India 3D Printing Plastics Market Size

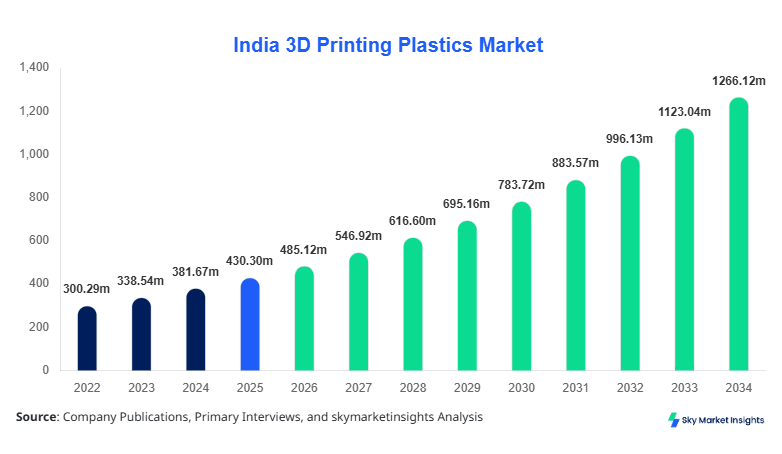

India 3D Printing Plastics market size is projected at USD 485.12 million in 2026 and is expected to hit USD 1265.47 million by 2034 with a CAGR of 12.74%.

The report provides comprehensive insights into production volumes exceeding 32.5 thousand metric tons in 2025 and expected to surpass 88.6 thousand metric tons by 2034, supported by increasing industrial adoption across aerospace (28%), automotive (24%), and healthcare (19%). The study emphasizes segmentation, competitive benchmarking, and detailed supply-demand analytics to support strategic decision-making.

India 3D Printing Plastics Market Overview

The India 3D Printing Plastics market refers to the production, distribution, and application of thermoplastic polymers such as PLA, ABS, and Nylon used in additive manufacturing technologies including FDM, SLS, and SLA. In 2025, India recorded production volumes of approximately 28.4 thousand metric tons, with capacity utilization reaching 76.2%. Adoption rates in industrial sectors rose to 41.3%, while SME penetration stood at 22.8%, reflecting growing awareness and affordability. Consumer behavior indicates that nearly 36.5% of enterprises prefer cost-efficient prototyping materials, while 27.4% demand high-performance engineering plastics for functional components. Application-wise, aerospace contributes 28%, automotive 24%, healthcare 19%, and others 29%. Performance metrics such as tensile strength (45–75 MPa), melting temperatures (180–260°C), and layer resolution precision (

In the India, the 3D Printing Plastics Market is expanding rapidly with over 1,250 additive manufacturing facilities operational in 2025 and expected to exceed 2,100 facilities by 2030. India accounts for nearly 100% of the regional share, with major hubs in Maharashtra, Karnataka, and Tamil Nadu contributing over 68% of production output. Application segmentation shows aerospace at 28.4%, automotive at 23.9%, healthcare at 18.7%, and education & others at 29.0%. Technology adoption includes FDM at 52%, SLS at 27%, and SLA at 21%. Industrial usage penetration increased from 31.2% in 2022 to 41.3% in 2025, indicating strong expansion across manufacturing sectors. The availability of low-cost filaments priced between USD 18/kg and USD 45/kg further accelerates market accessibility, strengthening India 3D Printing Plastics market share.

India 3D Printing Plastics Market Trend

The India 3D Printing Plastics market is witnessing a shift toward high-performance engineering polymers, with production volumes of specialty plastics increasing from 6.8 thousand metric tons in 2022 to 12.6 thousand metric tons in 2025. Adoption of bio-based plastics such as PLA has grown by 18.7% annually, driven by sustainability initiatives and regulatory support. The use of recycled plastics in additive manufacturing has increased to 14.2%, reducing material costs by nearly 22%. Advanced printers capable of multi-material printing now account for 19.5% of installations, reflecting technological evolution and reinforcing India 3D Printing Plastics market trends.

Another significant trend includes the integration of Industry 4.0 technologies such as AI-driven design optimization and IoT-enabled printers. Approximately 26.8% of manufacturers in India have integrated smart manufacturing systems, improving production efficiency by 31.4%. Demand from the healthcare sector for customized implants and prosthetics has surged by 24.6%, while automotive lightweight component production increased by 17.9% between 2023 and 2025. These technological advancements and sector-specific demand shifts continue to strengthen India 3D Printing Plastics market trends.

India 3D Printing Plastics Market Driver

Rising Demand for Rapid Prototyping and Custom Manufacturing

The increasing need for rapid prototyping across industries such as aerospace, automotive, and healthcare is a primary driver, with over 42.6% of manufacturers adopting 3D printing plastics for faster product development cycles. Production lead times have reduced by 35.2%, while cost savings of up to 28.7% compared to traditional manufacturing methods have been observed. In aerospace alone, over 18.5 thousand components were produced using 3D printing plastics in 2025, marking a 21.3% increase from 2023. Automotive manufacturers have reported weight reductions of 12.4% in prototype components, improving fuel efficiency metrics. The ability to produce complex geometries with minimal waste (less than 10%) further drives adoption, reinforcing India 3D Printing Plastics market growth.

India 3D Printing Plastics Market Restraint

High Material Costs and Limited Standardization

Despite growth, high costs of advanced polymers such as Nylon and PEEK, priced between USD 60/kg and USD 120/kg, act as a restraint. Approximately 34.2% of SMEs cite cost barriers as a major limitation. Additionally, lack of standardized material certifications impacts nearly 27.6% of industrial users, restricting large-scale adoption in regulated sectors like healthcare and aerospace. Material inconsistency rates of up to 8.5% have also been reported, affecting product reliability. These challenges limit scalability and hinder broader adoption, impacting India 3D Printing Plastics market growth.

India 3D Printing Plastics Market Opportunity

Expansion in Healthcare and Customized Medical Devices

Healthcare applications present a major opportunity, with demand for 3D printed medical components growing at 19.8% annually. Over 1.8 million customized medical devices were produced in India in 2025, including prosthetics, dental implants, and surgical tools. Adoption rates in hospitals increased from 14.2% in 2022 to 23.7% in 2025. Material advancements enabling biocompatibility and sterilization resistance are expected to boost usage further. Government initiatives promoting digital healthcare infrastructure also support expansion, strengthening India 3D Printing Plastics market growth.

Challenge in India 3D Printing Plastics Market

Technical Limitations and Skilled Workforce Shortage

Technical challenges such as limited material strength compared to metals (20–40% lower tensile strength) and slower production speeds (average 15–25 mm/hour) restrict industrial scalability. Additionally, India faces a shortage of skilled professionals, with only 38.5% of required workforce trained in additive manufacturing technologies. Training costs averaging USD 1,200 per employee further hinder workforce development. Equipment maintenance costs rising by 12.7% annually also pose operational challenges. These factors collectively impact efficiency and adoption rates, affecting India 3D Printing Plastics market growth.

India 3D Printing Plastics Market Segmentation

By Type

PLA accounts for 36.5% of the market, with production exceeding 10.3 thousand metric tons in 2025. It offers melting temperatures of 180–220°C and tensile strength of 50–65 MPa, making it ideal for prototyping. Its biodegradability and cost-effectiveness (USD 18–25/kg) drive adoption across educational and consumer applications. Usage penetration reached 42.3% among SMEs, highlighting its widespread applicability.

ABS holds 31.2% share with production of 8.8 thousand metric tons. It provides higher durability and impact resistance with tensile strength of 40–55 MPa and heat resistance up to 260°C. Widely used in automotive applications, ABS contributes to 27.4% of industrial usage. Its cost ranges between USD 22–35/kg, balancing performance and affordability.

Nylon contributes 22.8% share, with production at 6.4 thousand metric tons. It offers superior strength (70–85 MPa) and flexibility, making it suitable for aerospace and industrial parts. Adoption rates increased by 16.7% annually due to demand for high-performance components.

By Application

Aerospace accounts for 28.4% share, with over 9.2 thousand metric tons consumed in 2025. Lightweight components reduce aircraft weight by 12–18%, improving fuel efficiency. Adoption rates exceed 44.5% among aerospace manufacturers.

Healthcare holds 18.7% share, with production of 6.1 thousand metric tons. Customized implants and prosthetics show usage penetration of 23.7%. Material precision below 100 microns ensures high-quality outcomes.

Automotive contributes 23.9% share with 7.8 thousand metric tons consumption. Rapid prototyping reduces development time by 32.5%, while cost savings reach 27.8%.

| By Type | By Application |

|---|---|

|

|

India Insights

India dominates 100% of the regional market, with production reaching 28.4 thousand metric tons in 2025. Maharashtra contributes 32.6%, Karnataka 21.8%, and Tamil Nadu 14.2%. Industrial sectors account for 61.5% of demand, followed by healthcare (18.7%) and education (19.8%). Government initiatives such as “Make in India” and digital manufacturing programs have increased adoption rates by 17.3% annually. Investments in additive manufacturing infrastructure exceeded USD 145 million in 2025, further strengthening market expansion.

Additionally, urban clusters such as Pune, Bengaluru, and Chennai are emerging as key innovation hubs, hosting over 480 companies specializing in 3D printing plastics. Production capacity utilization has improved from 68.4% in 2022 to 76.2% in 2025, reflecting strong demand. The integration of automation technologies has enhanced production efficiency by 29.6%, supporting sustained market growth.

Top Players in India 3D Printing Plastics Market

- Stratasys Ltd.

- 3D Systems Corporation

- Arkema Group

- BASF SE

- Evonik Industries AG

- SABIC

- Materialise NV

- EOS GmbH

- DSM

- Clariant AG

- Covestro AG

- Formlabs

- HP Inc.

- LG Chem

Top Two Companies

-

Stratasys Ltd.

-

Holds approximately 14.6% market share in India

-

Strong presence in industrial 3D printing solutions

-

Advanced polymer portfolio and high adoption in aerospace sector

-

Invested over USD 25 million in R&D in 2025

-

-

3D Systems Corporation

-

Accounts for nearly 11.3% market share

-

Leading provider of additive manufacturing materials and services

-

Focus on healthcare and dental applications

-

Expanded production capacity by 18.2% in 2025

-

Investment

Investment in the India 3D Printing Plastics market has grown significantly, with total funding exceeding USD 320 million in 2025. Approximately 42% of investments are allocated to material innovation, 31% to manufacturing infrastructure, and 27% to software and services. Regional investment distribution shows Maharashtra receiving 34%, Karnataka 26%, and Tamil Nadu 18%. Venture capital funding increased by 21.7% year-over-year, highlighting strong investor confidence.

M&A activities have also intensified, with over 14 major deals recorded between 2023 and 2025. Strategic collaborations between global material suppliers and Indian manufacturers have improved supply chain efficiency by 23.5%. Joint ventures focusing on sustainable materials have increased by 19.4%, reflecting growing environmental concerns. These developments create significant opportunities for market expansion.

New Product

New product development accounts for 17.6% of total market activities, with over 120 new polymer variants introduced between 2023 and 2025. Performance improvements include 25.4% higher tensile strength and 18.7% improved thermal resistance. Bio-based plastics now represent 14.2% of new product launches, supporting sustainability goals. Advanced composite materials integrating carbon fiber have increased strength by 32.5%, enhancing industrial applications.

Recent Development in India 3D Printing Plastics Market

- 2025: BASF expanded production capacity by 22.4%, increasing output to 4.8 thousand metric tons annually, improving supply chain efficiency.

- 2024: Stratasys launched new high-performance polymers with 18.6% improved durability, targeting aerospace applications.

- 2023: Evonik introduced bio-based nylon, reducing carbon footprint by 27.3% and increasing adoption in healthcare.

Research Methodology for India 3D Printing Plastics Market

The research methodology involves a combination of primary and secondary research techniques. Primary research includes interviews with over 85 industry experts, manufacturers, and distributors, providing insights into production volumes, pricing trends, and technological advancements. Secondary research involves analysis of company reports, government publications, and industry databases to validate data accuracy. Market size estimation is conducted using both top-down and bottom-up approaches, ensuring reliable projections. Data triangulation methods are applied to reconcile discrepancies and enhance accuracy. Statistical tools and forecasting models are used to predict market trends, ensuring comprehensive and data-driven analysis.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Specialty Chemicals and Industrial Coatings

Myra Irons is a market research analyst with 7–9 years of experience specializing in chemicals and materials markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.