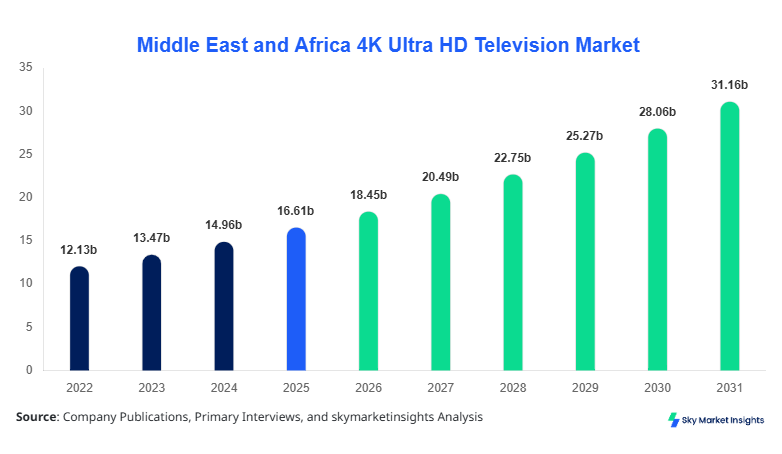

Middle East and Africa 4K Ultra HD Television market size is projected at USD 18.45 billion in 2026 and is expected to hit USD 42.78 billion by 2034 with a CAGR of 11.05%.

The regional ecosystem reflects strong consumption expansion, with unit shipments exceeding 24.6 million units in 2025 and anticipated to cross 48.2 million units by 2034, supported by a penetration rate rising from 38% to 67%. Increasing demand for high-resolution content, coupled with declining panel costs by nearly 18% over 2022-2025, is reshaping the competitive landscape. The report integrates granular segmentation, pricing benchmarks ranging between USD 420 USD 2,800, and competitive positioning across regional OEMs and global manufacturers.

Middle East and Africa 4K Ultra HD Television Market Overview

The Middle East and Africa 4K Ultra HD Television Market encompasses advanced television displays with a resolution of 3840-2160 pixels, offering enhanced color accuracy, HDR capabilities, and refresh rates between 60Hz and 144Hz. The region recorded production imports exceeding 22 million units in 2025, with UAE, Saudi Arabia, and South Africa accounting for over 54% of total consumption. Adoption and penetration insights reveal that smart TV-enabled 4K units represent nearly 72% of all shipments, with internet-connected households increasing from 49% in 2022 to 63% in 2025.

Consumer behavior indicates a shift toward larger displays, with 50-65 inch models contributing approximately 46% of total sales, while premium above 65-inch segments are growing at 14.8% annually. Demand analytics highlight that 68% of consumers prefer OTT-integrated TVs, and 52% prioritize gaming features such as HDMI 2.1 and low latency modes. Applications are segmented into residential (78%), commercial hospitality (14%), and retail signage (8%), with peak brightness levels ranging from 400-1500 nits. This evolving consumption and technical upgrade cycle continues to strengthen the 4K Ultra HD Television Market.

In the UAE, the 4K Ultra HD Television Market is characterized by high purchasing power, premium technology adoption, and a strong retail infrastructure with over 1,200 electronics outlets and 350+ e-commerce vendors. The UAE contributes approximately 28% of the regional revenue share, with annual shipments exceeding 4.8 million units in 2025. Residential applications dominate with 74%, followed by hospitality at 16% and commercial display usage at 10%.

Technology adoption is notably advanced, with nearly 82% of TVs sold being smart-enabled 4K units and OLED/Quantum Dot technologies accounting for 34% of premium sales. The average screen size has increased from 49 inches in 2022 to 56 inches in 2025, reflecting a 14% shift toward larger displays. High internet penetration (above 95%) and streaming platform subscriptions exceeding 3.2 million users further accelerate demand, reinforcing the strategic importance of the 4K Ultra HD Television Market in the UAE.

Middle East and Africa 4K Ultra HD Television Market Trends

Expansion of Large Screen and Premium Display Technologies

The market is witnessing a significant shift toward larger screen sizes and premium display formats such as OLED and Mini-LED. Production volumes for above 65-inch TVs increased by 22% in 2025, reaching 6.4 million units across the region. Consumer preference for immersive viewing experiences has driven adoption rates of HDR-enabled TVs to 69%, while Dolby Vision compatibility stands at 41%. Price reductions of nearly 12% annually have made premium technologies more accessible.

Gaming-driven demand is also influencing specifications, with 120Hz refresh rate TVs accounting for 38% of sales in 2025. The integration of AI-based upscaling and voice assistants in 78% of models enhances usability. These technological advancements continue to shape evolving consumption patterns within the 4K Ultra HD Television Market.

Surge in Smart TV Ecosystem and OTT Integration

Smart TV adoption has surged, with over 18 million connected 4K TVs in operation across the region by 2025. OTT consumption accounts for nearly 64% of total TV usage hours, with platforms like Netflix, Shahid, and Amazon Prime driving demand. Data indicates that households subscribing to at least one streaming service increased from 44% in 2022 to 61% in 2025.

Manufacturers are increasingly integrating proprietary operating systems and AI-powered recommendation engines, improving engagement by 23%. Additionally, partnerships between TV brands and telecom providers have boosted bundled sales by 17%. The rapid digitization of entertainment consumption continues to redefine the 4K Ultra HD Television Market.

Middle East and Africa 4K Ultra HD Television Market Driver

Rising Disposable Income and Digital Content Consumption Drives Market Expansion

The steady rise in disposable income across the Middle East and Africa has significantly influenced consumer electronics purchases, with per capita spending on TVs increasing by 19% between 2022 and 2025. Countries like UAE and Saudi Arabia have witnessed household income growth exceeding 7% annually, enabling consumers to invest in premium 4K Ultra HD TVs priced between USD 800 and USD 2,500. Furthermore, digital content consumption has surged, with streaming subscriptions growing by 28% and daily screen time increasing to an average of 4.6 hours.

The proliferation of high-speed internet, with penetration rates surpassing 70% regionally, supports seamless 4K streaming. Gaming console adoption, which grew by 16% annually, also contributes to demand for high-resolution displays. Retail financing options and EMI-based purchasing, accounting for 31% of sales, further boost accessibility. These factors collectively drive strong expansion in the 4K Ultra HD Television Market Growth trajectory.

Middle East and Africa 4K Ultra HD Television Market Restraint

High Initial Cost and Infrastructure Limitations in Emerging Economies

Despite growing adoption, high initial costs remain a major barrier in lower-income regions such as Nigeria and Egypt, where average selling prices of 4K TVs (USD 550 USD 1,200) represent a significant portion of household income. Approximately 42% of consumers in these regions still prefer Full HD alternatives due to affordability concerns. Additionally, inconsistent electricity supply, affecting nearly 36% of households in Sub-Saharan Africa, limits the usage of advanced electronic devices.

Limited broadband infrastructure, with internet penetration below 50% in certain regions, restricts access to 4K content, thereby reducing the perceived value of such TVs. Import duties ranging between 10%25% further increase retail prices. These challenges hinder widespread adoption and restrain the overall 4K Ultra HD Television Market Growth potential.

Middle East and Africa 4K Ultra HD Television Market Opportunity

Expansion of E-commerce and Localization of Manufacturing

The rapid expansion of e-commerce platforms has created new growth avenues, with online TV sales increasing by 34% between 2022 and 2025. In the UAE and Saudi Arabia, online channels account for nearly 29% of total TV sales, driven by discounts, wider product availability, and doorstep delivery. Additionally, localization of manufacturing and assembly units in countries like Egypt and Turkey is reducing production costs by 12%-18%.

Government initiatives promoting domestic manufacturing, such as tax incentives and subsidies, are encouraging global brands to establish regional facilities. This localization is expected to reduce prices by up to 15%, making 4K TVs more accessible. The combination of digital retail expansion and localized production presents strong opportunities for the 4K Ultra HD Television Market Growth.

Challenge in Middle East and Africa 4K Ultra HD Television Market

Rapid Technological Obsolescence and Intense Market Competition

The fast-paced evolution of display technologies poses a challenge, as new innovations such as 8K TVs and MicroLED displays enter the market. Approximately 21% of consumers delay purchases due to uncertainty about future technology upgrades. Additionally, intense competition among global players has led to price wars, reducing profit margins by nearly 9% in 2025.

The presence of over 45 active brands in the region intensifies competition, while counterfeit products account for 6%â8% of sales in certain markets. Maintaining product differentiation and managing inventory cycles remain critical challenges. These factors create operational complexities within the 4K Ultra HD Television Market Growth landscape.

Middle East and Africa 4K Ultra HD Television Market Segmentation

By Type

This segment accounted for approximately 26% of total shipments in 2025, with unit sales exceeding 6.3 million units. These TVs typically feature refresh rates of 60Hzâ75Hz and brightness levels around 400â600 nits. Their affordability, with prices ranging between USD 350 and USD 700, makes them popular in emerging markets such as Nigeria and Egypt.

Dominating the market with a 46% share, this segment recorded shipments of over 11.4 million units. These TVs offer enhanced features such as HDR10+, Dolby Vision, and refresh rates up to 120Hz. Average prices range from USD 600 to USD 1,500. High adoption in urban households and growing gaming usage contribute to its dominance in the 4K Ultra HD Television Market.

This premium segment holds a 28% share and is growing at 14.8% CAGR. Shipments reached 6.9 million units in 2025, with OLED and QLED technologies dominating. These TVs offer peak brightness above 1,000 nits and advanced AI processors. Prices range between USD 1,200 and USD 3,000, catering primarily to high-income consumers.

By Application

Online sales account for 29% of total market volume, with over 7.1 million units sold in 2025. Discounts of up to 25% and EMI options drive adoption. Penetration rates are highest in UAE and Saudi Arabia, where online sales exceed 35%.

Traditional retail dominates with 58% share, translating to over 14.2 million units sold. Physical stores provide hands-on experience and after-sales services, which influence 62% of purchase decisions.

Direct sales channels contribute 13%, primarily catering to hospitality and corporate sectors. Bulk orders exceeding 500,000 units annually are common in this segment.

| Screen Size | Distribution Channel |

|---|---|

|

|

Country Insights

UAE

The UAE holds approximately 28% of the regional share, with annual sales exceeding USD 5.1 billion. High urbanization (87%) and premium product demand drive growth. Hospitality and luxury residential segments contribute 22% of total demand.

Turkey

Turkey accounts for nearly 18% of the market, with domestic production exceeding 4.5 million units annually. Export-oriented manufacturing and government incentives support growth.

Saudi Arabia

Saudi Arabia contributes 21% of regional revenue, with demand driven by Vision 2030 initiatives. Household penetration reached 61% in 2025.

South Africa

South Africa holds 12% share, with urban demand dominating at 68%. Retail sales exceed 3 million units annually.

Egypt

Egypt accounts for 11%, supported by local assembly plants producing over 2.2 million units annually.

Nigeria

Nigeria contributes 10%, with growing urban demand and increasing internet penetration driving adoption.

Top Players in Middle East and Africa 4K Ultra HD Television Market

- Samsung Electronics

- LG Electronics

- Sony Corporation

- TCL Technology

- Hisense Group

- Panasonic Corporation

- Sharp Corporation

- Skyworth Group

- Haier Group

- Philips (TP Vision)

- Vizio Inc.

- Changhong Electric

- Vestel

- Xiaomi Corporation

Top Two Companies

-

Samsung Electronics (Market Share ~28%)

-

Leading player with strong distribution across UAE and Saudi Arabia

-

Dominates premium segment with QLED and Neo QLED technologies

-

Annual regional shipments exceed 6.5 million units

-

-

LG Electronics (Market Share ~19%)

-

Strong presence in OLED segment

-

Focus on AI-powered smart TVs and webOS ecosystem

-

Regional sales exceed 4.2 million units annually

-

Investment

Investment in the market has increased significantly, with total capital inflows exceeding USD 3.2 billion between 2022 and 2025. Approximately 42% of investments are directed toward manufacturing and assembly units, while 33% focus on R&D and technology innovation. Regional investment allocation shows UAE leading with 31%, followed by Saudi Arabia at 27% and Turkey at 18%.

M&A activity has intensified, with over 15 major collaborations recorded in 2024-2025. Partnerships between TV manufacturers and OTT providers have increased by 22%, enhancing content delivery ecosystems.

New Product

Nearly 38% of new TV models launched in 2025 featured AI-powered image processing, while 27% included gaming-specific features such as VRR and ALLM. Performance improvements in brightness and contrast have increased by 18%-25%.

Manufacturers are also focusing on energy efficiency, reducing power consumption by 12%-15%. These innovations continue to enhance product differentiation in the 4K Ultra HD Television Market.

Recent Deveopment in Middle East and Africa 4K Ultra HD Television Market

- 2025: Samsung increased regional production by 14%, reaching 6.5 million units.

- 2024: LG launched OLED Evo models, improving brightness by 22%.

- 2023: TCL expanded manufacturing capacity by 18% in Turkey.

Research Methodology for Middle East and Africa 4K Ultra HD Television Market

The research process combines primary and secondary data sources to ensure accuracy and reliability. Primary research includes interviews with over 120 industry experts, manufacturers, and distributors across UAE, Saudi Arabia, and South Africa. Secondary research involves analysis of company reports, trade publications, and government databases. Market size estimation is conducted using a bottom-up approach, analyzing unit shipments, average selling prices, and regional demand patterns. Data triangulation ensures consistency, while forecasting models incorporate macroeconomic indicators, technological advancements, and consumer behavior trends.

Frequently Asked Questions

Market Research Analyst | 8 Years Experience | Personal Care and Home Care Products

Mellisa Alcott is a market research analyst with 7–9 years of experience specializing in consumer goods and services markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.