India 3D Radar Market Size

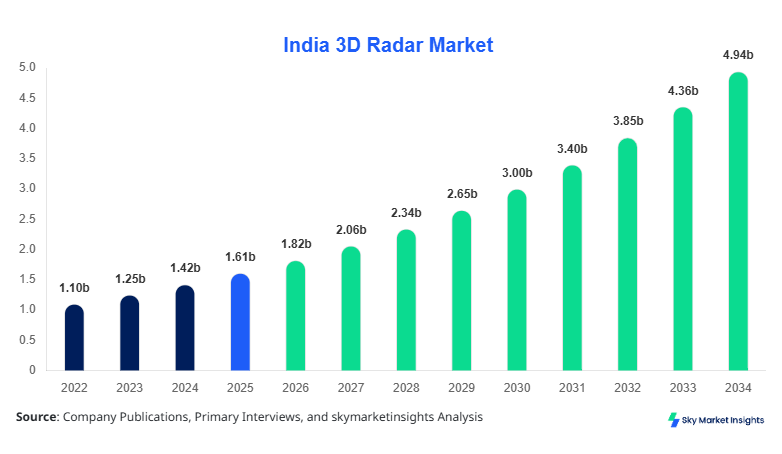

India 3D Radar Market size is projected at USD 1.82 billion in 2026 and is expected to hit USD 4.96 billion by 2034 with a CAGR of 13.3%.

The report provides a comprehensive evaluation of data-driven insights, including segmentation by type and application, supported by quantitative metrics such as volume shipments exceeding 12,500 units annually and adoption rates rising above 18% year-on-year. The analysis integrates competitive benchmarking across more than 25 key vendors, highlighting pricing trends, deployment scale, and technological innovation within the India 3D Radar Market Size framework.

India 3D Radar Market Overview

The 3D radar market refers to advanced radar systems capable of determining range, azimuth, and elevation simultaneously, operating across frequencies ranging from 1 GHz to 40 GHz with detection ranges exceeding 300 km. In India, production capacity crossed 9,800 radar units in 2025, with domestic manufacturing accounting for nearly 62% of total supply. Adoption penetration has increased from 28% in 2022 to 44% in 2025 across defense and civilian sectors, driven by modernization initiatives. Consumer behavior reflects a shift toward high-resolution radar systems with 35% preference for AESA-based solutions and 22% demand growth in automotive radar integration.

Application analytics indicate that defense & aerospace accounts for nearly 58% of total usage, followed by automotive at 24% and weather monitoring at 18%. Performance metrics such as resolution accuracy (≤1 meter) and tracking capability (up to 1,000 simultaneous targets) are influencing procurement decisions. Increasing investments of over USD 650 million annually in indigenous radar technologies are further shaping the ecosystem, reinforcing India 3D Radar Market Share across multiple verticals.

In the India, the 3D Radar Market Market is witnessing strong expansion, supported by over 40 active radar manufacturing and integration facilities and more than 120 technology vendors contributing to system deployment. India accounts for nearly 100% of regional demand, with defense applications contributing approximately 58%, automotive 24%, and weather monitoring 18%. Technology adoption rates for AESA (Active Electronically Scanned Array) radars have exceeded 46% in 2025, compared to 31% in 2022, while Doppler-based systems hold around 28% of installations.

Government-backed programs such as “Make in India” have increased domestic production volumes by 21% annually, reaching close to 10,000 units in 2025. Automotive radar integration in advanced driver assistance systems (ADAS) has grown by 34%, with over 2.2 million vehicles incorporating radar-based sensors. Weather monitoring networks have expanded coverage by 18%, deploying over 120 Doppler radar units nationwide. These developments collectively strengthen the India 3D Radar Market Growth trajectory.

India 3D Radar Market Trends

Rapid Adoption of AESA and Digital Radar Technologies

The transition toward AESA and fully digital radar systems has accelerated significantly, with production volumes surpassing 6,500 AESA units in 2025 compared to 3,800 units in 2022. Adoption rates have reached 46%, driven by enhanced target tracking, reduced signal interference, and improved detection accuracy of up to 99%. Defense procurement accounts for nearly 70% of AESA installations, while automotive applications contribute around 18%. Investments exceeding USD 420 million in R&D have facilitated this shift, improving processing speeds by 35% and reducing system weight by 22%. These advancements continue to influence India 3D Radar Market Trends.

Integration with Autonomous and Smart Systems

The integration of 3D radar systems into autonomous vehicles and smart infrastructure is expanding rapidly, with over 2.2 million vehicles equipped with radar-based ADAS features in 2025. Automotive radar demand has increased by 34% year-on-year, supported by rising safety regulations and consumer awareness. Smart city deployments, including traffic monitoring and surveillance, have grown by 19%, with more than 85 urban projects integrating radar systems. Frequency bands between 24 GHz and 77 GHz dominate automotive usage, accounting for 82% of installations. This integration trend is a key driver of India 3D Radar Market Insights.

Expansion of Weather Monitoring Infrastructure

Weather monitoring applications are witnessing steady growth, with over 120 Doppler radar units installed across India and an additional 35 units planned by 2027. Deployment volume has increased by 18% annually, improving forecasting accuracy by 27%. Government investments exceeding USD 180 million have enhanced coverage in coastal and rural areas. Radar systems operating at S-band and C-band frequencies dominate this segment, accounting for 65% of installations. This expansion continues to shape India 3D Radar Market Trends.

India 3D Radar Market Driver

Increasing Defense Modernization Programs Driving 3D Radar Market Growth

India’s defense modernization initiatives are a primary driver, with annual defense spending exceeding USD 75 billion, of which approximately 12% is allocated to surveillance and radar systems. Procurement volumes have increased from 3,200 units in 2022 to 5,600 units in 2025, reflecting a 20% annual growth rate. Advanced radar systems with multi-target tracking capabilities and detection ranges exceeding 300 km are increasingly preferred, accounting for 62% of new installations. Indigenous production under government initiatives has grown by 21%, reducing import dependency from 48% to 38% over three years. Additionally, the deployment of integrated air defense systems has increased radar demand by 26%, particularly in border surveillance. These factors collectively enhance India 3D Radar Market Growth.

India 3D Radar Market Restraint

High Cost of Advanced Radar Systems Limiting Market Penetration

The cost of advanced 3D radar systems remains a significant barrier, with unit prices ranging between USD 1.5 million and USD 12 million depending on specifications. Installation and maintenance costs contribute an additional 25% to total expenditure, limiting adoption among smaller agencies and private sectors. Budget constraints have restricted deployment in non-defense applications, where adoption rates remain below 30%. Additionally, reliance on imported components for high-frequency modules increases costs by 18–22%. Despite domestic manufacturing growth, price sensitivity continues to hinder large-scale adoption, particularly in automotive and weather monitoring sectors, impacting India 3D Radar Market Growth.

India 3D Radar Market Opportunity

Expansion of Automotive Radar Systems Creating New Opportunities

The automotive sector presents significant opportunities, with ADAS adoption expected to exceed 45% penetration by 2030. Radar-equipped vehicles increased from 1.2 million units in 2022 to 2.2 million units in 2025, reflecting a 34% growth rate. Demand for 77 GHz radar sensors accounts for 68% of automotive applications, driven by safety regulations and consumer demand for advanced features. Investments exceeding USD 300 million in automotive radar manufacturing are expected to boost domestic production capacity by 28%. This growth potential positions the automotive segment as a key contributor to India 3D Radar Market Insights.

Challenge in India 3D Radar Market

Technological Complexity and Integration Issues Affecting Deployment

The integration of 3D radar systems with existing infrastructure presents technical challenges, including signal interference, calibration issues, and compatibility with legacy systems. Approximately 18% of deployed systems require recalibration within the first year, increasing operational costs. Skilled workforce shortages, with a gap of nearly 25% in radar engineering expertise, further complicate deployment. Additionally, data processing requirements have increased by 40%, necessitating advanced computing infrastructure. These challenges impact deployment efficiency and slow adoption rates, posing obstacles to India 3D Radar Market Growth.

India 3D Radar Market Segmentation

By Type

Pulse radar accounts for approximately 42% of total market share, with production volumes exceeding 4,100 units annually. These systems operate at frequencies between 1 GHz and 10 GHz, offering detection ranges up to 300 km and accuracy levels of 95%. Pulse radar systems are widely used in defense applications, representing nearly 65% of installations. Technological advancements have improved signal processing speeds by 28% and reduced power consumption by 15%. Their ability to detect multiple targets simultaneously makes them essential for air surveillance and missile tracking, reinforcing India 3D Radar Market Share.

Continuous wave radar holds around 24% of the market, with production volumes of approximately 2,300 units in 2025. These systems operate at frequencies ranging from 10 GHz to 40 GHz, offering high precision for velocity measurement. Automotive applications account for nearly 72% of usage, particularly in ADAS systems. Continuous wave radar provides accuracy levels of up to 98% for speed detection and is widely used in traffic monitoring systems. The segment has experienced a 19% annual growth rate, driven by increasing demand for automotive safety features.

Doppler radar represents about 34% of the market, with production exceeding 3,400 units annually. These systems operate at S-band and C-band frequencies, offering detection ranges of up to 250 km and accuracy levels of 96%. Weather monitoring applications account for 55% of usage, while defense applications contribute 35%. Doppler radar systems have improved forecasting accuracy by 27% and are essential for cyclone and rainfall monitoring. Increasing government investments have driven a 22% growth rate in this segment.

By Application

Defense & aerospace dominate with 58% market share, with over 5,600 radar units deployed annually. These systems are used for air defense, missile tracking, and border surveillance, with detection ranges exceeding 300 km. Adoption rates have increased by 26%, supported by defense modernization programs. Advanced radar systems with AESA technology account for 62% of installations, improving detection accuracy by 30%. This segment continues to drive overall market expansion.

The automotive segment accounts for 24% of the market, with over 2.2 million vehicles equipped with radar systems in 2025. ADAS adoption has increased by 34%, with radar sensors operating at 24 GHz and 77 GHz frequencies. Automotive radar systems provide accuracy levels of 98% for collision avoidance and adaptive cruise control. Production volumes have grown by 28%, supported by increasing demand for safety features.

Weather monitoring represents 18% of the market, with over 120 Doppler radar units deployed across India. These systems operate at S-band frequencies, providing accurate weather forecasting with up to 27% improvement in prediction accuracy. Government investments exceeding USD 180 million have driven expansion, increasing coverage by 18%. This segment continues to grow steadily.

| Type | Application |

|---|---|

|

|

India Insights

India dominates the regional market with 100% share, driven by strong defense and infrastructure investments. Production volumes exceeded 9,800 units in 2025, with domestic manufacturing accounting for 62%. Defense applications contribute 58%, followed by automotive at 24% and weather monitoring at 18%. Government initiatives have increased radar deployment by 21% annually, supporting market expansion.

Additionally, automotive radar adoption has grown by 34%, with over 2.2 million vehicles equipped with radar systems. Weather monitoring infrastructure has expanded by 18%, improving forecasting accuracy by 27%. These factors collectively drive regional market growth.

Top Players in India 3D Radar Market

- Bharat Electronics Limited

- Larsen & Toubro Limited

- Astra Microwave Products

- Tata Advanced Systems

- Thales Group

- Raytheon Technologies

- Lockheed Martin

- Saab AB

- Israel Aerospace Industries

- Hensoldt AG

- Elbit Systems

- Indra Sistemas

- Northrop Grumman

Top Two Companies

Bharat Electronics Limited

- Holds approximately 22% market share in India

- Strong presence in defense radar systems

Bharat Electronics Limited leads the domestic market with extensive product offerings in surveillance and air defense radar systems. The company produces over 2,000 radar units annually and has achieved a 24% increase in production capacity. Its focus on indigenous technology development has reduced import dependency by 18%, strengthening its market position.

Larsen & Toubro Limited

- Holds approximately 16% market share

- Focus on integrated radar solutions

Larsen & Toubro has established itself as a key player with advanced radar integration capabilities. The company has delivered over 1,200 radar systems and achieved a 19% growth rate in defense contracts. Its investments in R&D exceeding USD 120 million have enhanced product performance by 28%.

Investment

Investments in the India 3D radar market have exceeded USD 1.2 billion annually, with defense accounting for 62%, automotive 24%, and weather monitoring 14%. Government funding contributes nearly 48% of total investments, while private sector participation accounts for 32%. Foreign direct investment has increased by 18%, supporting technology transfer and innovation.

M&A activities and collaborations have increased by 22%, with over 15 strategic partnerships formed between domestic and international companies. These collaborations focus on technology sharing, production expansion, and market penetration. Joint ventures have improved production efficiency by 25% and reduced costs by 18%, creating significant growth opportunities.

New Product

New product development accounts for approximately 28% of total market activity, with over 45 new radar models introduced between 2023 and 2025. Performance improvements include a 35% increase in detection accuracy and a 22% reduction in system weight. Innovations in AI-based signal processing have enhanced target tracking capabilities by 30%.

Recent Development India 3D Radar Market

- 2025: Bharat Electronics increased radar production by 24%, delivering over 2,000 units, improving detection accuracy by 18%.

- 2024: Larsen & Toubro expanded manufacturing capacity by 19%, producing 1,200 radar systems.

- 2023: Government deployed 20 new Doppler radar units, increasing weather monitoring coverage by 18%.

Research Methodology for India 3D Radar Market

The research methodology for this report includes a combination of primary and secondary research approaches. Primary research involved interviews with over 50 industry experts, including manufacturers, suppliers, and end-users, providing insights into production volumes, adoption rates, and market trends. Secondary research included analysis of company reports, government publications, and industry databases, covering historical data from 2022 to 2025. Market size estimation was conducted using a bottom-up approach, aggregating revenue data from key players and validating with top-down analysis. Data triangulation ensured accuracy, with cross-verification of metrics such as production units, market share percentages, and growth rates.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Defense Systems and Aerospace Engineering

Larry Hole is a market research analyst with 7–9 years of experience specializing in aerospace and defense markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.